Home » Posts tagged 'depression' (Page 2)

Tag Archives: depression

Americans Have Already Skipped Payments On More Than 100 Million Loans, And Job Losses Continue To Escalate

Americans Have Already Skipped Payments On More Than 100 Million Loans, And Job Losses Continue To Escalate

Those that have been hoping for some sort of a “V-shaped recovery” have had their hopes completely dashed. U.S. workers continue to lose jobs at a staggering rate, and economic activity continues to remain at deeply suppressed levels all over the nation. Of course this wasn’t supposed to happen now that states have been “reopening” their economies. We were told that things would soon be getting back to normal and that the economic numbers would rebound dramatically. But that is not happening. In fact, the number of Americans that filed new claims for unemployment benefits last week was much higher than expected…

Weekly jobless claims stayed above 1 million for the 13th consecutive week as the coronavirus pandemic continued to hammer the U.S. economy.

First-time claims totaled 1.5 million last week, higher than the 1.3 million that economists surveyed by Dow Jones had been expecting. The government report’s total was 58,000 lower than the previous week’s 1.566 million, which was revised up by 24,000.

To put this in perspective, let me once again remind my readers that prior to this year the all-time record for a single week was just 695,000. So even though more than 44 million Americans had already filed initial claims for unemployment benefits before this latest report, there were still enough new people losing jobs to more than double that old record from 1982.

That is just astounding. We were told that the economy would be regaining huge amounts of jobs by now, but instead job losses remain at a catastrophic level that is unlike anything that we have ever seen before in all of U.S. history.

…click on the above link to read the rest of the article…

No, The U.S. Economy Will Definitely Not Be Returning To “Normal”. In Fact, Things Will Soon Get Even Worse.

No, The U.S. Economy Will Definitely Not Be Returning To “Normal”. In Fact, Things Will Soon Get Even Worse.

2020 has been quite a year so far. It has been one nightmare after another, and yet the economic optimists continue to insist that economic activity will soon snap back to normal levels somehow. So the economic optimists aren’t really alarmed by the fact that the core areas of our major cities have been torched, gutted and looted by rioters, because they assume that all of this violence is just a temporary phenomenon and that any damage that has been done can be repaired. And they aren’t really alarmed by the fact that the COVID-19 pandemic is starting to escalate again. In fact, over the last seven days we have seen the number of newly confirmed cases around the globe hit levels that we have never seen before. They just assume that “the worst is behind us” and that the vast majority of the businesses and jobs that have been lost during this pandemic will be quickly recovered.

Wouldn’t it be wonderful if they were actually correct?

Sadly, the truth is that economic conditions will not be returning to normal. Yes, some of the jobs that were lost will be recovered as states start to “reopen” their economies. But more than 100,000 businesses have already permanently closed during this new economic downturn, and all of those jobs are lost forever.

And yes, the level of economic activity will rise as states end their lockdowns, but it will still be much lower than it was before COVID-19 started spreading like wildfire in the United States.

At this point, even the perpetually optimistic OECD is admitting that global economic activity as a whole will be way down in 2020…

…click on the above link to read the rest of the article…

Most U.S. States Have ‘Reopened’ Their Economies, So Why Does Unemployment Continue To Spiral Out Of Control?

Most U.S. States Have ‘Reopened’ Their Economies, So Why Does Unemployment Continue To Spiral Out Of Control?

This wasn’t supposed to happen. Once states started to “reopen” their economies, the tsunami of unemployment was supposed to end. But instead, we continue to see Americans lose jobs at a pace that is far beyond anything we have ever seen before in all of U.S. history. All the way back in 1982, there was a week when 695,000 Americans filed initial claims for unemployment benefits, and that all-time record was never broken until this year. Of course we have seen monster number after monster number here in 2020, and we just learned that last week another 1.877 million Americans filed new claims for unemployment benefits…

Filings for unemployment insurance claims totaled 1.877 million last week in a sign that the worst is over for the coronavirus-related jobs crisis but that the level of unemployment remains stubbornly high.

Economists surveyed by Dow Jones had been looking for 1.775 million new claims. The Labor Department’s total nevertheless represented a decline from the previous week’s upwardly revised total of 2.126 million.

So even though more than 40 million Americans had already lost their jobs in 2020, there were still enough people losing their jobs last week to surpass the old record from 1982 by more than a million.

Just think about that.

Overall, a grand total of 42.6 million Americans have now lost their jobs since the pandemic began, and that makes this the largest spike in unemployment in all of U.S. history by a very wide margin.

