The rationale for today’s easy money policies is pretty straightforward: Falling interest rates and rising government deficits will counteract the drag of excessive debts taken on in previous stimulus programs and asset bubbles, enabling the developed world to create wealth faster than it takes on new debt. The result: a steady decline in debt/GDP to levels that allow the current system to survive without wrenching changes.

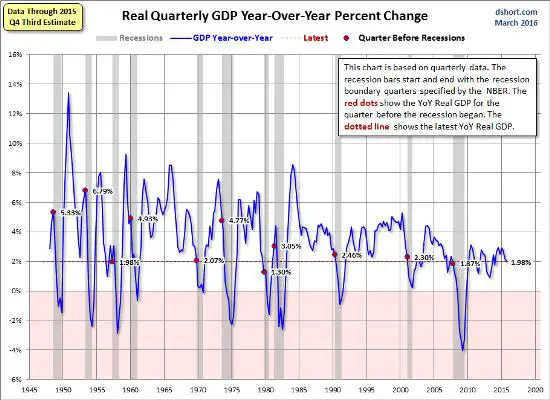

That’s a seductive, free-lunchy kind of idea — if it actually worked. But as the following chart of historical US GDP growth illustrates, as we’ve taken on more and more debt, each successive stimulus program has generated less and less growth. Compare the past few years to the rip-roaring recoveries of the 1960s through 1990s and it’s clear that whatever mechanism once converted easy money into greater wealth is no longer operating.

And note that the 2% recent growth on the above chart doesn’t include the revision of Q4 2015 growth to only 1.4%, and the Atlanta Fed’s GDPNow projection of 0.4% growth for 2016’s first quarter.

It’s the same story pretty much everywhere else. Japan, for instance:

Now the question becomes, how does the US and the rest of the world “grow out of its debt” if it can’t grow at all? Won’t the steady accretion of debt at every level of every society go parabolic in a zero-growth world? The answer is that mathematically speaking, this appears to be unavoidable.

So what will we do? More of the same of course:

OECD Calls for Urgent Increase in Government Spending

(Wall Street Journal) – Governments in the U.S., Europe and elsewhere should take urgent and collective steps to raise their investment spending and deliver a fresh boost to flagging economic growth, the Organization for Economic Growth and Development said Thursday.

…click on the above link to read the rest of the article…