For the past few years, homeowners just about everywhere have been able to finesse life’s problems by thinking “at least my house is going up.” This home equity accretion allowed them to buy stuff on credit, safe in the knowledge that even as they maxed out yet another credit card their net worth continued to rise. They felt smart and confident, in other words, and so continued to behave in ways that the modern world defines as normal and natural.

But now that’s ending. Home prices have stopped rising in many places and in a few canaries in the financial coal mine have begun to plunge. Here’s what “plunge” means for Australians:

House prices ‘falling by over $1,000 a week’ in Sydney and Melbourne, Deloitte says

The boom time is over and we’re now officially experiencing the “house price fall we had to have”, according to Deloitte Access Economics’s latest business outlook.

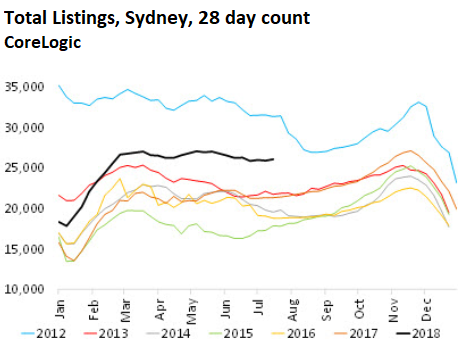

It has found what many had been predicting: prices are dipping as interest rates are rising, with our biggest cities feeling the winds of change most keenly.

“Our house prices here in Australia had streaked past anything sensible by way of valuation,” said Deloitte partner Chris Richardson.

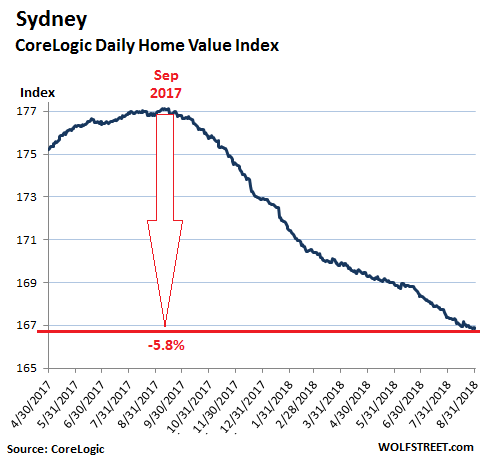

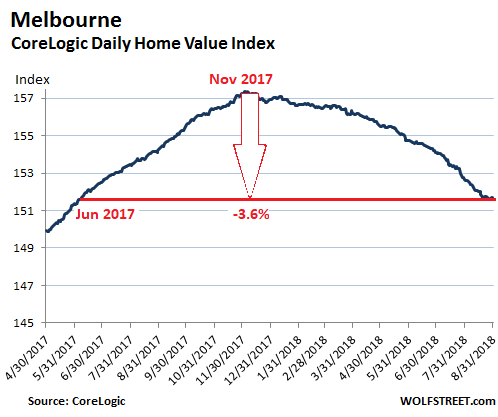

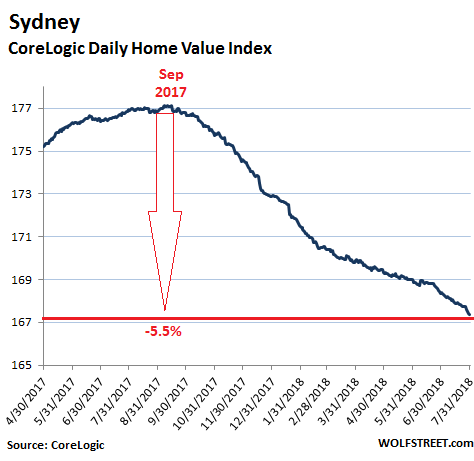

“Now, finally gravity has caught up with that stupidity and prices are falling.“In Sydney and Melbourne, housing prices are falling by over $1,000 a week.”

Prices had surged across the country over the past five years as historically low interest rates have driven Australians to load up on debt, while investors had also cashed in.

Not if, but by how much

Housing forecasts have gone from disagreement over whether home prices will fall to debates about how much they’ll decline.

…click on the above link to read the rest of the article…