JPMorgan: We Are Fast Approaching The Point Where Banks Run Out Of Liquidity

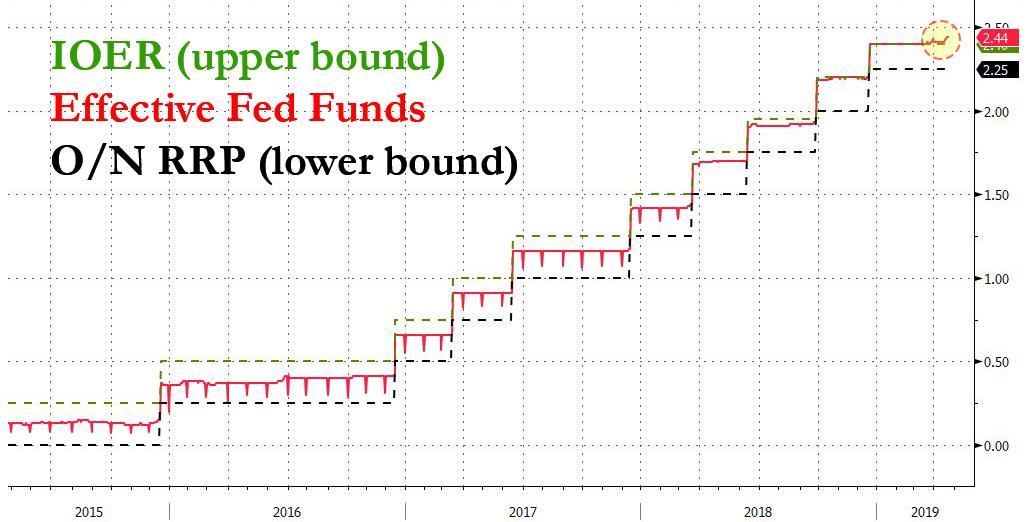

Last week we first noted that something unexpected has been going on in overnight funding markets: ever since March 20, the Effective Fed Funds rate has been trading above the IOER. This was unexpected for the simple reason that it is not supposed to happen by definition.

As a reminder, ever since the financial crisis, in order to push the effective fed funds rate above zero at a time of trillions in excess reserves, the Fed was compelled to create a corridor system for the fed funds rate which was bound on the bottom and top by two specific rates controlled by the Federal Reserve: the corridor “floor” was the overnight reverse repurchase rate (ON-RRP) which usually coincides with the lower bound of the fed funds rate, while on top, the effective fed funds rate is bound by the rate the Fed pays on Excess Reserves (IOER), i.e., the corridor “ceiling.”

Or at least that’s the theory. In practice, the effective FF tends to occasionally diverge from this corridor, and when it does, it prompts fears that the Fed is losing control over the most important instrument available to it: the price of money, which is set via the fed funds rate. And ever since March 20, this fear is front and center because as shown in the chart below, starting on March 20, the effective Fed Funds rate rose above the IOER first by just 1 basis point, and then, last Friday spiked as much as 4 bps above IOER.

…click on the above link to read the rest of the article…