And when the monthly employment report comes out on Friday, the official U.S. unemployment rate is expected to surpass 20 percent…

…click on the above link to read the rest of the article…

10 Numbers That Show The U.S. Has Fallen Into A Horrifying Economic Depression

10 Numbers That Show The U.S. Has Fallen Into A Horrifying Economic Depression

The last recession was really, really bad, but it was never like this. It is time for us to face reality, and that means admitting that the U.S. economy has plunged into a depression. This is already the worst economic downturn that America has experienced since the Great Depression of the 1930s, and we are right in the middle of the largest spike in unemployment in all of U.S. history by a very wide margin. Of course it was fear of COVID-19 that burst our economic bubble, and fear of this virus is going to be with us for a very long time to come. So we need to brace ourselves for an extended economic crisis, and at this point even Time Magazine is openly referring to this new downturn as an “economic depression”. Needless to say, there will be a tremendous amount of debate about how deep it will eventually become, but everyone should be able to agree that our nation hasn’t seen anything like this since before World War II.

In order to prove my point, let me share the following 10 numbers with you…

#1 According to a study that was just released by the National Bureau of Economic Research, more than 100,000 U.S. businesses have already permanently shut down during this pandemic, and that represents millions of jobs that are never coming back.

#2 The Federal Reserve Bank of Atlanta is now projecting that U.S. GDP will shrink by 42.8 percent during the second quarter…

A new GDP forecast from the Federal Reserve Bank of Atlanta for the three months through June estimates an unprecedented drop of 42.8 percent. The bank describes the data as a “nowcast” or real-time, compared with the official government report of GDP, which is dated. The first-quarter preliminary data, which showed a 4.8 percent dip, included a limited period of impact from COVID-19.

…click on the above link to read the rest of the article…

A Taste Of What Is Coming – Food Prices Just Increased By The Most That We Have Seen Since 1974

A Taste Of What Is Coming – Food Prices Just Increased By The Most That We Have Seen Since 1974

Get ready to pay much more for groceries. I have been warning that the flood of new money that the Federal Reserve and Congress have been pumping into the system would have very serious consequences, and I have also been warning that food prices would be shooting higher. When things start getting really crazy, demand for food and other basic essentials goes way up, and meanwhile this pandemic has significantly disrupted production of certain products. So even though most of the economy is currently still in a deflationary phase, food prices are beginning to spike. In fact, the U.S. Labor Department says that we just witnessed the largest one month increase since February 1974…

The Labor Department reported Tuesday that prices U.S. consumers paid for groceries jumped 2.6% in April, the largest one-month pop since February 1974. The spike in supermarket prices was broad based and impacted items from broccoli and ham to oatmeal and tuna.

The price of the meats, poultry, fish and eggs category rose 4.3%, fruits and vegetables climbed 1.5%, cereals and bakery products advanced 2.9%, and dairy goods gained 1.5%.

Sadly, this is just the beginning.

Prior to this pandemic, Americans spent about 10 percent of their incomes on food.

As this new economic depression deepens, expect that number to eventually more than double.

We live at a time when global food supplies are becoming increasing stressed for a variety of reasons. In wealthy countries this is going to force food prices aggressively higher, and in poor countries this is going to mean that a lot of people simply will not have enough to eat.

…click on the above link to read the rest of the article…

U.S. Depression? The V-Shaped Recovery Fades Away

U.S. Depression? The V-Shaped Recovery Fades Away

The recent jobless claims figures show how difficult it will be for the U.S. recovery to be as quick and strong as initially expected.

- 7.7 million jobs were lost in Hospitality and Leisure in April, 2.5 million in Education and Health, with 2 million in Retail and another 2 million in Professional Services. These sectors are unlikely to recover fast and enough to compensate the job losses of the past month and even less likely to see the same level of wages of 2019.

- Credit card delinquencies are rising, and retail sales are going to see a very modest recovery because household debt is increasing, wages are under pressure and most citizens are changing their consumption patterns, looking to strengthen their savings in case another shock arrives.

- Corporate debt is rising to new records due to the collapse in operating revenues. As such, companies will likely take all possible measures to conserve cash flow, reduce expenditure and be prudent about hiring decisions. This will lead to slower job creation and investment even once the economy opens.

- Tax increases are likely to affect the recovery. The government deficit is soaring, with the Treasury looking at $2 trillion of new debt in 2020 due to the measures implemented to combat the economic impact of coronavirus. Unfortunately, the Democrats are looking to increase taxes just when the economy needs more investment and attraction of capital. If taxes rise significantly, what is already a weak outlook for capital expenditure and job creation is likely to worsen.

All of this makes a V-shaped recovery even more challenging than before. However, the U.S. economy is likely to recover faster than the Eurozone and suffer less in 2020.

