Here Comes The Shanghai Accord 2.0: China Unleashes Gargantuan Credit Injection To Start 2019

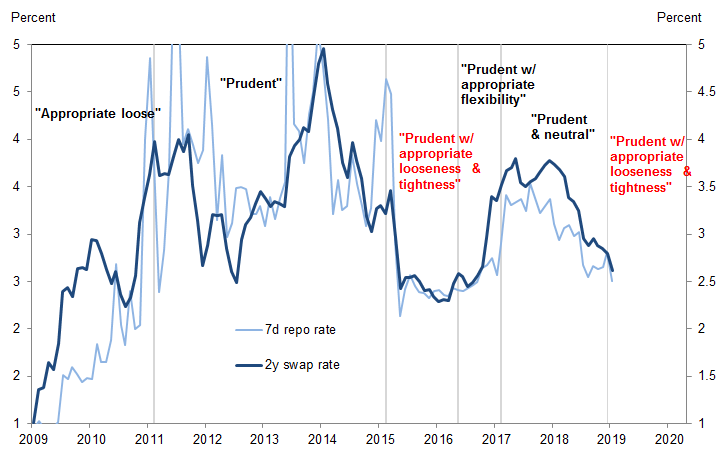

One month ago, we pointed out a curious shift in the official language out of China’s central bank: in late December, when traders were generally away on vacation, the PBOC indicated a critical shift in the official monetary policy description at the December Central Economic Work Conference, from “prudent and neutral” to “prudent with appropriate looseness and tightness”.

What caught our attention is that the new description was surprisingly similar to what was adopted in 2015, just as monetary policy eased significantly and ahead of the famous “Shanghai Accord” of January 2016 when, as the world was careening to a bear market, a coordinated response from G-7 leaders and China sparked a massive rally in stocks as China unleashed another massive credit injection burst which impacted the global economy for the next year. As Goldman said at the time, “such official policy language, while subtle, can carry important information about the monetary policy stance.”

Which is why in January we said that “while traders were focusing on the latest words out of Fed Chair Powell, is the real “risk-on” catalyst the hint out of China that a new “Shanghai Accord” may be imminent” and added that “the answer is most likely yes, especially if the upcoming US-China trade talks fail to yield a favorable outcome, as the alternative would be even more pain for China’s economy.”

One month later we got the answer when China overnight reported its latest credit aggregate data, and it was a doozy.

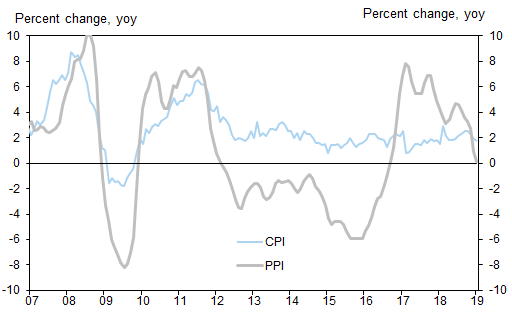

While the market’s attention may have been focused on that “other” news reported by China overnight, namely yet another disappointing month of CPI and PPI, as China’s CPI inflation eased further to 1.7% Y/Y in January from 1.9% in December, while PPI inflation moderated further to just barely above deflation territory, printing at 0.1% yoy in January, the lowest since October 2016…

…click on the above link to read the rest of the article…