Technically Speaking: The Markets Next “Minsky Moment”

In this past weekend’s newsletter, I discussed the issue of the markets next “Minsky Moment.” Today, I want to expand on that analysis to discuss how the Fed’s drive to create “stability” eventually creates “instability.”

In 2007, I was at a conference where Paul McCulley, who was with PIMCO at the time, discussed the idea of a “Minsky Moment.” At that time, this idea fell on “deaf ears” as markets were surging higher amidst a real estate boom. However, it wasn’t too long before the 2008 “Financial Crisis” brought the “Minsky Moment” thesis to the forefront.

So, what exactly is a “Minsky Moment?”

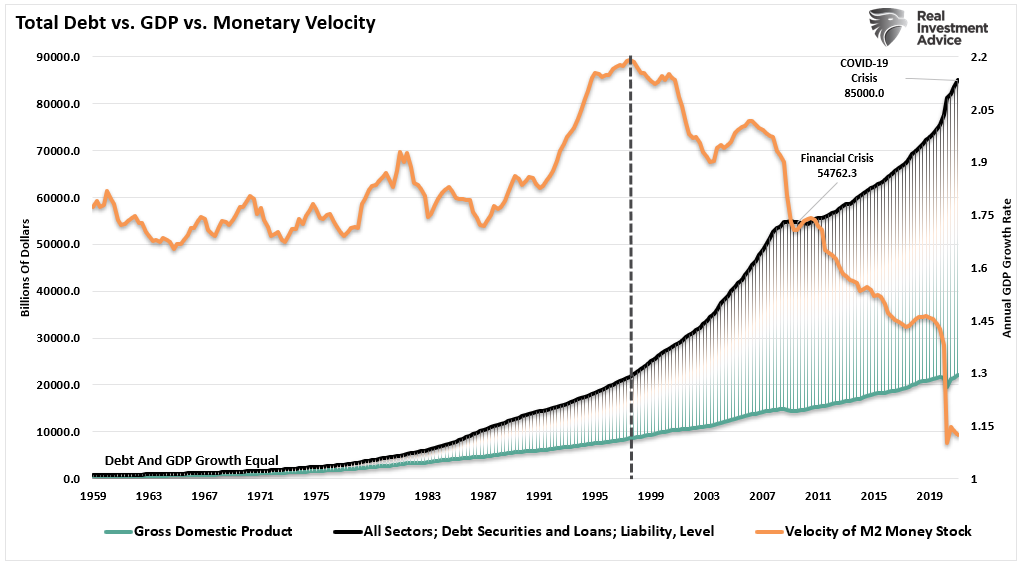

Economist Hyman Minsky argued that the economic cycle is driven more by surges in the banking system and credit supply. Such is different from the traditionally more critical relationship between companies and workers in the labor market. Since the Financial Crisis, the surge in debt across all sectors of the economy is unprecedented.

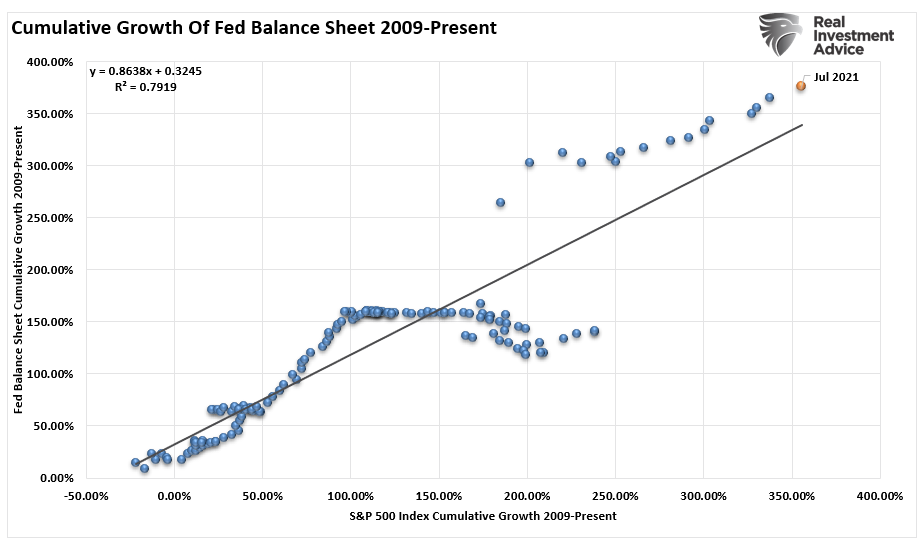

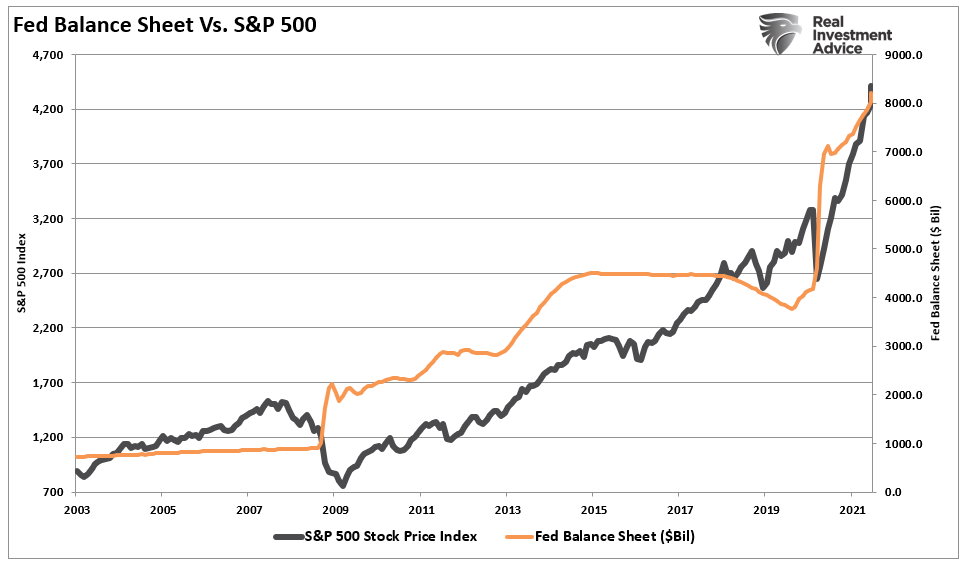

Importantly, much of the Treasury debt is being monetized, and leveraged, by the Fed to, in theory, create “economic stability.” Given the high correlation between the financial markets and the Federal Reserve interventions, there is credence to Minsky’s theory. With an R-Square of nearly 80%, the Fed is clearly impacting financial markets.

Those interventions, either direct or psychological, support the speculative excesses in the markets currently.

Bullish Speculation Is Evident

Minsky’s specifically noted that during periods of bullish speculation, if they last long enough, the excesses generated by reckless, speculative activity will eventually lead to a crisis. Of course, the longer the speculation occurs, the more severe the problem will be.

Currently, we see clear evidence of “bullish speculation” from:

…click on the above link to read the rest of the article…