Bank of Japan Tapers (Quietly), QE Party Over

No flashy announcement, to avoid alarming the markets.

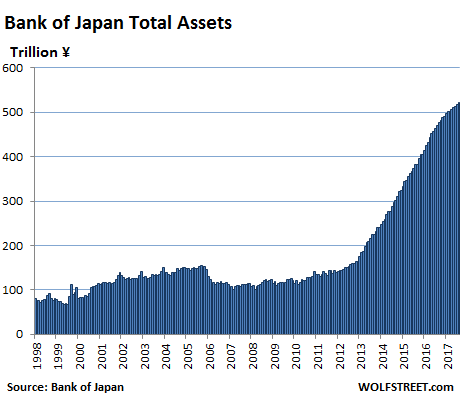

After years of blistering asset purchases, the Bank of Japan disclosed today that it held a total of ¥521.6 trillion in assets as of November 30, including Japanese Government Bonds (JGBs), gold, corporate bonds, Japanese REITs, equity ETFs, loans, etc. That is quite a pile, so to speak. It amounts to about 96% of Japan’s GDP.

By this measure, the BOJ’s balance sheet dwarfs the Fed’s balance sheet, which amounts to 23% of US GDP. When it comes to QE, no one can hold a candle to Japan. Its holdings of JGBs alone rose to ¥443.6 trillion. Its balance sheet looks like a typical post-Financial-Crisis central-bank balance sheet on steroids (chart in trillion yen):

There a couple of differences compared to other central banks: One, the BOJ started QE long before anyone even called it “QE,” but in 2013, it really got going, and those giant moves made the prior periods of QE look minuscule. And two, the BOJ actually unwound some of its earlier QE starting in late 2005 but soon gave up on it.

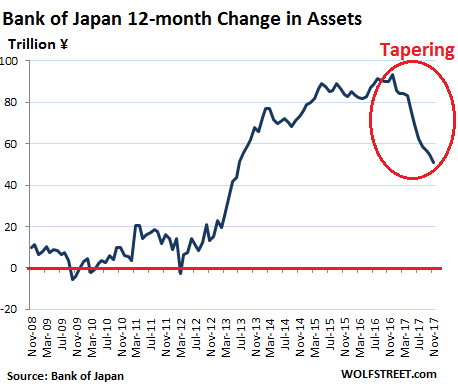

Now something else has been happening: Starting in December 2016 – the month the Fed raised rates and a few months after some Fed governors started to kick around the idea publicly that QE should be unwound – the BOJ began to curtail its asset purchases.

In other words, it began to “taper.” Assets are still increasing but at a much slower rate. During peak QE – the 12-month period ending December 31, 2016 – it added ¥93.4 trillion (about $830 billion) to its balance sheet. Over the 12-month period ending November 30, 2017, it has added “only” ¥50.8 trillion to its balance sheet. Though that’s still a good chunk of money (about $450 billion), that addition is down 46%.

This chart shows the 12-month change in the balance sheet in trillion yen, going back to the Financial Crisis:

…click on the above link to read the rest of the article…