HELOCs in the US & Canada: As “Scarred” Americans Learned Bitter Lesson, Canadians Went Nuts

Home-equity-loan balances in Canada per capita are now 3.3 times what they were in the US during HELOC peak before it all collapsed.

Home Equity Lines of Credit – the infamous HELOCs Americans used as endless ATMs to draw equity out of their homes before home prices collapsed – played a role in the US mortgage crisis. And Americans have learned a lesson since, despite mega-efforts by the industry to revive HELOCs.

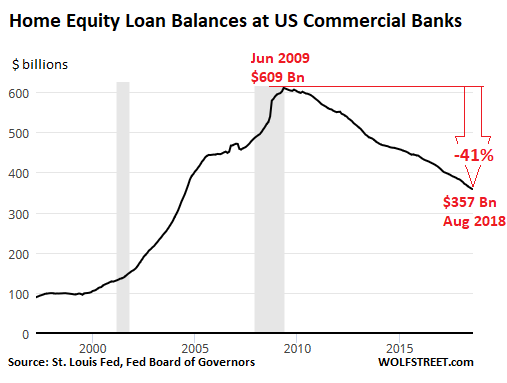

Balances of revolving home equity loans at US commercial banks soared by about 300% in seven years, from $154 billion at the beginning of 2002 right into the crisis, peaking in June 2009 at $609 billion. As the housing-and-mortgage crisis blew those dreams of the endless ATM apart, Americans learned their lessons, either defaulting on, or paying down, their HELOCs. At the end of August, HELOC balances had fallen 41% from the peak, to $357 billion – back where they’d been in 2004 on the way up – even as aggregate home values now exceed the peak of Housing Bubble 1:

This near-decade-long decline triggered lamentations by William Dudley last year, when he was still president of the New York Fed, that Americans weren’t borrowing enough against their homes, and that they therefore were too lackadaisical in their job of boosting consumer spending with borrowed money.

In Canada there is no such reluctance. That makes sense because Canadians had skipped the housing bust that Americans had gone through. Instead, the Canadian home-price surge, after a brief dip during the Financial Crisis, continued until 2017 and in the process became one of the wildest and scariest housing bubbles in the world. And Canadians are loving their endless home-equity ATMs.

…click on the above link to read the rest of the article…