The Case For Gold Is Not About Price

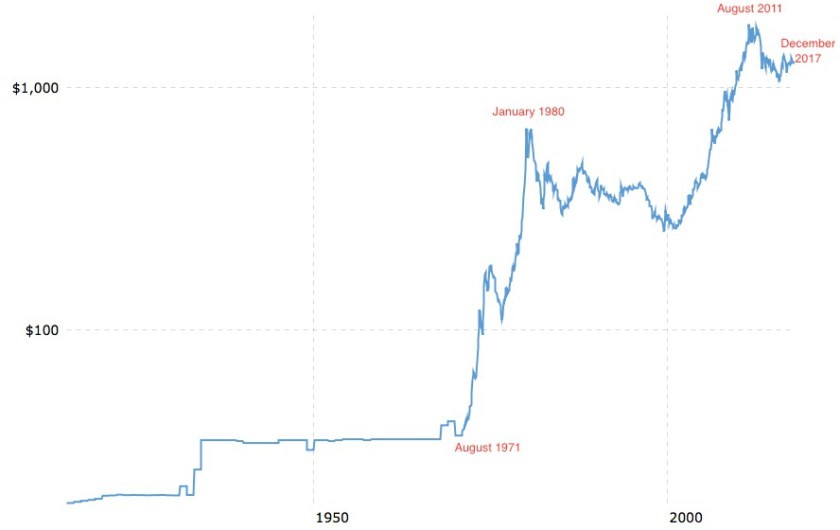

Between the years 1971 and 2011, the price of gold went from $42.00 per ounce to $1900.00 per ounce – a forty-five-fold increase. This is depicted on the chart below…

(Click to enlarge)

Looking at the chart, it would appear that gold is in a long-term bull market and that continually higher prices over time can be expected. Proponents of this approach to gold cite fundamentals such as a weakening U.S. dollar, social unrest, wars (combat and trade), political instability, etc.

And the numbers seem to bear this out. For the forty-year period between August 1971 and August 2011, the price of gold was up forty-four hundred percent.

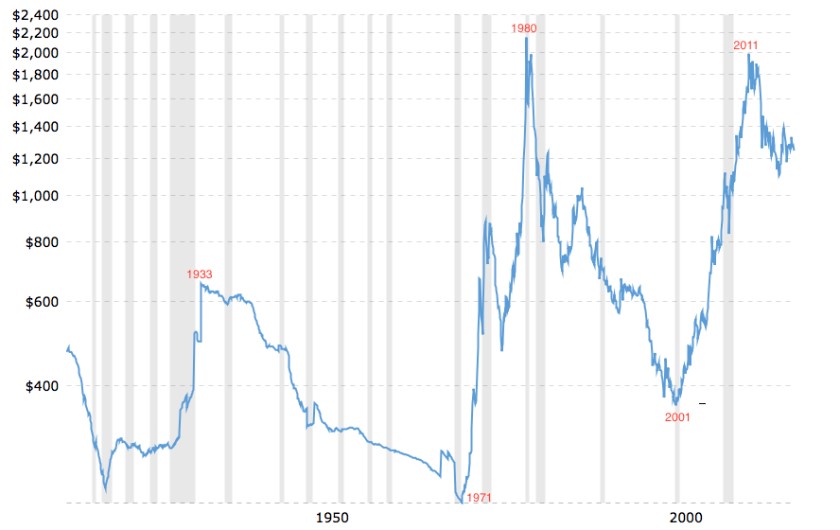

But are we really making any money? The chart below paints a clearer picture…

(Click to enlarge)

The inflation-adjusted chart immediately above seems to support a severely modified view of gold from that which we mentioned earlier. Rather than long-term, ever-higher, onward and upward, we see strictly defined periods of extreme volatility. Indeed, it appears almost cyclical.

And our previous total return of 4,400 percent for the forty-year period August 1971 to August 2011, is reduced to 900 percent. Even so, that is the equivalent of a 6% average annual return, net of inflation. Which is huge.

(In case you are interested, the average annual return for the S&P 500 – with dividends reinvested – for the same exact time period, is 5.13 percent. That relatively small differential on an annual basis is magnified considerably when you compare cumulative total returns: Gold at 900% vs. S&P 500 at 639%)

So, does the nine hundred percent total return/6% annual return represent a profit? Yes, most definitely. Net of the effects of inflation, the price of gold increased ten-fold; all of which represents added value. Here’s why…

In 1971, the cost for one loaf of bread was $.24. The average cost for one gallon of gasoline was $.36. With gold at $42.00 per ounce, you could purchase one hundred

…click on the above link to read the rest of the article…