Brent Crude prices could jump to well above $150 per barrel if Russia’s oil exports fall off a cliff in the coming months, according to Bank of America.

“With our $120/bbl Brent target now in sight, we believe that a sharp contraction in Russian oil exports could …. push Brent well past $150/bbl,” analysts at Bank of America (BofA) Global Research wrote in a research note on Friday carried by Reuters.

In a base-case scenario, Bank of America expects Brent Crude prices to average $104.48 a barrel this year and $100 a barrel in 2023.

Early on Friday, Brent Crude was trading at over $117 per barrel, the highest in two months, amid tight fuel supplies globally and bullish prospects of demand with the U.S. driving season beginning with the Memorial Day holiday weekend and Shanghai in China set for gradual reopening from June 1st.

There is a distinct possibility of a sharp drop in Russian oil exports as the EU continues to seek consensus and persuade Hungary to drop its opposition to a Russian oil embargo. Reports have it that some EU member states are inclined to accept a temporary exemption of Russian pipeline supply to central Europe via the Druzhba pipeline from the embargo as a bargaining chip to convince Hungary to agree to a ban on imports of Russian seaborne oil.

…click on the above link to read the rest of the article…

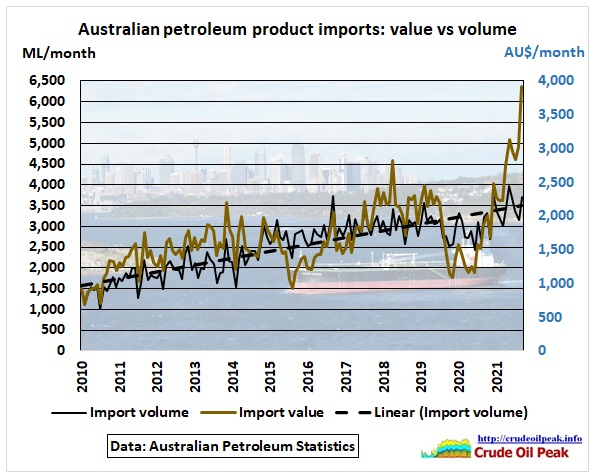

Fig 1: Petroleum product imports by volume (black lines) and value (brown line)

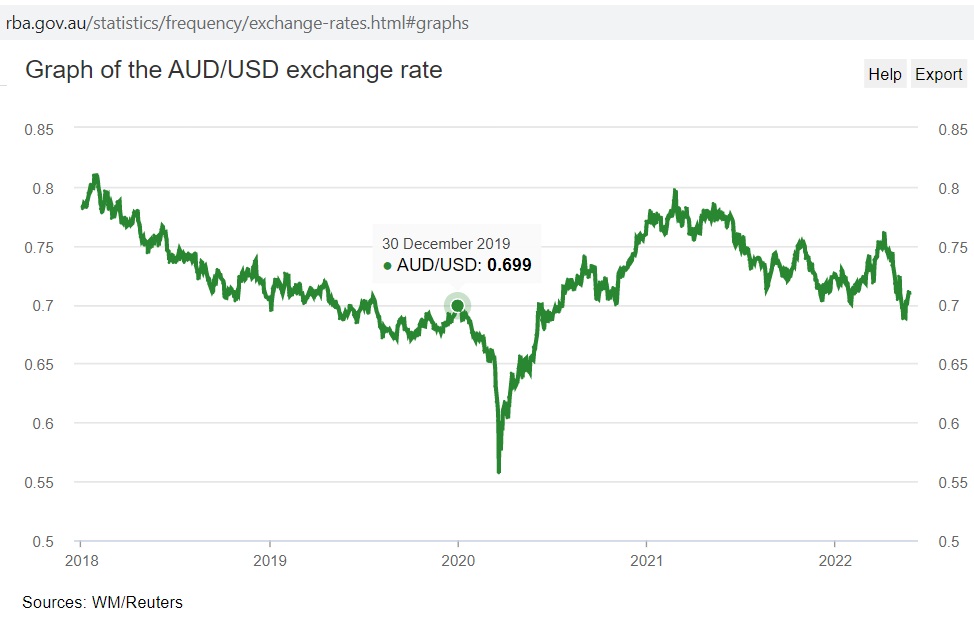

Fig 1: Petroleum product imports by volume (black lines) and value (brown line) Fig 2: Australian dollar to US$ exchange rate

