Fed’s Emergency Repo Operation Oversubscribed As Repo Rates Spike To December High

Ahead of today’s massive liquidity drain, which according to some calculations will be as much as $100 billion between $54BN in coupon settlements from last week’s Treasury auctions and an additional $50 billion or so in corporate income tax payments to the Treasury…

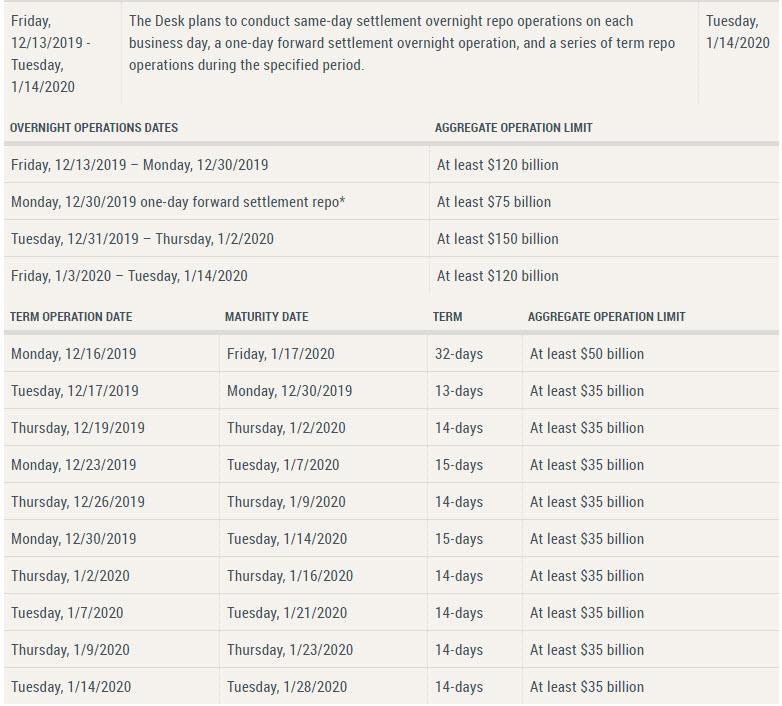

… which combined would be as large, if not bigger than the Sept 16 cash transfer to the Treasury which sparked the mid-September repo crisis, last Thursday the Fed announced a “kitchen sink” liquidity tsunami, throwing as much as $500 billion in liquidity backstops in the form of expanded and extended repo and term repo operations, while keeping the Fed’s “Not QE” T-Bill monetization chugging along.

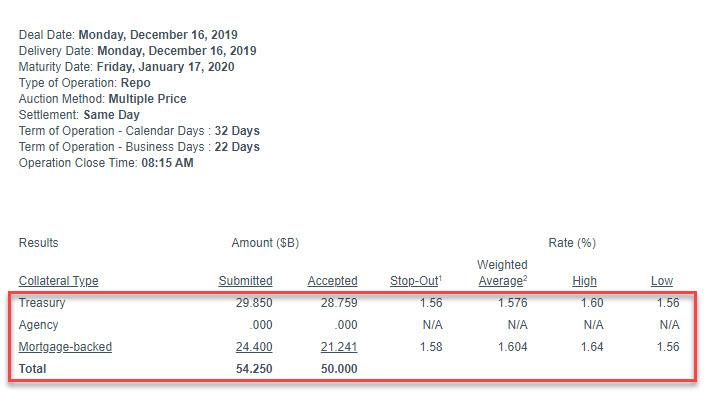

The first of these emergency repo operations was scheduled for this morning, ahead of the liquidity drain, in the form of a $50 billion, 32-day repo, which took place shortly after 8am, and was once again oversubscribed as there was more demand for liquidity, or $54.25 billion, than there was total supply.

Specifically, Dealers submitted $29.850BN in Treasury securities, and $24.4BN in MBS, at stop out rates of 1.56% and 1.58%, respectively, and which both came in more than fully subscribed relative to the $28.759BN in TSYs, and $21.241BN in MBS accepted.

This offering, which matures on January17, 2020, was the fourth “turn” repo providing funding past the year-end period.

The fact that the operation was oversubscribed was the first indication that banks are once again reserve-constrained and scrambling to procure as much year-end liquidity as they can get their hands on. Whether repo operations in the coming days are oversubscribed will indicate if the Fed’s roughly $500 billion in repo ops scheduled for the next 4 weeks will be enough to keep the Fed from losing control over overnight rates, as Credit Suisse repo expert Zoltan Pozsar predicted last week in his now infamous “Countdown to QE4” report.

…click on the above link to read the rest of the article…