Summary

- IEA predicts global oil demand will peak by 2030, leading to an 8 million b/d surplus due to Electric Vehicle and energy transition movement.

- IEA’s outlook shows a disconnect between GDP growth and oil demand growth, with unrealistic assumptions about EV penetration and gasoline demand drop.

- Despite IEA’s flawed projections, there are insights in the report suggesting peak oil supplies this decade, particularly in US shale production.

- We see an oil market that’s going to be in a sustainable deficit by 2030.

- Looking for a helping hand in the market? Members of HFI Research get exclusive ideas and guidance to navigate any climate. Learn More »

Roman Mykhalchuk

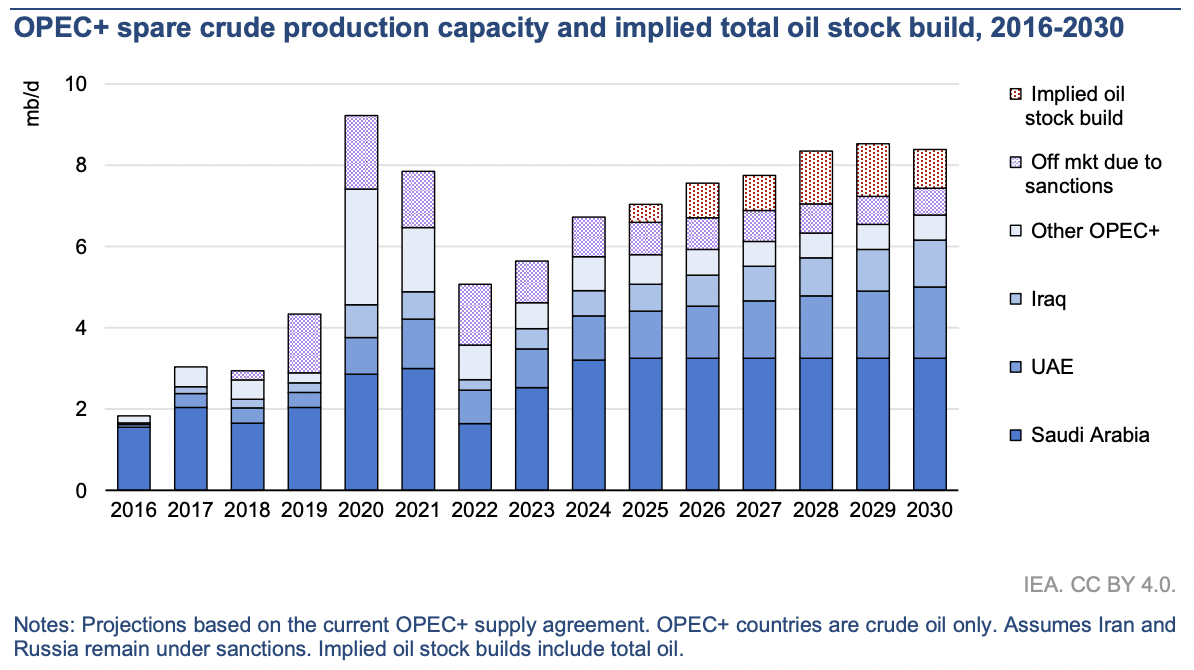

IEA published its latest 2030 outlook yesterday, and I don’t even know where to start. The big headline from the IEA medium-term outlook is that global oil demand will peak by 2030, and oil producers are going to face a surplus as large as ~8 million b/d thanks to Electric Vehicles (“EVs”) and the energy transition movement.

IEA

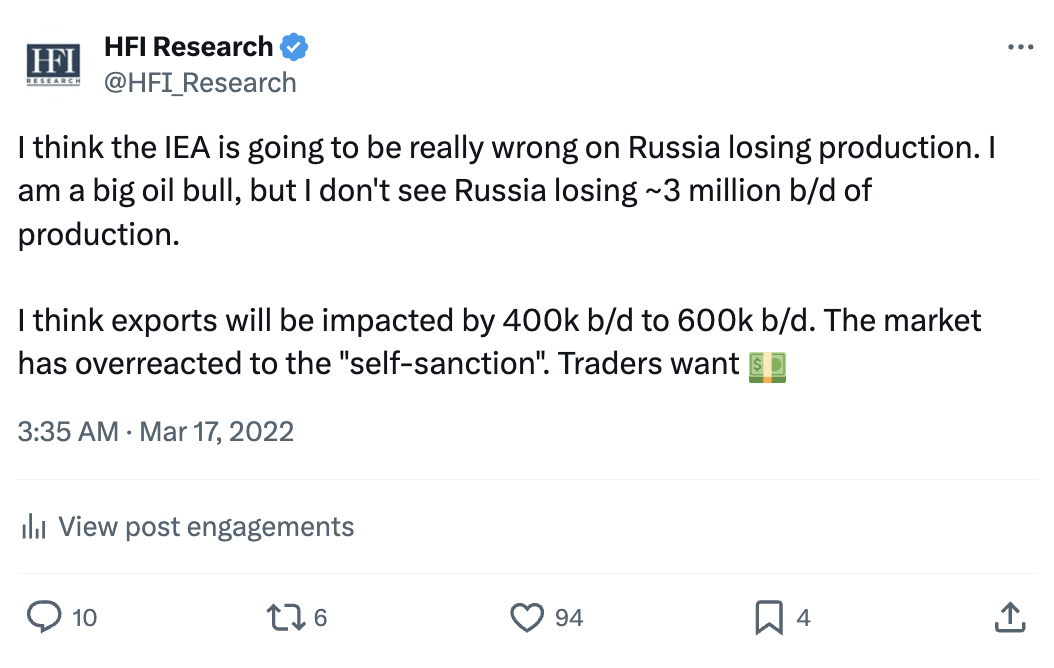

For energy investors, this is the greatest confirmation signal you needed. As a golden rule in energy investing, we’ve learned that fading the IEA has almost always worked. Who remembers IEA’s famous call in March 2022 for Russia to lose ~3 million b/d of oil production following the Ukraine invasion?

We remember, and at the time, we published a piece cautioning those following IEA’s prediction. In addition, we also tweeted at the time the following:

HFIR

With the benefit of hindsight, Russia lost zero barrels, and we ended up being wrong about the 400k b/d to 600k b/d export loss as well.

Nonetheless, the point of this article is to look at the rationale behind IEA’s massive surplus estimate. There are some notable bullish figures in these charts as well, disguised behind the hideous demand estimates.

Let’s get started.

Delusion

…click on the above link to read the rest of the article…