Kass: Follow The Money

The Tremor Before the Quake and the Fed’s $450 Billion Balance Sheet Reduction

“The combination of rate hikes and balance sheet reductions from the Federal Reserve in 2018 sucked up global U.S. dollar liquidity and put emerging markets under immense pressure in 2018. Emerging market equities were 20-30% lower from February through October, then the S&P played catch-up to the downside. This, combined with tariffs from the White House, has placed global manufacturing in a significant slowdown that has begun to circle back into the United States. After all, over $60T of global GDP is OUTSIDE the USA.” – Lawrence McDonald, “Fed Cave-athon Driving Stocks Higher For Now“

Why did Fed Chairman Jerome Powell’s comments on Friday get such a ringing endorsement from the equity market?

The answer is simple.

The driver to market movement is not valuations. Rather, it is the degree of the system’s liquidity condition.

Valuations generally don’t matter much when liquidity is injected and expanding price- earnings ratios don’t end bull markets.

But when markets perceive a drying up in liquidity or central bankers pivot, as in late 2018, markets suffer.

Watch the money!

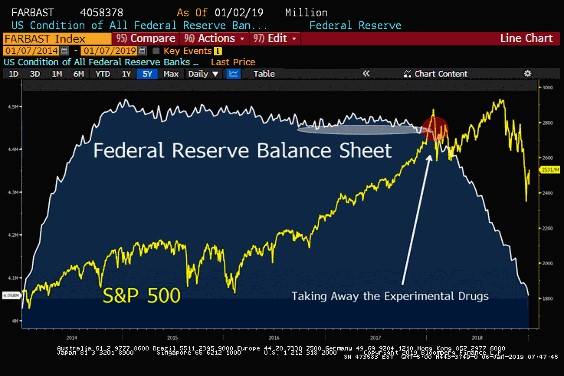

The problem is not rising interest rates in 2019. Regardless of the Fed’s actions this year — and I continue to believe there will be no fed fund hikes this year — the bloated Fed balance sheet will be running off as quantitative easing (QE) is reversed.

The relationship between liquidity and capital markets volatility is inversely related. That is why in the first half of 2018 I called for a new regime of volatility, which we have gotten in spades since late September 2018. And that is why I see a continuation of heightened volatility throughout this year.

Tightened Liquidity

Last week, Dennis Gartman produced this chart of the declining monetary base:

…click on the above link to read the rest of the article…