I was given a lecture in Toronto to our institutional clients years ago and the central bank of Canada came with ten people. It was an interesting session because the audience began to ask me questions about what the central banks were looking at to make their decisions. I would answer and then the audience would immediately turn to see their response. It was a really fascinating session that turned me into this quasi-spokesperson for the central banks. I would respond and usually swat down these absurd theories one after another. The head of the Bank of Canada I knew well and the whole table was unbelievable poker-players. They never flinched nor did you get any read from any body language. When it was over, I went up to them and apologized saying I hoped I did not insult them in any way. They reply was astounding: “Marty, I only wish I could tell these fools we do not look at this stuff!”

People attribute the central banks will also sort of theories you would think they were the all-powerful demigods of finance. Decoding what a central bank says is very important. Yet I find all the commentary to be so off the mark it is laughable. The new word the Fed likes to use is its increasing reliance on “transitory” factors to explain the past six-year problem of being unable to reach the Fed’s 2% inflation target. They explain the failure with “transitory price changes” in some components such as health care and financial services. That was in their minutes from the May 1-2, 2018 meeting. When you look closely, price changes become “transitory” on the downside as well as “transitory”when they move on the upside. Indeed, they love to explain trends as “transitory” for that avoids any permanent trend forecast.

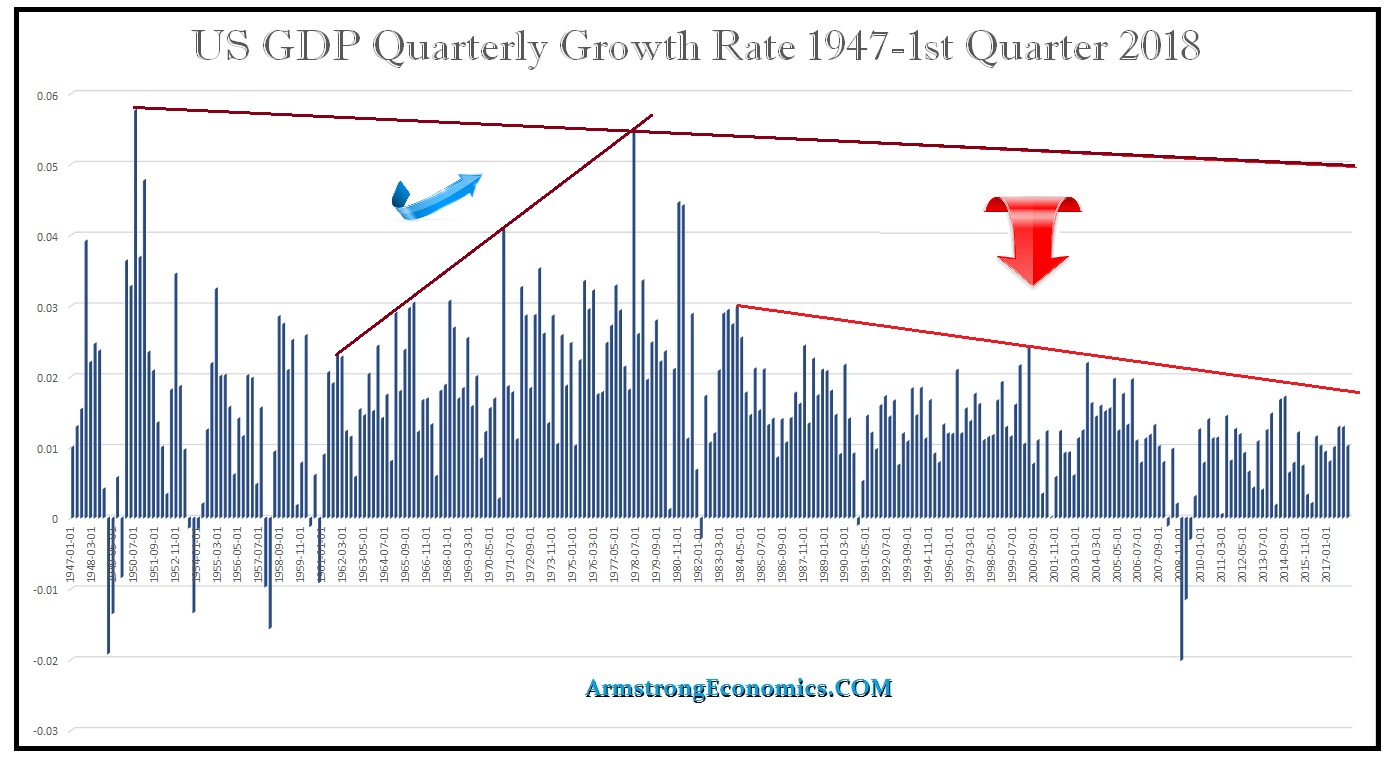

…click on the above link to read the rest of the article…