Something unusual happened while we were focused on the global oil-price collapse–the increase in U.S. shale gas production stalled (Figure 1).

Figure 1. U.S. shale gas production. Source: EIA and Labyrinth Consulting Services, Inc.

(click image to enlarge)

Total shale gas production for June was basically flat compared with May–down 900 mcf/d or -0.1% (Table 1).

Table 1. Shale gas production change table. Source: EIA and Labyrinth Consulting Services, Inc.

(click image to enlarge)

Marcellus and Utica production increased very slightly over May, 1.1 and 1.5 mmcf/d, respectively. The Woodford was up 400 mcf/d and “other” shale increased 300 mcf/d. Production in the few plays that increased totaled 3.3 mmcf/d or one fair gas well’s daily production.

Related: The Broken Payment Model That Costs The Oil Industry Millions

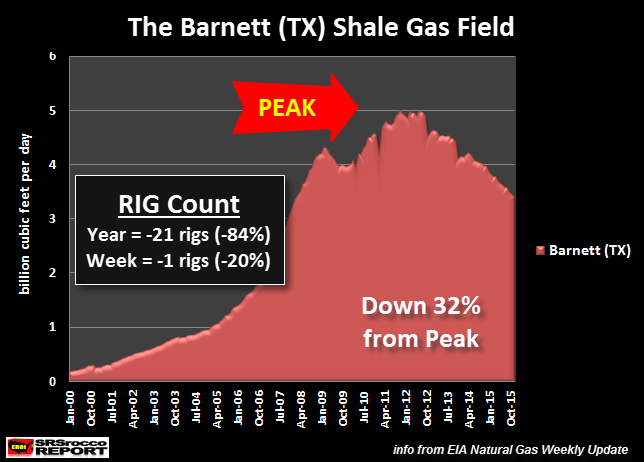

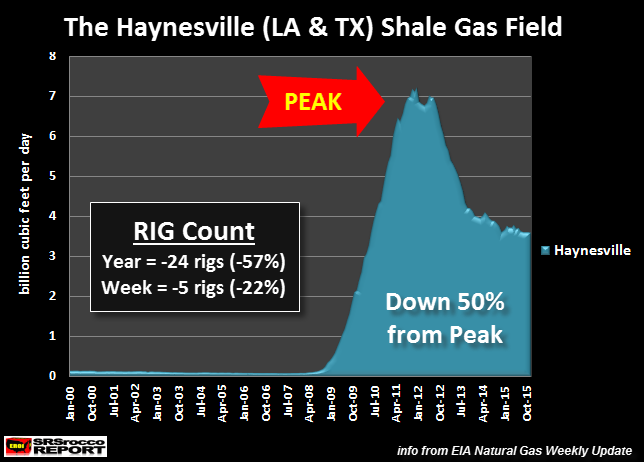

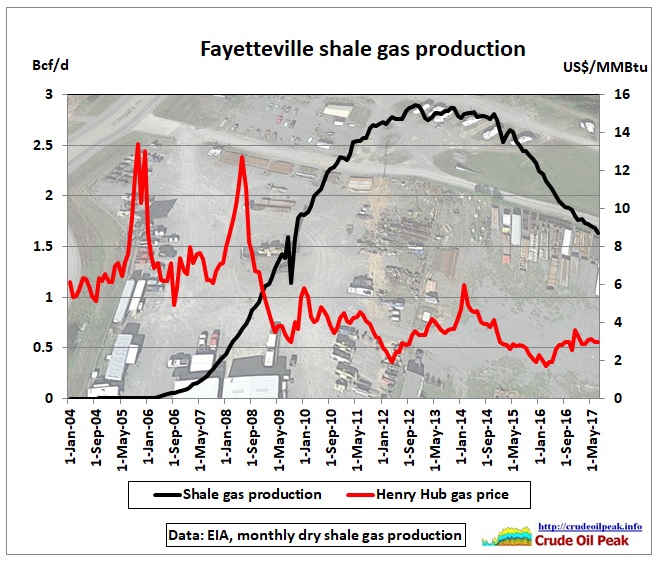

The rest of the shale gas plays declined. The earliest big shale gas plays–the Barnett, Fayetteville and Haynesville–were down 25%, 14% and 48% from their respective peak production levels for a total decline of -4.8 bcf/d since January 2012.

