- The IMF revised Chinese growth forecasts higher in July – were they premature?

- Retail sales, industrial output and fixed investment have slowed

- The Real Estate sector is still buoyant but home price increases are moderating

- Narrow money supply growth has slowed, other parts of the economy will follow

China has long been the marginal driver of demand for a wide array of commodities. In an attempt to understand the recent rise in the price of industrial metals, the strength of Chinese demand is a key factor. The picture is mixed.

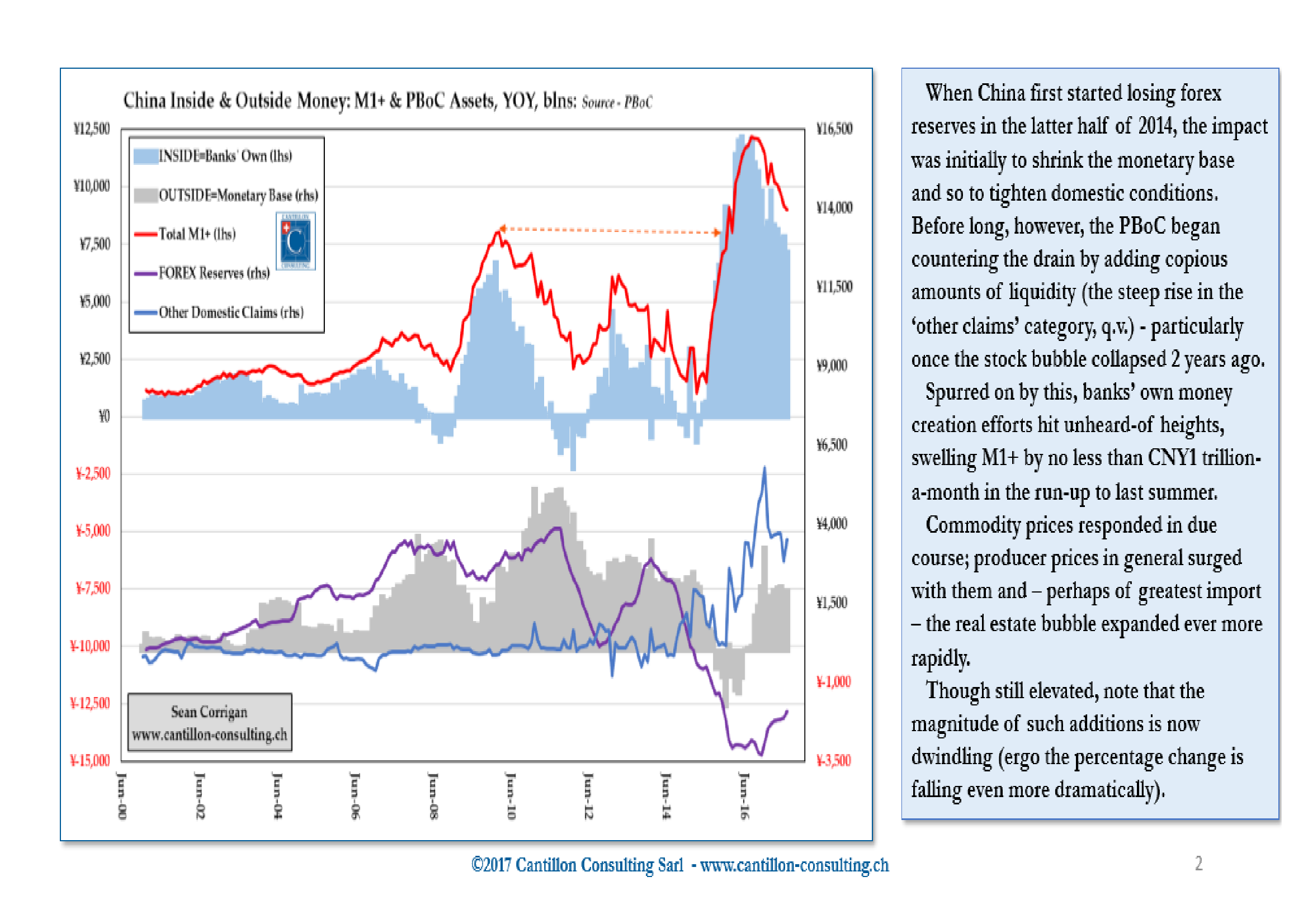

The chart and commentary below is taken from Sean Corrigan’s August newsletter – Cantillon Consulting – China: Is the tide turning?:-

Source: Cantillon Consulting

As Corrigan goes on to say:-

As the deceleration has progressed, the PMI has shown its expected downward response. In due course, company revenues – and ultimately profits – will follow if this is long maintained.

