The Central Banks Face Unwelcome Realities: Their Policies Boosted Wealth Inequality and Failed to Generate “Growth”

Rather than be seen to be further enriching the rich, I think central banks will start closing the “free money for financiers” spigots.

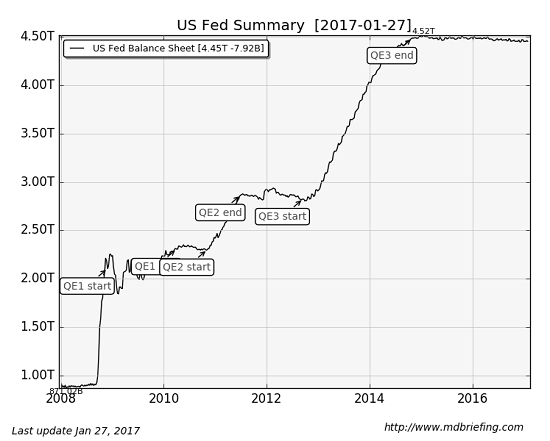

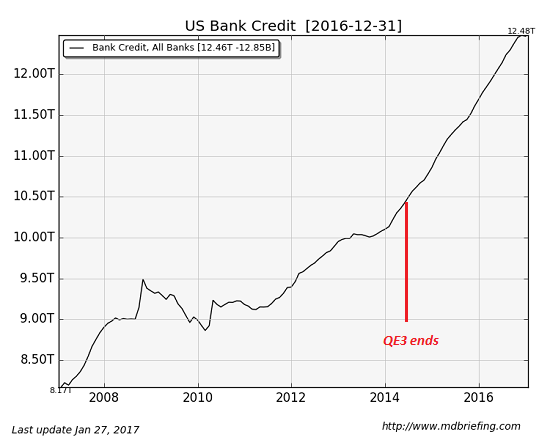

Take a quick glance at these charts of the Federal Reserve balance sheet and bank credit in the U.S. Notice what happened to bank credit after the Fed “tapered” and stopped expanding its balance sheet?

Bank credit exploded higher:

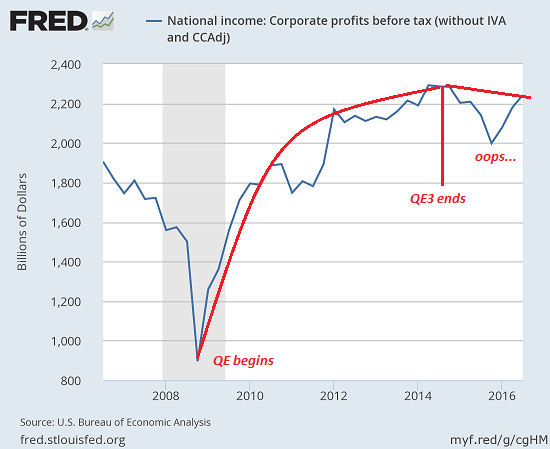

Now look at corporate profits:

Once the Fed ended its $3.7 trillion “experiment” of vastly expanding its money-creation and bond-buying in early 2014, what happened to bank credit? Bank credit had expanded by a bit over $1 trillion in the early years of the Fed’s quantitative easing, but it really took off after QE3 ended, soaring roughly $2 trillion.

This was the policy goal all along: the Fed would do the heavy lifting to keep credit and the financial markets from imploding, and eventually private-sector credit would expand enough to fuel a self-sustaining recovery.

While measures of employment and production have lofted higher, productivity, profits and wages for the bottom 95% have all stagnated. Is it coincidental than corporate profits began weakening once the Fed’s QE3 ended? Perhaps.

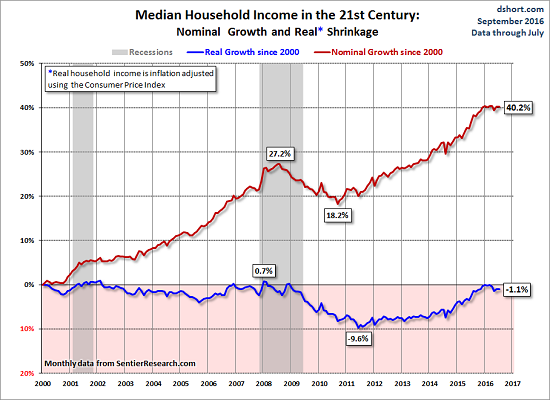

How about the stagnation of household median income during the Fed’s expansion and the rise of private bank credit from 2014 to the present? Was that also a coincidence?

If the economy was expanding smartly as the Fed was goosing credit higher, it certainly wasn’t trickling down to households.

What’s happening beneath the happy-happy surface is that the returns on expanding credit are diminishing rapidly. The Fed’s QE “free money for financiers” never did “trickle down” to the bottom 95%, and the enormous expansion of bank credit is no longer driving corporate profits higher.

…click on the above link to read the rest of the article…