Fed’s Fourth Bill POMO Is Most Oversubscribed Yet Amid Liquidity Scramble

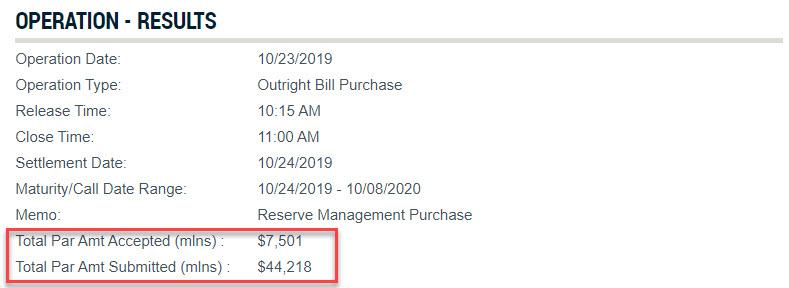

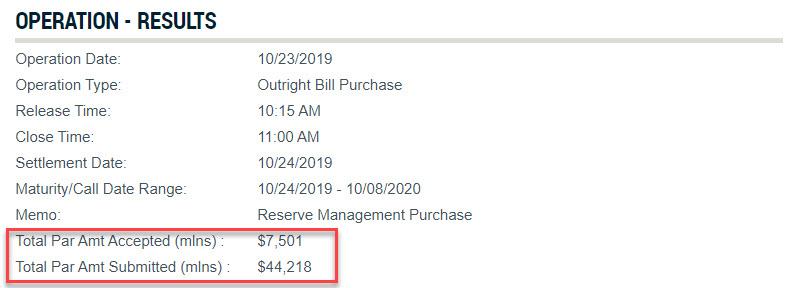

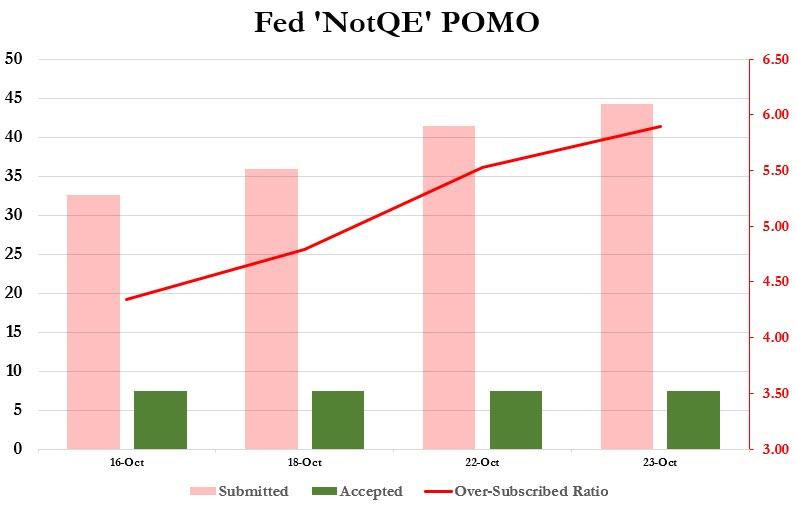

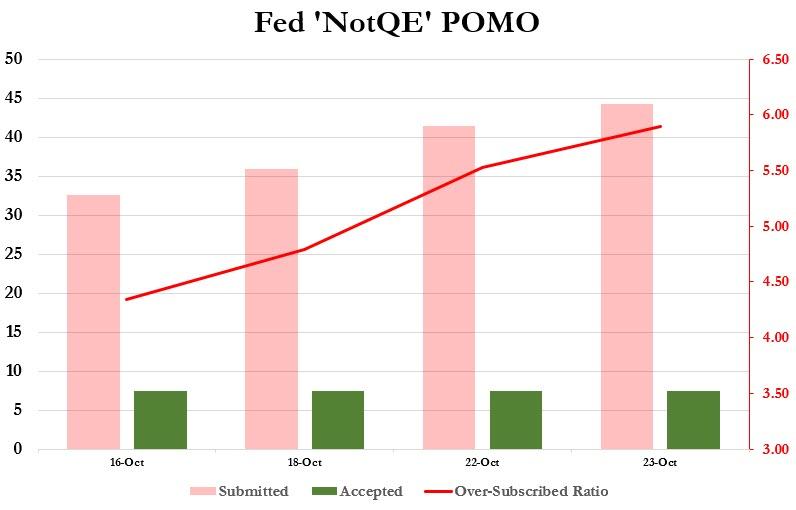

One day after the Fed unexpectedly saw a surge in demand for its term-repo operation, which was oversubscribed for the first time since the mid-September repo crisis erupted, the liquidity shortage in the funding market appears to be getting worse by the day, and in today’s just concluded 4th consecutive T-Bill POMO, which saw the Fed monetize another batch of Bills, Dealers submitted $44.2BN in bids for the maximum $7.5BN in Fed “Reserve Management” (note: not QE) purchases.

This means that today’s operation was 5.9x oversubscribed, the most of any operation since the launch of “Not QE4”, and clearly an increase from the first three POMOs, when operations were 4.3x, 4.8x and 5.5x oversubscribed.

{kind=link}

The results confirm that demand for the Fed’s permanent liquidity injection is increasing with every operation – suggesting that not only was the September repo turmoil not a one-time liquidity event, but that that liquidity shortage is getting worse – even as usage of the Fed’s latest overnight repo saw a modest decline.

As such the question we have been asking for the past month – and one which Elizabeth Warren should also consider asking of Steven Mnuchin – remains: why are banks still so desperate for liquidity even though the Fed has now made clear that its balance sheet will expand to accommodate all reserve needs, and why do they so stubbornly refuse to approach the interbank market for their funding needs? In short, what do they know about the banking system that we don’t?

{kind=link}