Has the PBoC deliberately weakened CNY as part of the trade war?

It has been another trade war week, as the market has been looking for clues on the Chinese retaliation measures against the Trump tariffs that are planned to go live on 6 July.

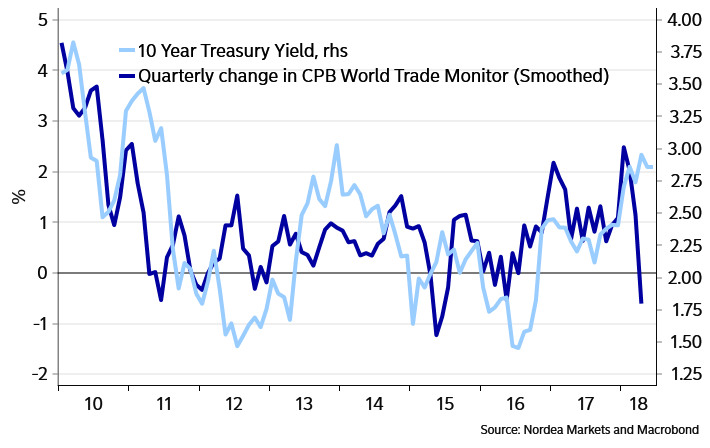

Global trade momentum started to weaken even before the trade conflict escalated. The three months from February until April marked the weakest running 3-month period for world trade since early 2015. A bad sign given that the period included a temporary cease-fire between Trump and Xi Jinping. Usually it adds downwards pressure on 10yr bond yields, when world trade is slowing (at least initially). A further slowdown of global trade in June/July/August could keep long bond yields under pressure over the summer. In other words, the trade war fog needs to dissipate for the 10yr US Treasury yield to unfold its upside potential to the range between 3.25%-3.50% (Major Forecast Update: USD to remain in the driving seat)

Chart 1: Less global trade, lower long bond yields

Last week we wrote that we found trade-based Chinese retaliation measures more likely than attempts to retaliate via the financial markets. The fact that Trump is threatening with new tariffs on goods worth a total of USD 450bn makes the retaliation process trickier for China. It is simply not possible to retaliate symmetrically, as there are not enough US exports into China to tax. This leaves an elevated risk of unorthodox retaliation measures being used. Prohibiting symbolic US products from entering Chinese territory could be one way of doing it. Expect more clarity on whether Xi Jinping will deliver an ALL-IN answer as early as this weekend.

…click on the above link to read the rest of the article…