Greater recourse to receivables financing (funded partly by recourse to shadow finance) can delay full recognition of this awhile, but it cannot fail to impair either the magnitude or the quality of earnings as it works through the economy.

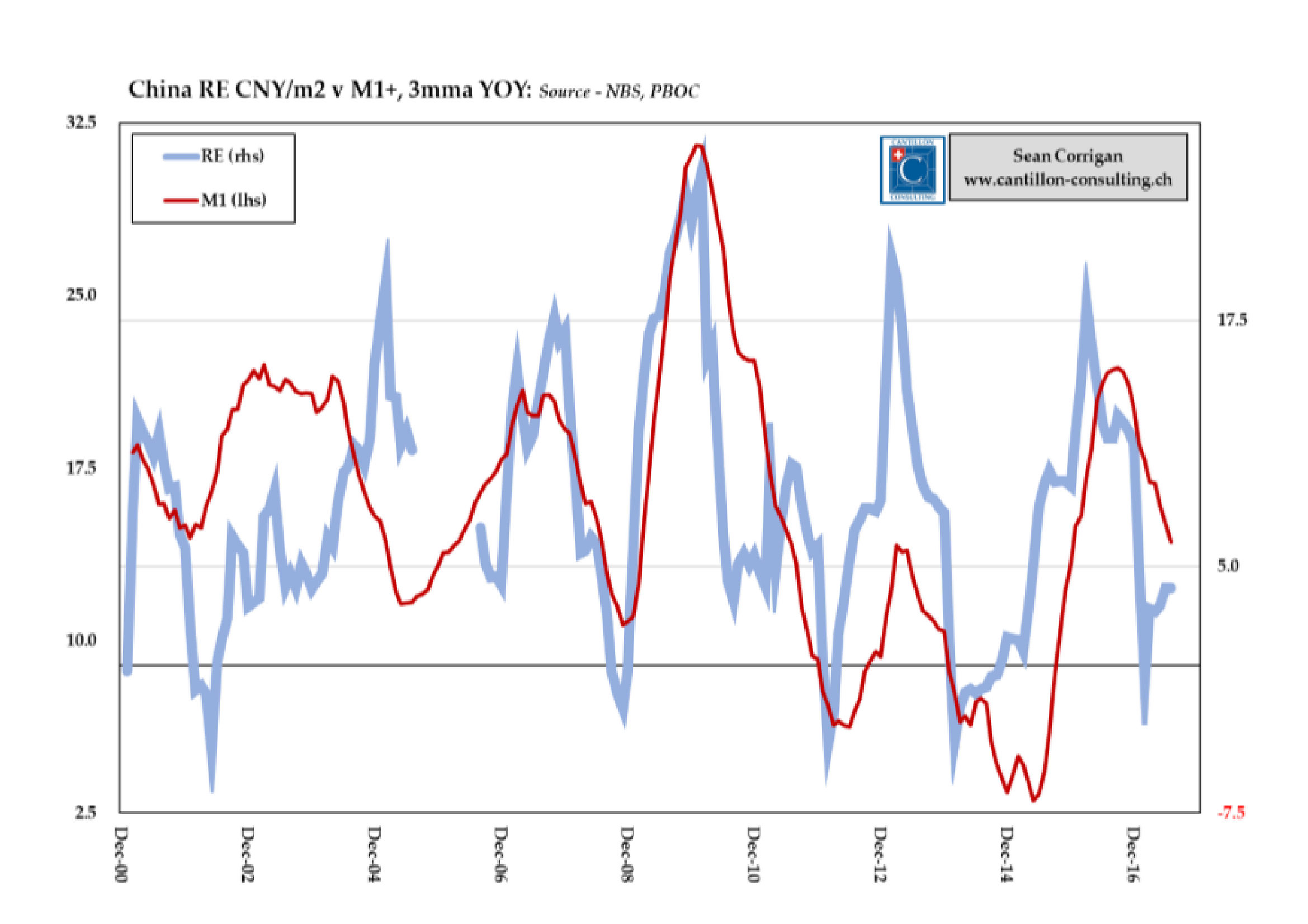

At the heart of the credit equation lies the Real Estate market:-

Source: Cantillon Consulting

During 2016 property prices in China increased by 19%, new homes by 12.4%, the fastest since 2011, but the market has cooled of late due to government intervention to subdue its speculative excess. New-home prices, excluding government-subsidized housing, gained from the previous month in 56 of 70 cities in July, compared with 60 in June. New Home Sales for August were the weakest in three years at +3.8%, however, investment in Real Estate development increased 7.8% last month – this is hardly a collapse. House prices are still forecast to rise by 6.8% in 2017 with growth driven by continued increases in second and third tier cities:-

…click on the above link to read the rest of the article…