ECB, Monetarism and a Greek Half-Decade

Greece really should not matter, at all, outside of the tragic plight of the Greeks themselves. You’ll see that message echoed particularly inside the US where the status quo takes a contradictory turn toward reasonableness in order to justify further what isn’t. This is all about asset prices and how they have been so skewed almost everywhere that when one part of that systemic imbibing threatens to pull back the curtain the rest works overdrive to convince that it doesn’t matter.

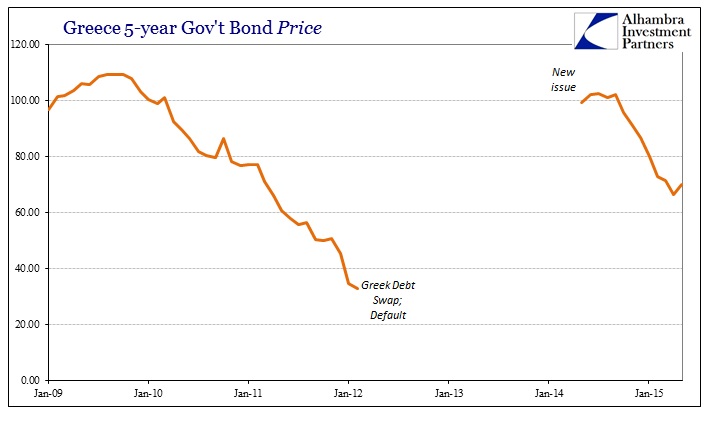

Just fourteen months ago, then-Prime Minister of Greece, Antonis Samaras, went on Greek television and confidently proclaimed, “Today, Greece took one more decisive step to exit the crisis. Confidence in our country was confirmed by the most objective judge – the markets.” Going further, then-Deputy Prime Minister Evangelos Venizelos objected to any other interpretation, “The bond issue proves the debt is sustainable, otherwise the markets wouldn’t have bought it.”

Obviously, those were political statements intended to send a political message in that the “objective” market was on the side of that current Greek political makeup and the “austerity” track into which they proclaimed to be amalgamated, inextricably within the euro currency. Under rational expectations theory, of course, the price with which the Greeks floated that bond was believed to be “correct” and thus efficient. The 4.95% yield at the auction, 20 times oversubscribed, certainly seemed to suggest that it was “market clearing” in at least that respect.

The problem with all of that view is apparent right now. The 5-year bond, after having a pretty good week last week with all the false deal rumors, is yielding this morning almost 23%. The losses embedded in that yield and its price were uniquely predictable, which is what is so damning about Greece as it relates to everything outside of the “small country on the Aegean.”

…click on the above link to read the rest of the article…