Satyajit Das: The CDO Bomb That Blew Up In 2008? There Is A New One

In recent months, with the investor spotlight increasingly falling on the “leveraged loan problem”, or the fact that there are now more leveraged loans outstanding – most of them offering virtually no covenant protection to investors and effectively stripping them of their “secured” position in the capitalization waterfall thus making them pari passu with high yield debt – than junk bonds, there has been a resurgence of discussions whether CLOs are the next “ticking timebomb”, and whether Collateralized Loan Obligations which have emerged as the primary source of demand for new loan issuance, will be the new CDOs and catalyze a systemic crash.

In an attempt to short-circuit such concerns, two weeks ago Barclays published a “CLO mythbuster” piece, in which it first noted that since 2008, Bloomberg, the Financial Times and even Hollywood have provided the general public with myriad causes of the Great Financial Crisis (GFC), “rarely failing to include a layman’s introduction to CDOs and how they played a major role”, and noting that “more recently, this conversation has grown to include comparisons to today’s CLO and leveraged loan markets, with premonitions of another GFC brewing just a decade after the last with CLOs acting as an accelerant.”

But first, this is Barclays defines a CDO in general, and a CLO in particular:

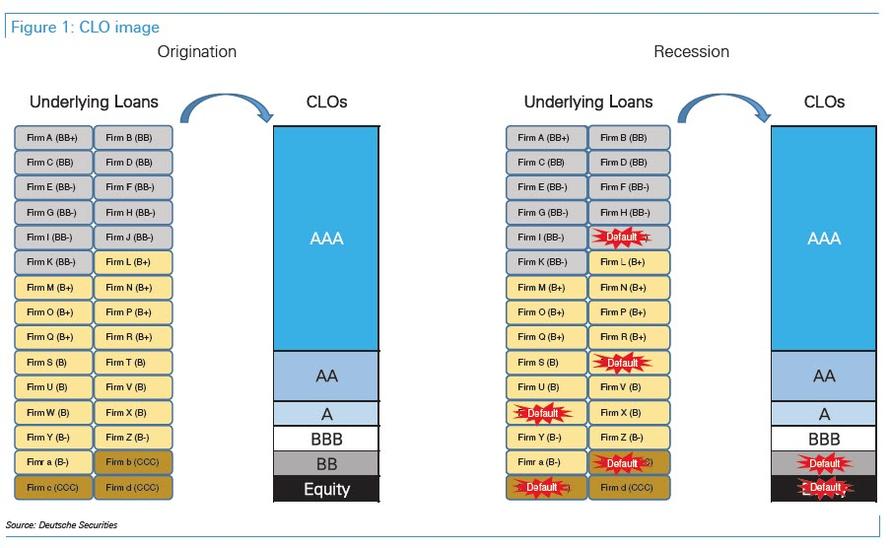

The term CDO actually covers an array of structured vehicles backed by debt, whether that debt is leveraged loans (CLOs), high-yield bonds (CBOs) or even other structured products (CDO-squared). So, while CDO subsets may have somewhat comparable structures (an SPV issues debt tranches, AAA through equity, and buys assets), the performance of the underlying assets and the ability for the vehicles’ liabilities to match the cash flows generated by those assets have proved vital for the future performance prospects of structured products.

…click on the above link to read the rest of the article…