The parallels between the last few years and those at the end of the 1990’s are striking. There was a few years ago the monetary intrusion of the “rising dollar” which at its worst seriously depressed the global economy. Oil prices crashed, as did several key currencies, and deflationary pressures that often accompany a significant downturn were manifest.

Starting in 1997, there was all of that, too. Oil prices though much lower to begin with were crushed, overseas the “dollar” “rose”, and currency problems were everywhere particularly in Asia (Japan both times, China only the later). And there were asset bubbles in both.

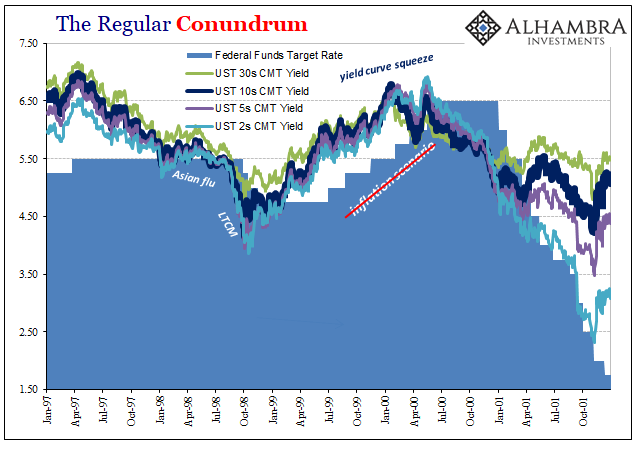

In terms of consumer price inflation, the similarities did not end. In 1999, the Federal Reserve having failed to account for the reasons behind the Asian flu began to act in anticipation of rising inflation. Ignoring bond market warnings, as Economists always do, the Fed took the excuse of oil price effects and their impacts on consumer price indices as justification.

Raising rates throughout 1999 and 2000, the central bank was eventually stopped by the collapse of the dot-com bubble and the deflationary pressures of recession as well as finance it did not foresee even though the bond market had been trading against them all along. Inflation, as a necessary consequence, fell back, too.

At its apex, the PCE Deflator in early 2001 reached a high of 2.87% and went no further. What was missing from the episode was every indication of broad-based consumer price inflation that might have suggested their concerns over acceleration or related imbalance. The so-called core rate never really moved all that much, indicating that oil prices off the 1999 lows were entirely responsible for the rise in the rate (WTI was up more than 60% year-over-year when the PCE Deflator registered that 2.87%).

…click on the above link to read the rest of the article…