Subprime Rises: Credit Card Delinquencies Blow Through Financial-Crisis Peak at the 4,705 Smaller US Banks

So what’s going on here?

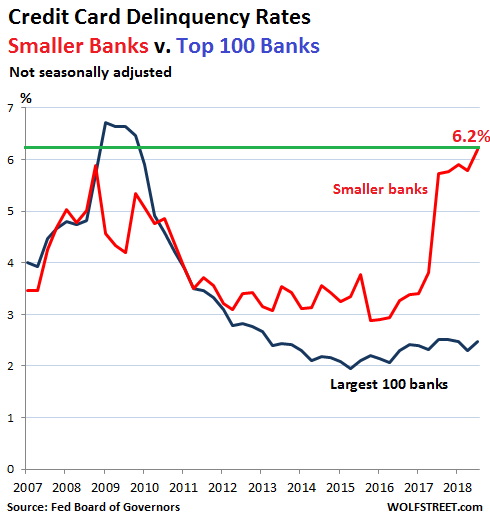

In the third quarter, the “delinquency rate” on credit-card loan balances at commercial banks other than the largest 100 banks – so the delinquency rate at the 4,705 smaller banks in the US – spiked to 6.2%. This exceeds the peak during the Financial Crisis for these banks (5.9%).

The credit-card “charge-off rate” at these banks, at 7.4% in the third quarter, has now been above 7% for five quarters in a row. During the peak of the Financial Crisis, the charge-off rate for these banks was above 7% four quarters, and not in a row, with a peak of 8.9%

These numbers that the Federal Reserve Board of Governors reportedMonday afternoon are like a cold shower in consumer land where debt levels are considered to be in good shape. But wait… it gets complicated.

The credit-card delinquency rate at the largest 100 commercial banks was 2.48% (not seasonally adjusted). These 100 banks, due to their sheer size, carry the lion’s share of credit card loans, and this caused the overall credit-card delinquency rate for all commercial banks combined to tick up to a still soothing 2.54%.

In other words, the overall banking system is not at risk, the megabanks are not at risk, and no bailouts are needed. But the most vulnerable consumers – we’ll get to why they may end up at smaller banks – are falling apart:

Credit card balances are deemed “delinquent” when they’re 30 days or more past due. Balances are removed from the delinquency basket when the customer cures the delinquency, or when the bank charges off the delinquent balance. The rate is figured as a percent of total credit card balances. In other words, among the smaller banks in Q3, 6.2% of the outstanding credit card balances were delinquent.

…click on the above link to read the rest of the article…