The long-awaited shale patch consolidation has arrived, sparking another bout of merger mania in the energy industry. It’s reminiscent of the one in the late 1990s, just as the Internet bubble was exploding. But don’t expect the stocks to rally this time.

Parallels between tech in the 1990s and today are common. But there’s been little mention of what the energy sector went through at the same time and how it suddenly looks so familiar. History’s repeating itself as it appears energy can’t attract investors — again.

Then as now, the backdrop to energy’s M&A boom is a collapse in oil prices. The difference this time, however, is the deals are happening at a quarter of the traditional premiums.

During this pandemic era, four deals have already emerged: Chevron’s takeover of Noble Energy, ConocoPhillips’s acquisition of Concho Resources, Pioneer Natural Resources’s purchase of Parsley Energy and Devon Energy’s merger with WPX Energy. This appears to be just the beginning as rumors circulate of more deals to come.

The economy has structurally changed since 2000, which makes tech’s acceleration look real and lasting. That’s not so for the energy industry, which staged a comeback in the early part of the century as tech dropped. But this time around, the sector faces worsening supply dynamics and a demand hit from which it’s likely to take years to recover.

Supply dynamics were not favorable even before the pandemic. The American shale boom and cheating on OPEC+ production quotas created an oversupplied oil market. Trade risk added to worries for shale producers, which were already treading water.

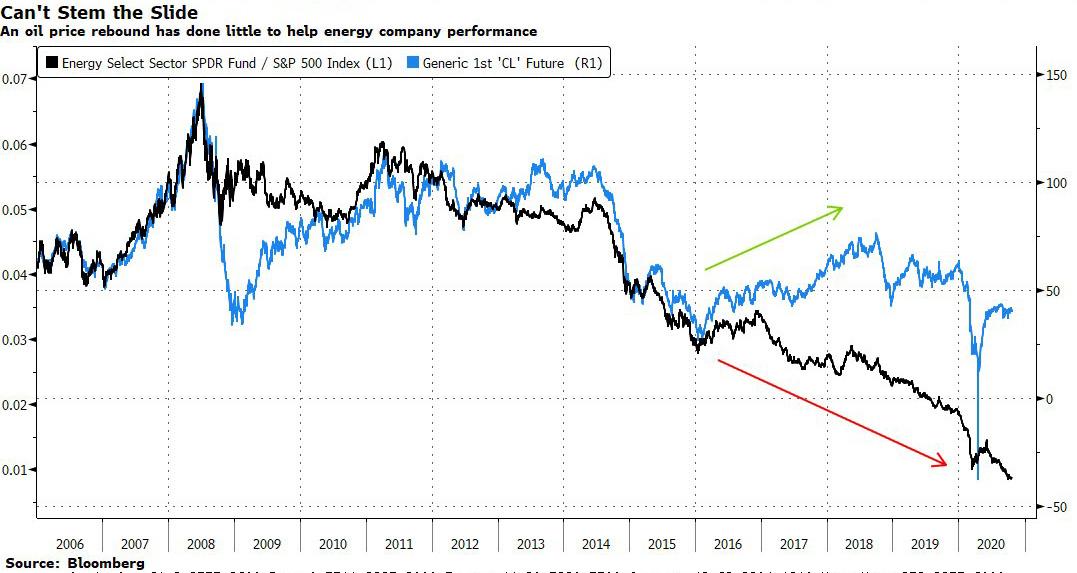

Since 2017, the pain has become clearer. Oil rallies have seldom spilled over into energy stocks beyond a brief increase in valuations spurred by private equity in 2016.

…click on the above link to read the rest of the article…