The Debate Is Over: In Two Months “Not QE” Officially Becomes QE 4

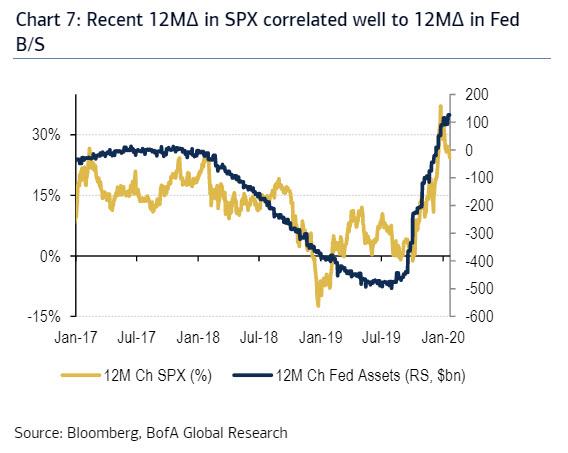

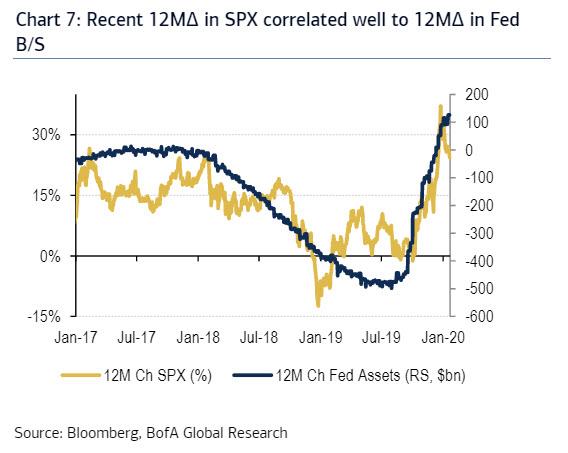

While Neel Kashkari may be theatrically appealing to the intellect of “QE conspiracists” – which as of today in addition to Robert Kaplan, Larry Kudlow and James Gorman also includes as per the chart below Bank of America, in addition to any other person with an even modest understanding of monetary policy…

… to explain to him how the Fed is moving prices with its $60BN in monthly purchases of T-Bills (something we did last week), an key development is coming that will make all such debates moot: in a few months the Fed’s “Not QE” will officially become “QE 4.”

{kind=link}

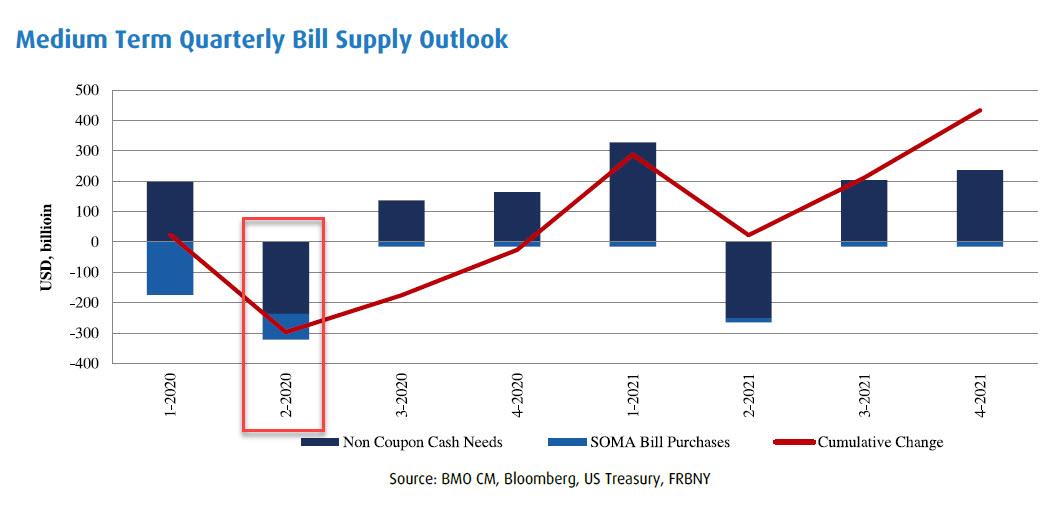

The reason: following an update to BMO’s bill supply forecasts, the bank’s rates strategist Jon Hill sees a great likelihood that the Fed will need to reduce its “demand burden” on the bill market, i.e., there won’t be enough Bills available for the Fed to monetize without it distorting the market, and will extend the purchase program to include short coupons in the process officially ending any debate whether the Fed’s manipulation of the market under the guise of saving repo, is “Not QE”, because it is limited to Bills and thus no duration is taken out of the market, or is “QE 4”, in which the Fed purchases at least some coupon securities in addition to Bills.

Once the Fed makes the shift, BMO expects the monthly sizes of $60 bn, or $30 bn post assumed taper, would be composed of both bills and short coupons, “helping to reduce expected pressure in the bill market. “

At this point, Hill puts 75% odds on this change occurring by mid-March, meaning that any farcical “debate” whether the Fed’s injection of anywhere between $60 and $100BN in liquidity each month into the equity market, is or isn’t QE, will very soon be mercifully over.

{kind=link}