Is The Oil Burden A Rising Problem?

While markets become increasingly bullish, oil prices are close to a “warning zone” where the barrel could be one -if not the only- catalyst of a major slowdown.

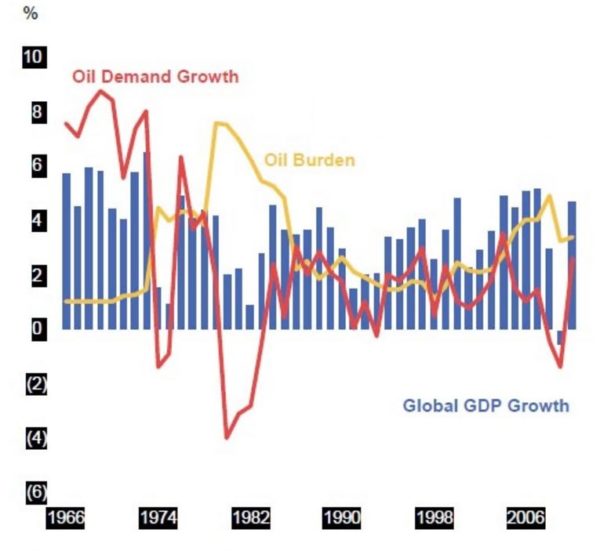

In my book “Escape from the Central Bank Trap”, I explain the concept of the “Oil Burden”. It is the percentage of global GDP spent on buying oil. It is often said that when the oil burden reaches 5-6% of GDP it can be a cause of a global slowdown.

The mistake that many make is to think that the oil burden is a cause and not a symptom.

In the past, we have seen that a period of abrupt increases in oil prices was followed by a recession or a crisis. However, not because oil prices rose rapidly, but because the dramatic increase in commodities’ prices was caused by a bubble of credit and excess monetary stimuli.

In reality, the oil burden is perfectly manageable at 5% of GDP because the energy intensity of GDP growth is diminishing. We are less dependent on energy to create growth in the economy.

Global energy intensity (total energy consumption per unit of GDP) declined by 1.2% in 2017, slightly below its historical yet unstoppable trend (-1.5%/year on average between 2000 and 2017 and -1.8% in 2016). In fact, global energy intensity is down 54% since 1990.

So the problem is not the oil burden by itself but the cause of the price spike.

When oil prices rise abruptly we should be concerned, because they can cause a domino effect on the real economy. When the reason for the price increase is not fundamental, we have a major problem.

Why are oil prices rising abnormally in recent months?

…click on the above link to read the rest of the article…