Bear Market Growls As Market Remains Weak

Several months ago, I penned an article about the problems with “passive indexing” and specifically the problem of the “algorithms” that are driving roughly 80% of the trading in the markets. To wit:

“When the ‘robot trading algorithms’ begin to reverse (selling rallies rather than buying dips), it will not be a slow and methodical process, but rather a stampede with little regard to price, valuation, or fundamental measures as the exit will become very narrow.”

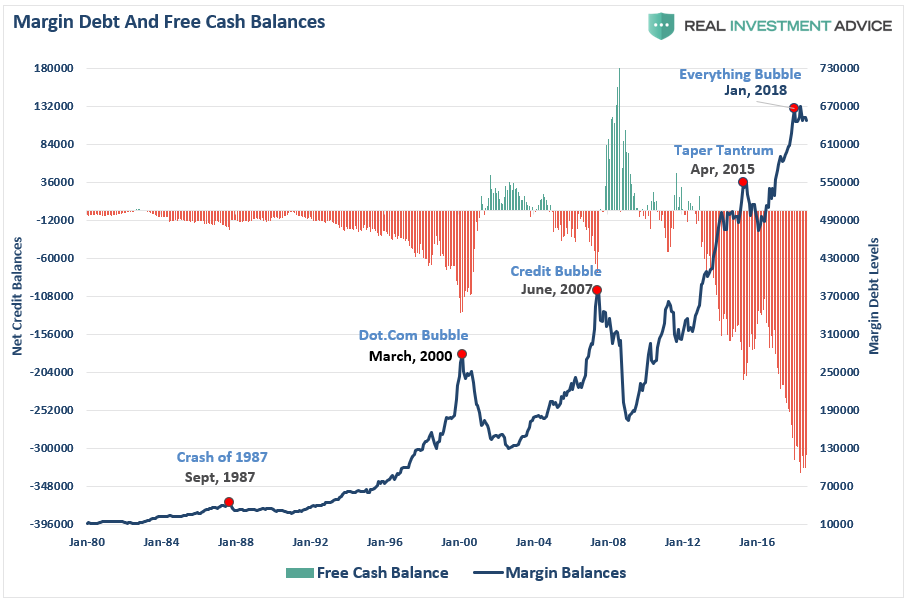

Fortunately, up to this point, there has not been a triggering of margin debt, as of yet, which remains the “gasoline”to fuel a rapid market decline. As we have discussed previously, margin debt (i.e. leverage) is a double-edged sword. It fuels the bull market higher as investors “leverage up” to buy more equities, but it also burns “white hot”on the way down as investors are forced to liquidate to cover margin calls. Despite the two sell-offs this year, leverage has only marginally been reduced.

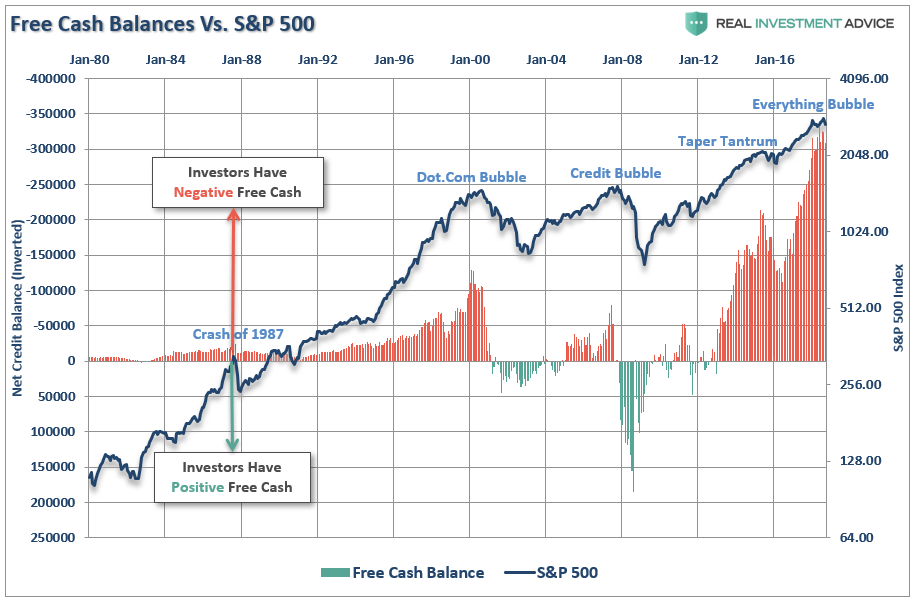

If you overlay that the S&P 500 index you can see more clearly the magnitude of the reversions caused by a “leverage unwind.”

The reason I bring this up is that, so far, the market has not declined enough to “trigger” margin calls.

At least not yet.

But exactly where is that level?

There is no set rule, but there is a point at which the broker-dealers become worried about being able to collect on the “margin lines” they have extended. My best guess is that point lies somewhere around a 20% decline from the peak. The correction from intraday peak to trough in 2015-2016 was nearly 20%, but on a closing basis, the draft was about 13.5%. The corrections earlier this year, and currently, have both run close to 10% on a closing basis.

…click on the above link to read the rest of the article…