Lebanon Announces Default On $1.2BN Debt Payment In Historical First

Lebanon announced Saturday it will default on its Eurobond debt for the first time in its history. The protest-racked country has seen a recent change in government, banks opened for merely about half of the past few months, strict controls on hard currency withdrawals and transfers abroad amid a liquidity crisis, a plummeting Lebanese Lira since October, a run on dollars, and crushing public debt which has lately blown up to nearly 170% of its gross domestic product (now about $89.5 billion).

Prime Minister Hassan Diab confirmed in public statements the bond payment of $1.2 billion due on Monday will not be paid: “The debt has become bigger than Lebanon can bear, and bigger than the ability of the Lebanese to meet interest payments,” he said in a televised address. “We are paying the price for the mistakes of the past years. Must we bequeath them to our children?”

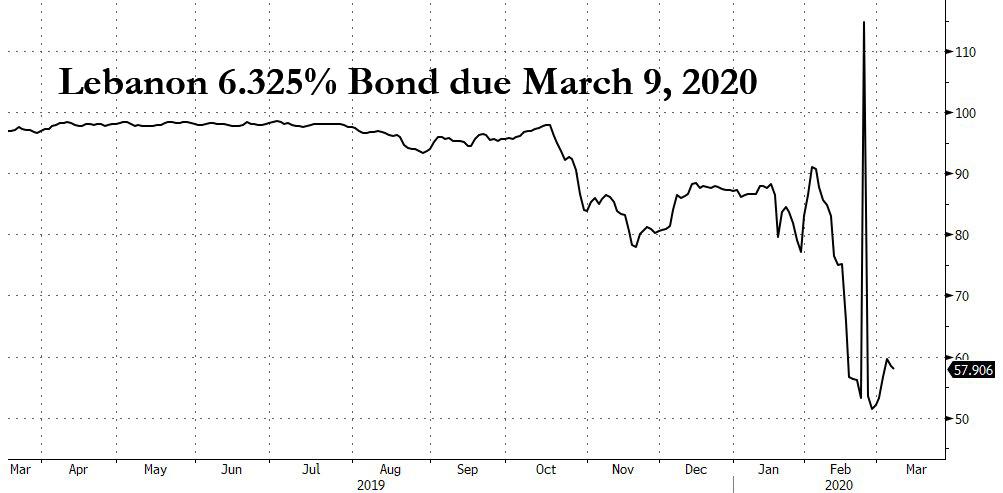

The broader crisis is being widely described as the worst and most potentially destabilizing disaster since the 1975-90 civil war. It also means that the country’s bond which mature on Monday and which last traded at a price of 57 cents on the dollar (or roughly 8000% YTM) won’t be repaid.

Local banks, which own some of the Eurobonds set to mature on March 9, have long argued against a default. But clients also fear the continued rapid depletion of their savings. Diab, appearing to respond not only to the people in the streets but to criticisms from the West centered on the Mediterranean nation’s decades of state corruption, pledged to continue negotiations to restructure the country’s debt “with all creditors… in a manner consistent with the national interest.”

…click on the above link to read the rest of the article…