Are We Entering an Earnings/Sales Recession?

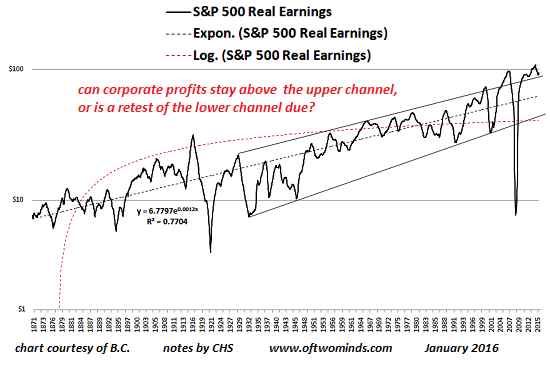

Are corporate profits due for a retest of the lower channel line? If so, what happens to equity valuations when corporate profits plummet?

Is the U.S. economy in recession? Is it heading for recession? These questions can only be answered in hindsight, but it’s worth looking for clues to what might be just ahead.

Longtime correspondent B.C. recently submitted a chart of corporate earnings and one of real demand and time deposits (a measure of money) and real final sales.

(Explanation of demand deposits).

Unsurprisingly, all three of these metrics tank in recessions.

Corporate profits have been hugging the upper line of a long-term channel for years.

While real final sales have not yet plunged to recession levels, the annual change in real demand and time deposits has fallen into negative territory.

While the annual change in demand and time deposits has swung between positive and negative for decades, the annual change in real final sales only enters negative territory in recessions.

While the two series don’t align perfectly, there is a clear correlation between the expansion of money supply and sales.

For this reason, the recent decline in demand and time deposits might serve as an early warning of an impending drop in real sales to recession levels.

Corporate profits have remained in a rising channel for 85 years, with one exception: the Global Financial Meltdown of 2008-09.

Interestingly, all three recent equity bubbles–in 2000, 2007 and the current bubble–align with corporate profit peaks above the upper channel line.

Are corporate profits due for a retest of the lower channel line? If so, what happens to equity valuations when corporate profits plummet? These questions may be answered later in 2016.

…click on the above link to read the rest of the article…