CAPITAL FLOWS – IS A RECKONING NIGH?

- Borrowing in Euros continues to rise even as the rate of US borrowing slows

- The BIS has identified an Expansionary Lower Bound for interest rates

- Developed economies might not be immune to the ELB

- Demographic deflation will thwart growth for decades to come

In Macro Letter – No 108 – 18-01-2019 – A world of debt – where are the risks? I looked at the increase in debt globally, however, there has been another trend, since 2009, which is worth investigating as we consider from whence the greatest risk to global growth may hail. The BIS global liquidity indicators at end-September 2018 – released at the end of January, provides an insight: –

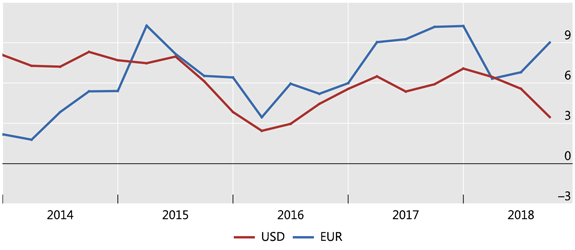

The annual growth rate of US dollar credit to non-bank borrowers outside the United States slowed down to 3%, compared with its most recent peak of 7% at end-2017. The outstanding stock stood at $11.5 trillion.

In contrast, euro-denominated credit to non-bank borrowers outside the euro area rose by 9% year on year, taking the outstanding stock to €3.2 trillion (equivalent to $3.7 trillion). Euro-denominated credit to non-bank borrowers located in emerging market and developing economies (EMDEs) grew even more strongly, up by 13%.

The chart below shows the slowing rate of US$ credit growth, while euro credit accelerates: –

Source: BIS global liquidity indicators

The rising demand for Euro denominated borrowing has been in train since the end of the Great Financial Recession in 2009. Lower interest rates in the Eurozone have been a part of this process; a tendency for the Japanese Yen to rise in times of economic and geopolitical concern has no doubt helped European lenders to gain market share. This trend, however, remains over-shadowed by the sheer size of the US credit markets. The US$ has remained preeminent due to structurally higher interest rates and bond yields than Europe or Japan: investors, rather than borrowers, dictate capital flows.

…click on the above link to read the rest of the article…