CREDITWORTHINESS OF NEW YORK AND ILLINOIS: ONE IS BANKRUPT

- Unless used for capital improvements, any new Illinois State borrowing, regardless of security structure, will amount to nothing more than kicking the can further down the road.

- Markets remain open to uncreditworthy government borrows longer than they should. In a low interest rate environment, investors will stretch credit standards.

- Benchmark bond ratings are at variance with the rating agencies.

Everyone knows Illinois’ financial condition is poor. Conventional thinking seems to be that a bond default, should that happen, would be many years in the future. Pardon me, but wasn’t that the thinking right up to Puerto Rico’s, “We can’t pay” announcement? To answer the question of just how badly off is Illinois, I assembled a list of key creditworthiness indicators and applied them to New York, a highly rated state, and Illinois.

COMMENTARY AND BENCHMARK PRIVATE BOND RATINGS

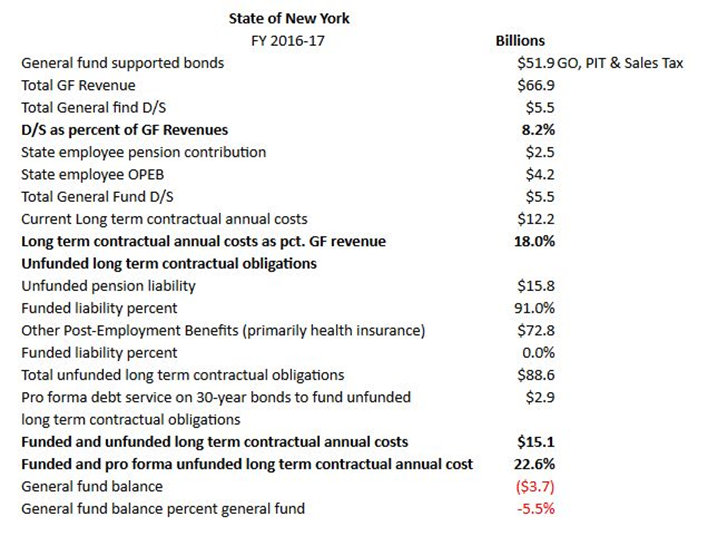

The State of New York is managing its financial resources and obligations in a better-than-average manner. Particularly, the State’s employee pensions are reported to be 90% funded, but the general fund deficit must be contained and then eliminated. Unfunded OPEB costs are too high and can be renegotiated. Funded and pro forma unfunded long-term contractual obligations equaled 23% of general fund revenue in FY ended June 30, 2017, and exceeds the 15% threshold for a Benchmark AA or AA+ credit rating.

*Both NYS income tax and sales tax bonds are payable from annual general fund appropriation. For additional information, click here.

COMMENTARY AND BENCHMARK PRIVATE BOND RATINGS

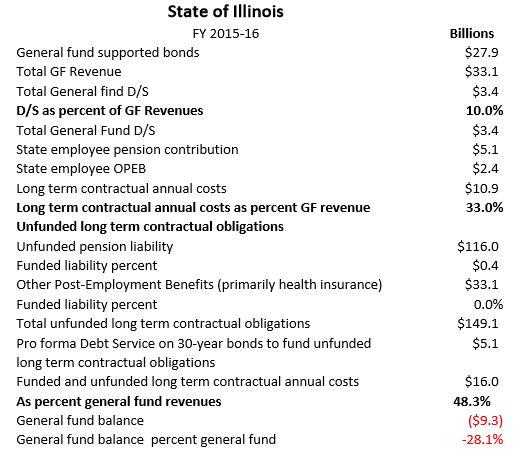

The State of Illinois, in my opinion, is past the point of no return. It does not have the ability to raise taxes or cut spending to the degree necessary to reduce the annual cost of bond and retiree benefits from 33% to a sustainable level. The amount of debt issued by Illinois requires a moderate 8% of general fund revenues to pay P&I.

…click on the above link to read the rest of the article…