Without the stimulus of ever-rising credit, the global economy craters in a self-reinforcing cycle of defaults, deleveraging and collapsing debt-based consumption.

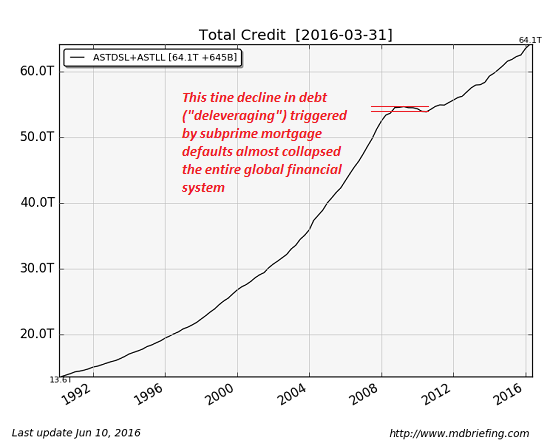

In an economy based on borrowing, i.e. credit a.k.a. debt, loan defaults and deleveraging (reducing leverage and debt loads) matter. Consider this chart of total credit in the U.S. Note that the relatively tiny decline in total credit in 2008 caused by subprime mortgage defaults (a.k.a. deleveraging) very nearly collapsed not just the U.S. financial system but the entire global financial system.

Every credit boom is followed by a credit bust, as uncreditworthy borrowers and highly leveraged speculators inevitably default. Homeowners with 3% down payment mortgages default when one wage earner loses their job, companies that are sliding into bankruptcy default on their bonds, and so on. This is the normal healthy credit cycle.

Bad debt is like dead wood piling up in the forest. Eventually it starts choking off new growth, and Nature’s solution is a conflagration–a raging forest fire that turns all the dead wood into ash. The fire of defaults and deleveraging is the only way to open up new areas for future growth.

Unfortunately, central banks have attempted to outlaw the healthy credit cycle.In effect, central banks have piled up dead wood (debt that will never be paid back) to the tops of the trees, and this is one fundamental reason why global growth is stagnant.

The central banks put out the default/deleveraging forest fire in 2008 with a tsunami of cheap new credit. Central banks created trillions of dollars, euros, yen and yuan and flooded the major economies with this cheap credit.

They also lowered yields on savings to zero so banks could pocket profits rather than pay depositors interest. This enabled the banks to rebuild their cash and balance sheets– at the expense of everyone with cash, of course.

{kind=link}