Chinese Media Stunner: China Will Be The Next Country To Cut Rates To Zero

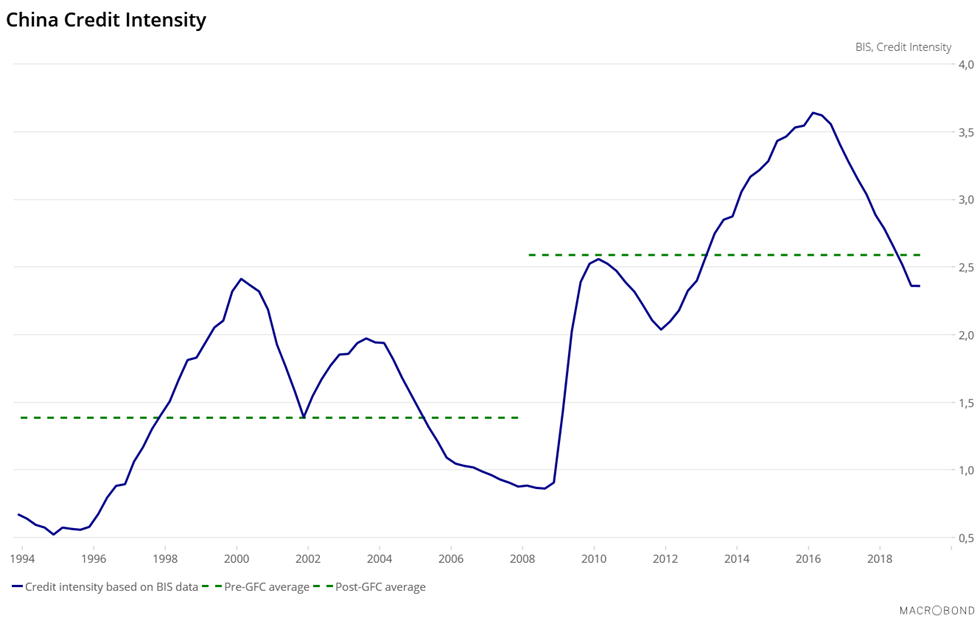

One week ago, we showed in one chart why the global economic recovery that so many expect is just a few months away, won’t happen: as the chart below shows, China’s credit intensity since 1994 has exploded. This means that before the Global Financial Crisis, China needed on average one unit of credit to create one unit of GDP. Since 2008, 2½ units of credit are required to create one unit of GDP. In other words, that China needs much more credit than 10 years ago to have the exact same amount of GDP. Injecting more credit in the economy is not the miracle solution it used to be, and the disadvantages of credit push tend to surpass the advantages.

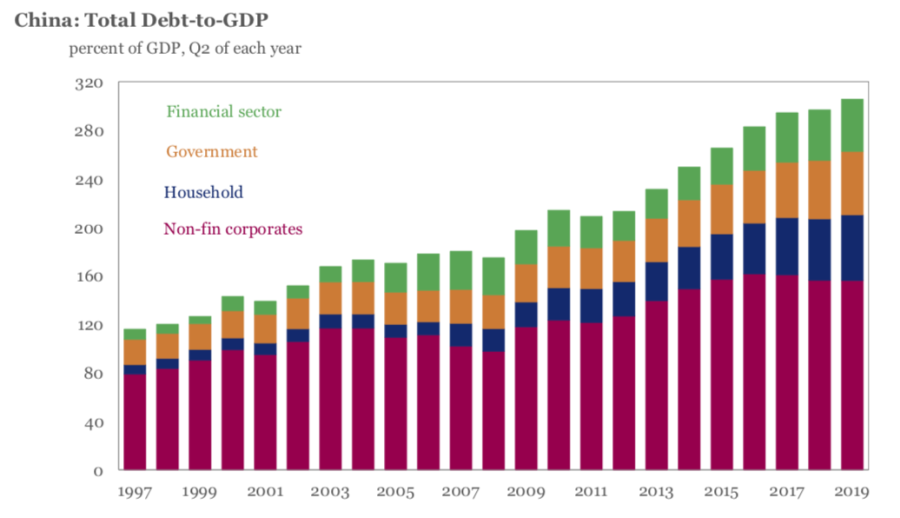

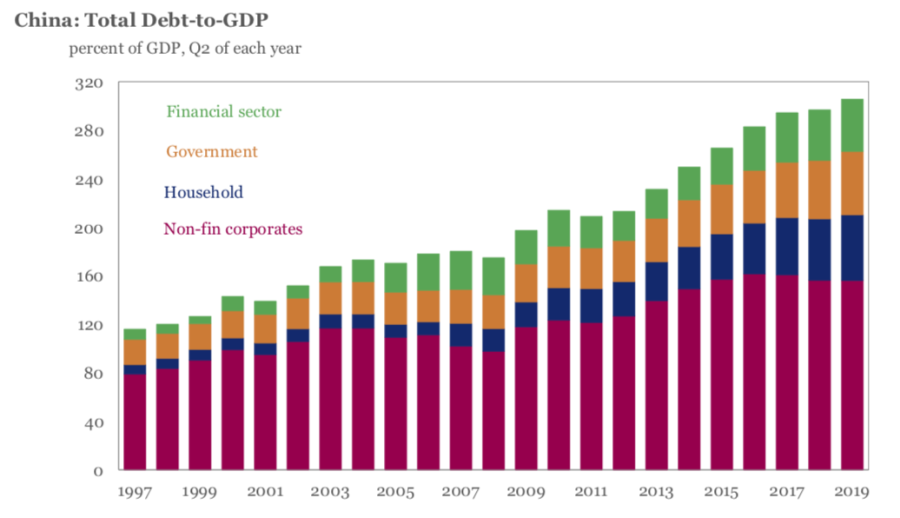

This explosion in China’s credit intensity in the past decade has directly fueled China’s debt engine, the same debt engine that single-handedly pulled the world out of a global depression in 2008/2009. Alas, this will not happen again: China’s public and household debts are at their highest historical levels, respectively at 51% of GDP and 53% of GDP, and the private sector debt service ratio is becoming a burden for many companies, reaching on average 19.7% This records an increase from 13% before the crisis. Overall, China’s debt to GDP is fast approaching an unprecedented 320%!

Which brings us to Saxo’s dour conclusion for all those who believe that the global economy is about to enjoy another period of sustainable growth (and has confused the Fed’s QE for economic resilience and fundamentals):

Contrary to previous periods of slowdown, notably in 2008-2010, 2012-2014 and in 2016, China is unlikely to save the global economy once again.

…click on the above link to read the rest of the article…

{kind=link}