QR 3/2018: How the Eurozone breaks

The Eurozone is a fragile financial mammoth. While its GDP lacks the US by around $3 trillion, assets of the banking sector are some 240 percent of GDP vs. around 90 percent in the US. It has been kept standing only through the large-scale asset purchase program (quantitative easing or QE) of the ECB. However, the ECB is about to phase-out its bond buying program, which will affect the debt dynamics and the likelihood of euro survival in a dramatic way.

The tragedy of the Eurozone in three acts

The Eurozone has been built on quicksand. The examples of more than 200 former currency unions suggests rather vividly that a currency union needs to be either backed by a political union or it needs to have an exit option. The eurozone, markedly, has neither.

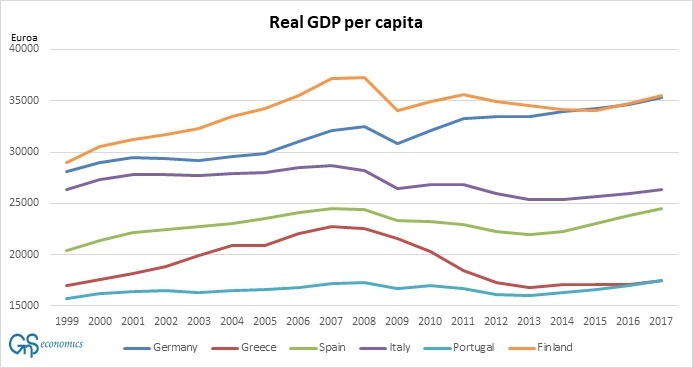

It was erroneously assumed that when countries join the European Monetary Union (EMU), their economies would start to converge. This means that it was thought that the poorer countries would start to catch-up to the richer ones in well-being and, e.g., productivity. That never materialized. The convergence that was observable during the first years of the euro halted after the financial crisis hit (see the Figure below).

Figure 1. Real (constant) gross domestic product per capita in selected Eurozone countries. Source: GnS Economics, European Commission

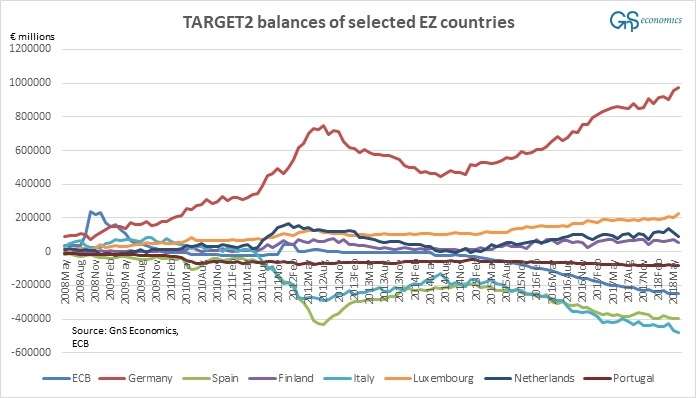

After the crisis of 2008, capital started to flee from the weaker member countries of the EZ (see Figure 2 below). When the run on the capital account of Greece, Ireland, Portugal and Spain started to accelerate in 2011, it pushed them on the verge of an default. Their sovereign defaults threatened to bring down major banks, especially in France and Germany. There was also a risk that defaulting countries would be forced to return to their own currency to support their banking system.

…click on the above link to read the rest of the article…