We Finally Understand How Destructive Negative Interest Rates Actually Are

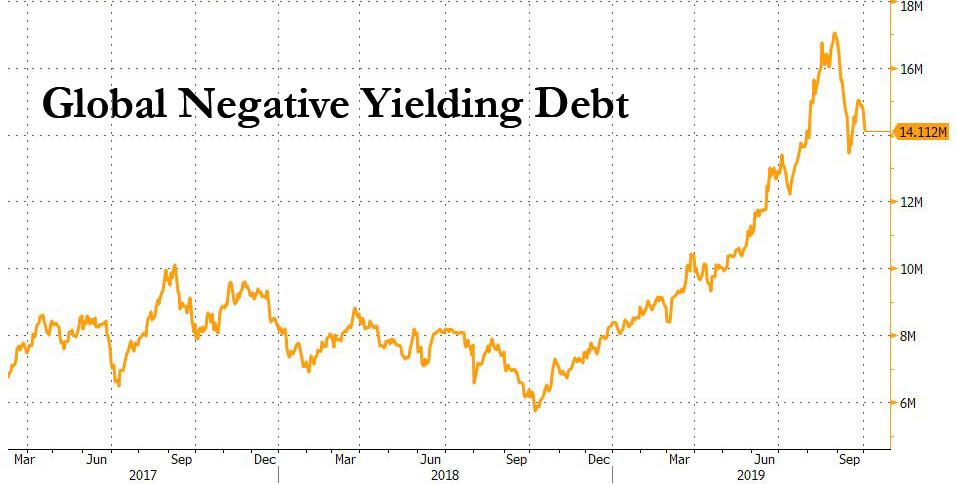

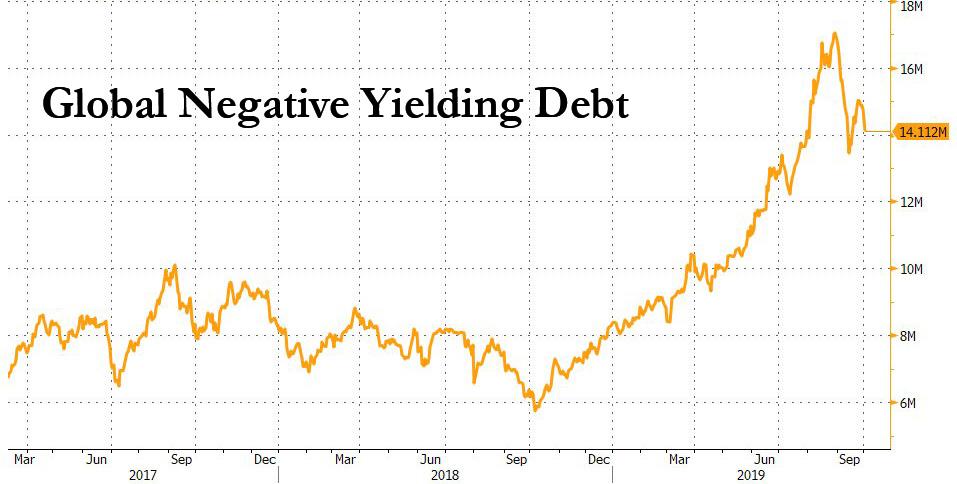

We are in the midst of a strange economic experiment. Vast quantities of negative-yielding debt are currently sloshing around the global economy. While the amount of negative-yielding bonds has dropped recently from a mind-boggling number in excess of $17 trillion, reinvigorated central bank easing across the globe ensures that this reduction is only temporary.

We are slowly starting to understand how destructive negative interest rates actually are. Central banks control short-term interest rates in an economy by setting the rate banks receive on their deposits, that is, on the reserves they hold at the central bank. A new development is the control central banks now exert over long-term rates through their asset purchase, or “QE” programs.

{kind=link}

Banks profit from the interest rate differential between “lending long” but “borrowing short”. Essentially, the difference between lending and deposit rates determine a bank’s profitability. However, with today’s very low interest rates, this difference becomes almost non-existent, and with negative rates, inverts completely.

When a central bank pushes rates to negative, banks need to pay interest on the reserves they hold there. But they are not relieved of the obligation they have to pay interest on customer deposits, who are understandably reluctant to pay interest on money they place at a bank. Consequently, the whole earnings logic of banking goes haywire if banks are required to pay interest on loans and receive interest on deposits. As profit margins of banks are squeezed, profitability falls and lending activities suffer.

However, the problems created by negative interest rates do not stop there. In 2008, an influential article describing the economic malaise in Japan after the financial crash of the early 1990s found that instead of calling-in or refusing to refinance existing debts, large Japanese banks kept loans flowing to otherwise insolvent borrowers.

…click on the above link to read the rest of the article…