China’s Losing Control Of Its Crushing Debt Load As Defaults And Missed Payments Skyrocket

China’s economic slowdown and heavy debt load is affecting everybody in the country – even it’s “jewelry queen”, Zhou Xiaoguang, according to the Wall Street Journal.

Zhou, who went from selling trinkets on city streets to taking a seat in China’s parliament and becoming Ernst & Young‘s “Entrepreneur of the Year” was faced with the reality of being unable to pay her company’s billions of dollars in debt while in a bankruptcy court in April.

She is just one example of a massive debt burden taking its toll on China.

China has relied on borrowing to fuel its expansion for at least a generation. In 2018, the country was known for creating four billionaires a week and is number one globally in self-made fortunes. But this quick pace of growth, with many borrowing heavily in the process, also masked companies’ strategic mistakes.

Fueled by debt, many over-expanded into crowded sectors and now those mal-investments and mis-allocations of resources are coming back to bite them.

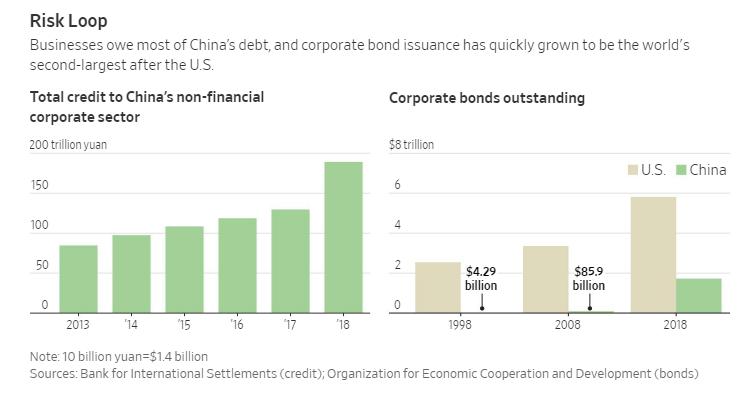

Over the past decade, the overall debt of the country has quadrupled to about three times the value of last year’s national output. Corporate debt makes up 2/3 of the total, amounting to more than $26 trillion last year. Most of the money is owed by government-run companies, but the stress is starting to surface also at private companies, who have less wiggle room with creditors and less support from the government.

For instance, Chenxi Group was decimated by lenders last year when they suddenly decide to call in loans. Earlier that year, the founder of machine maker Zhejiang Jindun Group committed suicide, leaping to his death, leaving the company to later reveal that it owed about $1.4 billion to loan sharks.

…click on the above link to read the rest of the article…