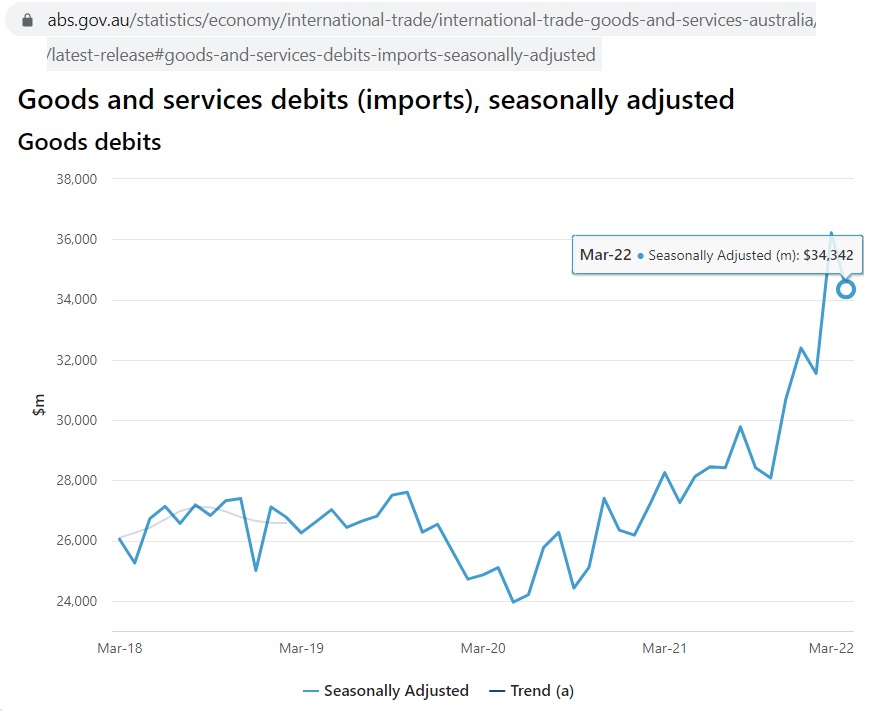

Fig 2: Australian dollar to US$ exchange rate Fig 3: Goods and services debits (imports)

