The Fed Will Ignite The Next “Financial Crisis”

There seems to be a very large consensus the markets have entered into a “permanently high plateau,” or an era in which price corrections in asset prices have been effectively eliminated through fiscal and monetary policy.

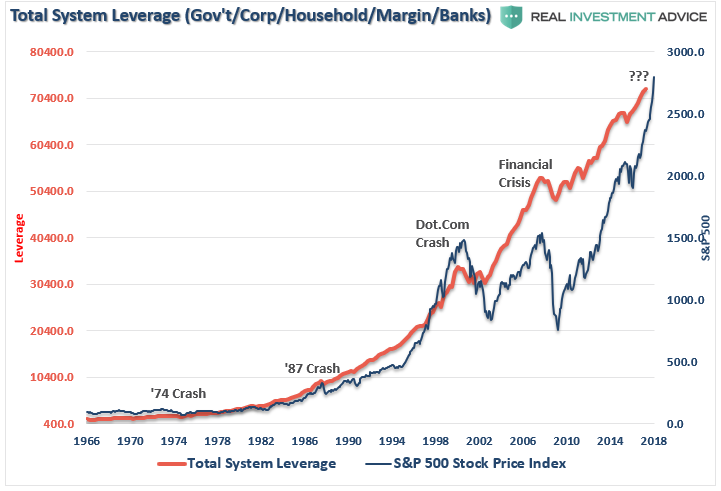

Partnering with this fairytale like mindset is an overwhelming sense of complacency. Throughout the entire monetary ecosystem, there is a rising consensus that “debt doesn’t matter” as long as interest rates remain low. Of course, the ultra-low interest rate policy administered by the Federal Reserve is responsible for the “yield chase” which has fostered a massive surge in debt in the U.S. since the “financial crisis.”

As Ray Dalio, CEO of Bridgewater, recently noted:

“We’re in a perfect situation, inflation is not a problem, growth is good, but we have to keep in mind the part of the cycle we’re in.”

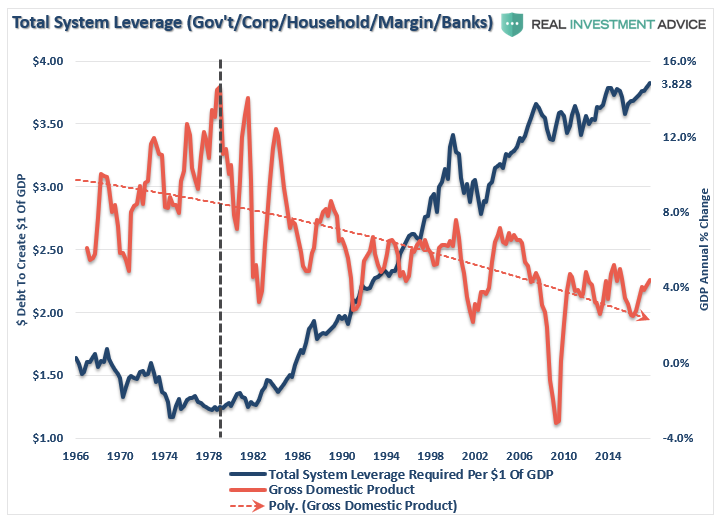

Yes, current economic growth is good, but not great. Inflation and interest rates currently remain low which creates an environment in which using debt remains opportunistic. But rising debt levels has a negative economic consequence. As shown, prior to the deregulation of the financial industry under Ronald Reagan, which led to an explosion in consumer credit issuance, it required just $1.25 of total system-wide debt to create $1.00 of economic growth. Today, it requires $3.83 to create the same $1 of economic growth. This shouldn’t be surprising, given that “debt” detracts from economic growth as the required “debt service” diverts income from savings and productive investment leading to a “diminishing rate of return” for each new dollar of debt.

However, debt levered economic cycles are a function of the ability to draw forward future consumption. But there is a finite limit to the “positive” effect of a debt-driven economic cycle.

Eventually, the “bill” must be paid.

…click on the above link to read the rest of the article…