The fact that Eagle Ford and Bakken gas production declined suggests tight oil production may finally be declining as well.

To make matters worse, total U.S. dry natural gas production declined -144 mmcf/d in June compared to May, and -1.2 bcf/d compared to April (Figure 2). Marketed gas declined -117 mmcf/d compared to May and -1 bcf/d compared to April.

Figure 2. U.S. natural gas production. Source: EIA and Labyrinth Consulting Services, Inc.

(click image to enlarge)

Although year-over-year gas production has increased, the rate of growth has decreased systematically from 13% in December 2014 to 5% in June 2015 (Figure 3).

Figure 3. U.S. dry gas year-over-year production change. Source: EIA and Labyrinth Consulting Services, Inc.

(click image to enlarge)

This all comes at a time when the U.S. is using more natural gas for electric power generation. In April 2015, natural gas used to produce electricity (32% of total) exceeded coal (30% of total) for the first time (Figure 4).

…click on the above link to read the rest of the article…

Fig 1: Location of the Fayetteville shale

Fig 1: Location of the Fayetteville shale Fig 2: Testifying to the newly found wealth – as long as it lasts.

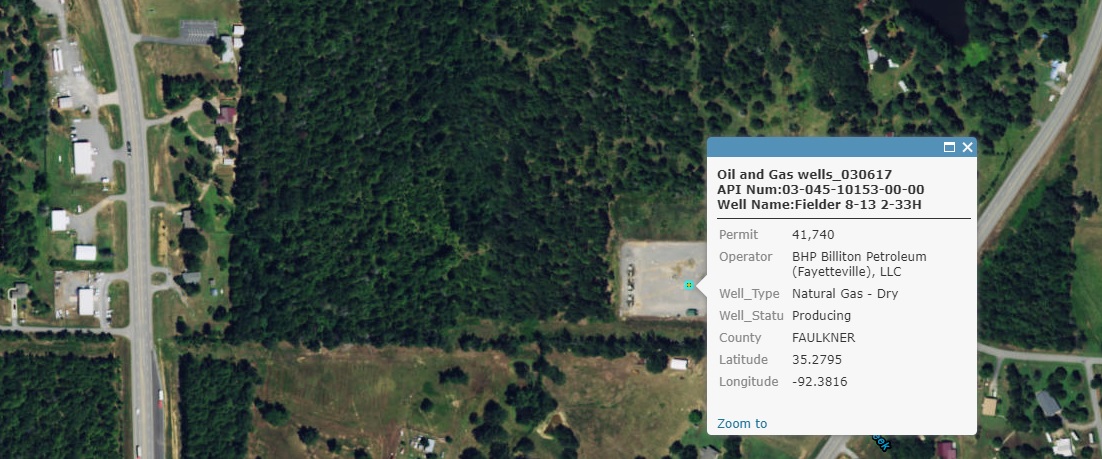

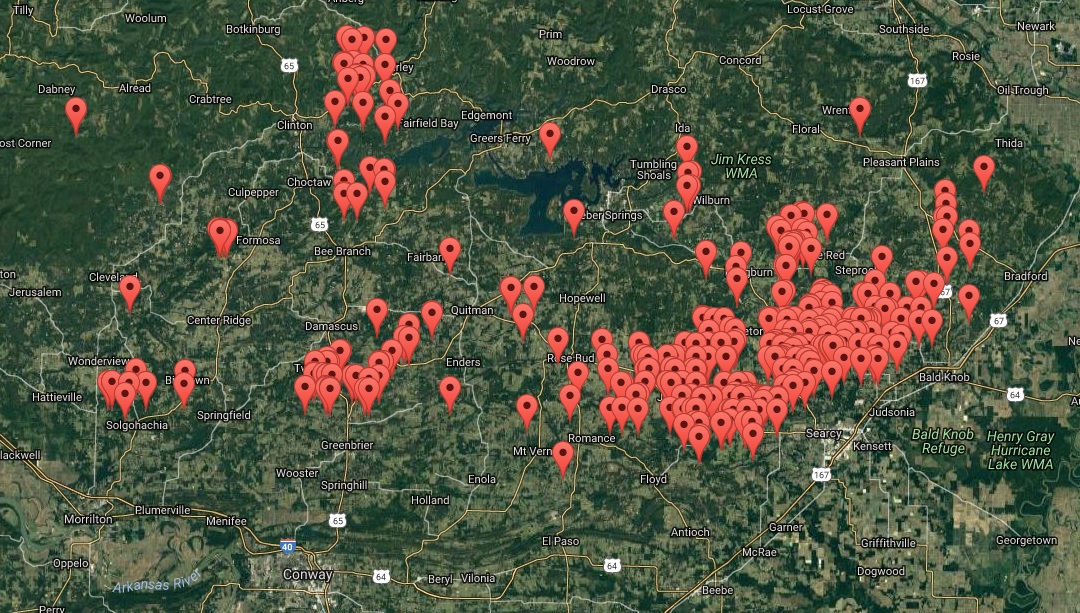

Fig 2: Testifying to the newly found wealth – as long as it lasts. Fig 3: BHP gas wells in Fayetteville

Fig 3: BHP gas wells in Fayetteville

Fig 5: Fayetteville shale gas production up to July 2017

Fig 5: Fayetteville shale gas production up to July 2017

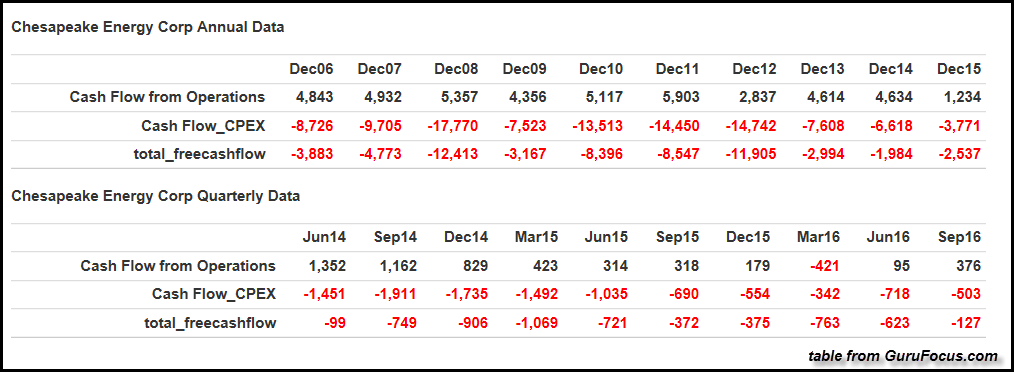

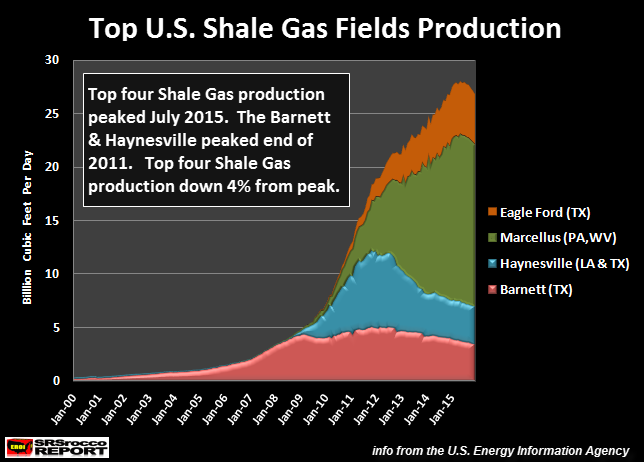

The countdown has started as the demise of the great U.S. shale gas industry has begun. This will have a disastrous impact on the U.S. economy as shale gas production declines in a big way. Unfortunately, very few Americans understand how sickly the domestic shale gas industry truly is, because they have been brainwashed to believe the United States is heading towards energy independence.

The countdown has started as the demise of the great U.S. shale gas industry has begun. This will have a disastrous impact on the U.S. economy as shale gas production declines in a big way. Unfortunately, very few Americans understand how sickly the domestic shale gas industry truly is, because they have been brainwashed to believe the United States is heading towards energy independence.