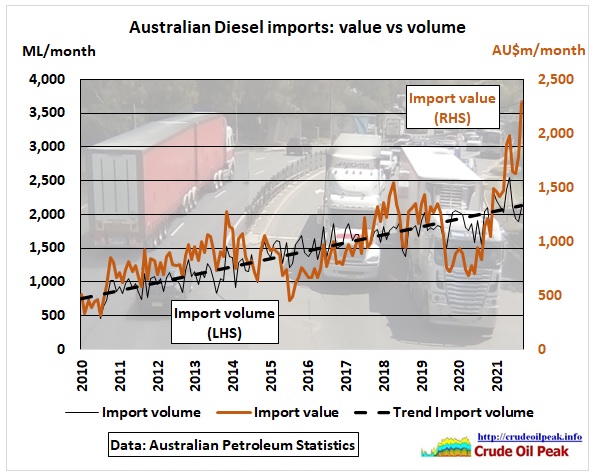

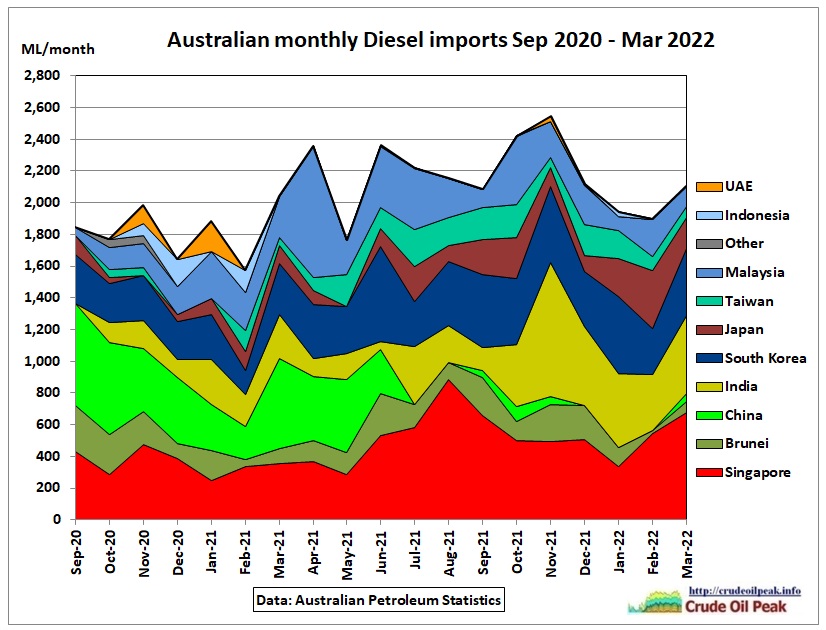

Fig 3: Goods and services debits (imports) Fig 4: Diesel imports by volume and value

