The Fed’s QE-Unwind is Really Happening

Fed’s assets drop to lowest level in over three years.

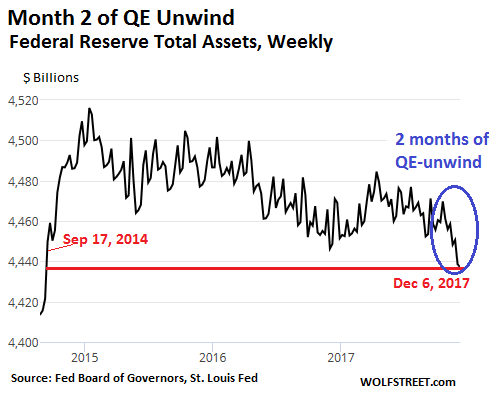

The Fed’s balance sheet for the week ending December 6, released today, completes the second month of the QE-unwind. Total assets initially zigzagged within a tight range to end October where it started, at $4,456 billion. But in November, holdings drifted lower, and by December 6 were at $4,437 billion, the lowest since September 17, 2014:

“Balance sheet normalization?” Well, in baby steps. But the devil is in the details.

The Fed’s announced plan is to shrink the balance sheet by $10 billion a month in October, November, and December, then accelerate the pace every three months. By October 2018, the Fed would reduce its holdings by up to $50 billion a month (= $600 billion a year) and continue at that rate until it deems the level of its holdings “normal” – the new normal, whatever that may turn out to be.

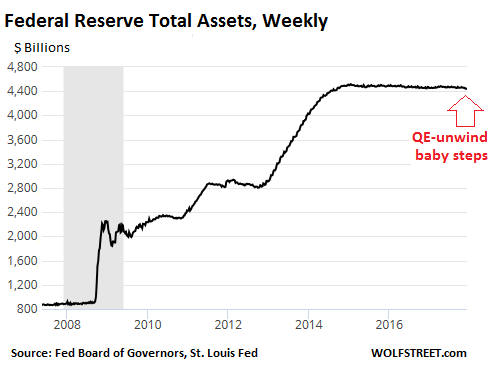

Still, the decline so far, given the gargantuan size of the balance sheet, barely shows up:

The Fed is unloading its Treasuries alright.

As part of the $10-billion-a-month unwind from October through December, the Fed is supposed to unload $6 billion in Treasury securities a month plus $4 billion in mortgage-backed securities (MBS) a month.

The Fed doesn’t actually sell Treasury securities outright. Instead, it allows some of them, when they mature, to “roll off” the balance sheet without replacement. When the securities mature, the Treasury Department pays the holder the face value. But the Fed, instead of reinvesting the money in new Treasuries, destroys the money – the opposite process of QE, when the Fed created the money to buy securities.

This happens only on dates when Treasuries that the Fed holds mature, usually once or twice a month.

…click on the above link to read the rest of the article…