Central Banks: From Coordination to Competition

This is one reason why I anticipate “unexpected” disruptions in the global economy in 2018.

The mere mention of “central banks” will likely turn off many readers who understandably have little interest in convoluted policies and arcane mumbo-jumbo, but bear with me for a few paragraphs while I make the case for something to happen in 2018 that will impact us all to some degree.

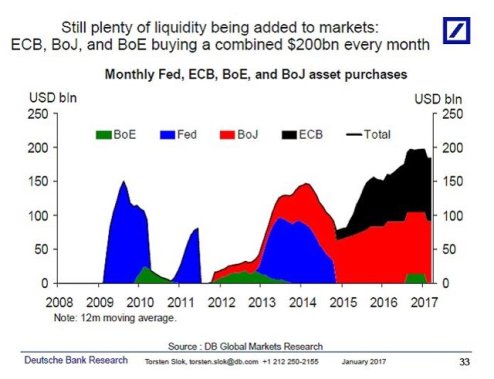

That something is the decay of the synchronized central bank stimulus policies that have pumped trillions of dollars, yuan, yen and euros into the global financial markets over the past nine years. Here are two charts that depict the “tag team” coordinated approach central banks have deployed: when one CB tapers its stimulus, another ramps up its money-creation/asset-purchases stimulus:

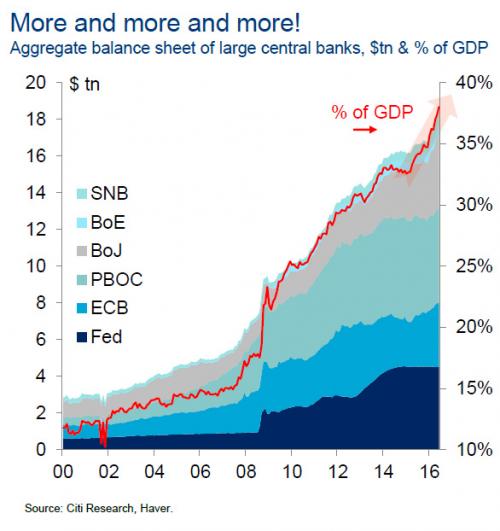

The balance sheets of all the primary central banks added together is astronomical:

This team effort is motivated by self-interest, of course; no one central bank can reflate the entire global economy, and yet that is the only way to reflate each nation/bloc’s own economy, given the global connectedness of the modern economy.

But the threads of mutual self-interest are fraying. At this late stage in the credit cycle, the central banks must begin “tapering”, i.e. diminishing and then ending their stimulus policies and eventually reducing their balance sheets by selling assets they bought in the stimulus phase (or simply stop replacing bonds they own that mature).

The Federal Reserve was first out of the gate in launching quasi-unlimited bond purchases, and it was the first central bank to cease stimulus (quantitative easing) and raise interest rates. It has now signaled that it will begin selling assets (i.e. stop replacing bonds that mature).

…click on the above link to read the rest of the article…