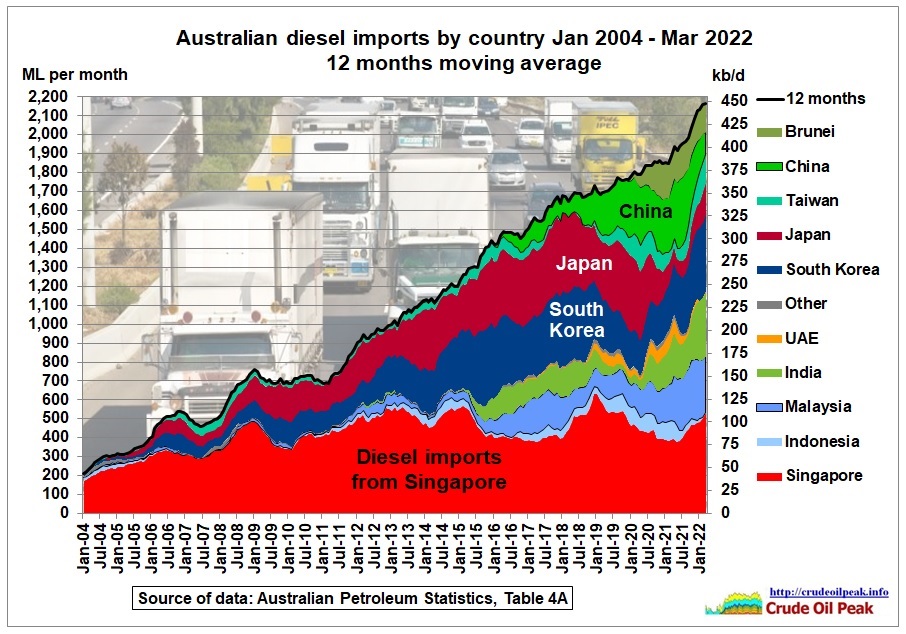

Fig 4: Diesel imports by volume and value Fig 5: Diesel imports by country

Fig 5: Diesel imports by country Fig 6: Monthly diesel imports

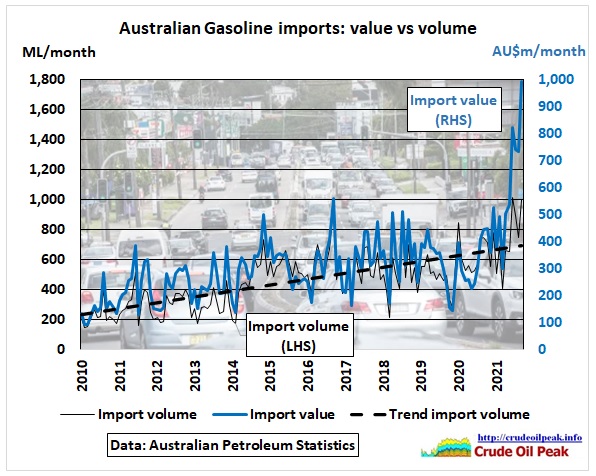

Fig 6: Monthly diesel imports Fig 7: Petrol imports by value and volume

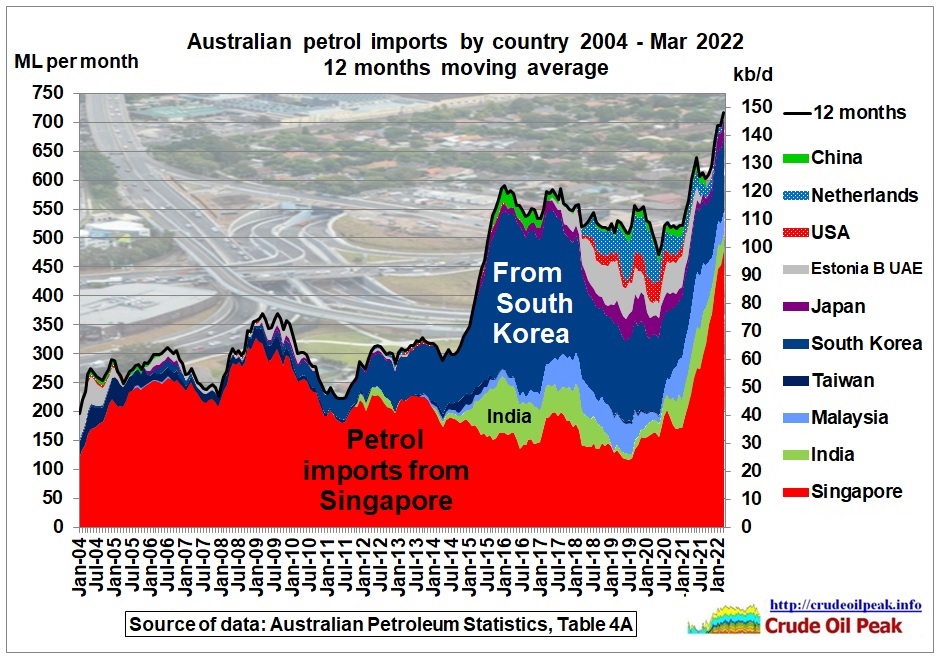

Fig 7: Petrol imports by value and volume Fig 8: Petrol imports by country. Singapore now dominates

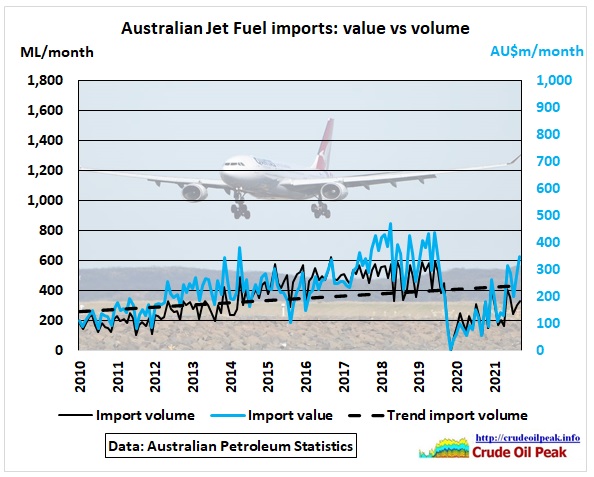

Fig 8: Petrol imports by country. Singapore now dominates Fig 9: Jet fuel imports by value and volume

Fig 9: Jet fuel imports by value and volume