The Market’s Biggest Risk: A Stagflationary Shock

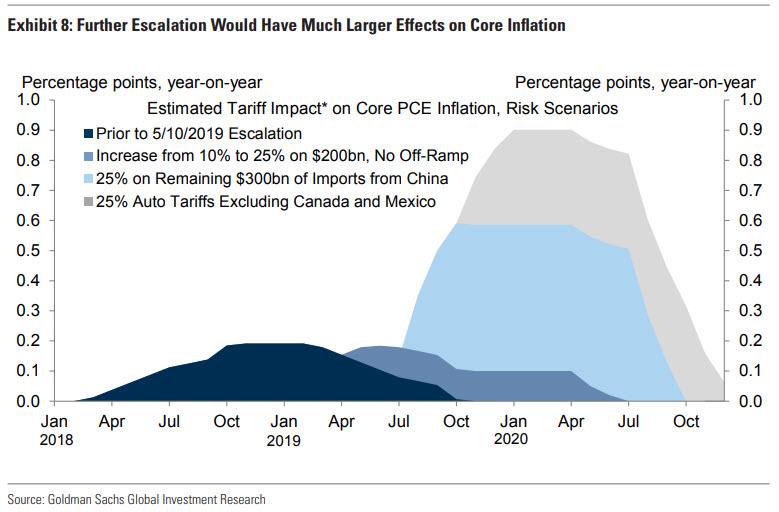

Nearly three weeks ago, when Goldman calculated that the imminent impact of even more tariff hikes (back then Trump’s intention to slap Mexico with tariffs wasn’t known yet) would be to sharply boost inflation as imposing 25% tariffs on roughly $300bn of remaining Chinese imports would have a peak effect of 0.5pp on core PCE, while auto tariffs would have a roughly 0.3pp peak effect…

… we said that “the unspoken risk here is clear: stagflation. Indeed, further escalation of the trade war could result in a hit to GDP as large as 0.4%, and if trade tensions sparked a major sell-off in the equity market the growth impact could worsen considerably, as virtually nobody is prepared for a stagflationary outcome.

Now, in his latest note to clients after a 1 week travel to Asia hiatus, Nomura’s Charlie McElligott writes that the mood/ overall market sentiment is anecdotally approaching “max bearish” on both global economic prospects- and risk-assets-, with investors certain that the “trade war” is going to worsen in coming-months, with no relief in-sight and expecting a “long war” with China playing hard-ball into the US Election:

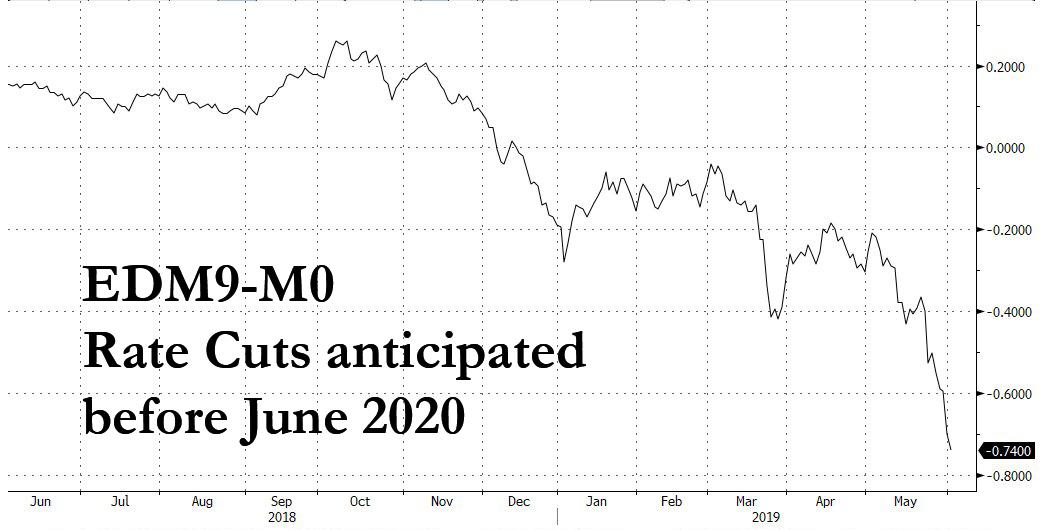

The good news, according to McElligott, is that his Treasury curve steepening view keeps bull steepening, with now greater than 3 Fed cuts implied before next June 2020, “as the market has moved from “growth scare”- to now “outright recession”- pricing on the new multi-fronted trade war & tariff escalation.”

The “perverse” news? This is where the Nomura strategist reminds us of what we said in mid-May, namely that the risk is that with the market now fully positioned for a deflationary shock, the outcome will be diametrically opposite. Here’s Charlie:

…click on the above link to read the rest of the article…