…click on the above link to read the rest of the article…

We Are Witnessing Economic Carnage Like We Have Never Seen Before, And The Economy Is Going To Continue To Bleed Jobs

We Are Witnessing Economic Carnage Like We Have Never Seen Before, And The Economy Is Going To Continue To Bleed Jobs

Now we are up to 33.5 million jobs lost. In just 7 weeks, the U.S. economy has been completely turned upside down, and the numbers are unlike anything that we have ever seen before. On Thursday, the Labor Department announced that 3.17 million Americans filed initial claims for unemployment benefits last week. That brings the grand total for this crisis up to 33.5 million, and that figure absolutely dwarfs what we witnessed during the last recession. And as I discussed yesterday, even the mainstream media is now admitting that millions of those jobs are never coming back.

Yes, some Americans will be going back to work now that the lockdowns are being ended, but for now it is being projected that the job losses will continue to surpass any gains that are made by workers that are returning to their old jobs.

In fact, one prominent economist told CNBC that it will likely take until mid-June before the number of Americans filing new claims for unemployment benefits each week falls below a million…

At the current pace, the week claims numbers should fall below 1 million by mid-June, according to Ian Shepherdson, chief economist at Pantheon Macroeconomics. “We’re very hopeful that June will see the beginnings of a rebound as states begin to reopen,” Shepherdson said.

To put that in perspective, prior to this year the all-time record for a single week was just 695,000.

So even when we get down to a million new claims each week, that will still be a catastrophic level.

And the truth is that these numbers don’t even tell the entire story. Because state unemployment websites have been so overwhelmed, there are vast numbers of unemployed Americans that still have not been able to successfully file claims.

…click on the above link to read the rest of the article…

Straight Talk

Straight Talk

We live through very unique times, not only because of the shock of the coronavirus that recently hit the world unexpectedly, but also because of large complex structural issues that have been building for decades.

A popular mantra says the stock market is not the economy and the economy is not the stock market referring to the often seen disconnect between market prices and events taking place in the economy. The most recent example has been Wall Street rallying with each disastrous jobs report hitting the news wires. Even this last Friday markets rallied again unperturbed by the latest unemployment report showing the most severe collapse in employment in our recent history. Depression like figures, yet the Nasdaq is green on the year, the S&P 500 largely off the lows with many again predicting new highs to come. Why? Because of unprecedented liquidity flooding markets as a result of monetary intervention making the disconnect between Wall Street and Main Street even wider. We can pretend the stock market is not the economy, but there is no stock market without an economy yet we are witnessing an unprecedented disconnect between the two that has been building for years.

Can this disconnect be sustained? Are investors too optimistic about the current rally? What are the implications going forward?

These are complex issues everyone is confronted with and there are no easy answers. What an intellectually challenging and energizing time to be alive!

I am grabbling with these issues as much as you are, we all are. And for that reason the idea for an ongoing webinar arose, to find a format to discuss these issues in more depth and make the debate more accessible and personal.

…click on the above link to read the rest of the article…

Oil flows spell deep depression

Oil flows spell deep depression

Energy is not just one commodity among many in the economy; it is the commodity. Without energy, nothing gets done. And, oil is not just one form of energy in the energy commodity complex; it is the energy source upon which our modern way of life depends. In fact, it is the main energy source running through the arteries of the global economy.

Far from being a boon to the world, ultra-low oil prices signal that the global economy is flat on its back—even worse, flat on its back with two broken legs.

Petroleum geologist and consultant Art Berman recently detailed the problem in this piece. Berman is the man who accurately predicted—starting way back in 2008—the persistent losses that shale oil and gas would produce for the companies that extracted them. The shale industry continuously vilified Berman for his analysis over the next decade, even as the industry was in the process of blowing 80 percent of investors’ capital as of last year. With the arrival of the coronavirus, the coup de grâs has just been delivered to a shale oil and gas industry that was already on its knees.

Perhaps the most important thing to understand about the current oil “glut” is that it is not merely the result of producing too much oil for an economy humming on all cylinders. It is primarily the product of a coronavirus-infested economy in which demand has dropped 20 percent in just a few weeks. As Berman points out, estimated U.S. oil consumption has returned to a level not seen since 1971.

…click on the above link to read the rest of the article…

National Guard Deployed At Nation’s Food Banks To Ensure Stability During Unprecedented Times

National Guard Deployed At Nation’s Food Banks To Ensure Stability During Unprecedented Times

There is increasing evidence on social media that the National Guard has been deployed to the nation’s food banks to ensure food supply chain networks are not severed, and shortages do not materialize.

This comes at a challenging period for the country, one where 26.5 million people have filed for unemployment benefits in five weeks as the economy crashes into depression.

We have documented the unprecedented volume of Americans flooding food banks across the country in the last four weeks as a hunger crisis develops.

Now it appears National Guard troops have been deployed to food banks in many states to make sure logistical pipelines of food to these facilities can continue dishing out care packages to the working poor.

And why would the Pentagon, likely instructed by the Trump administration, deploy military assets to food banks? Because food shortages are already starting to develop as facilities are overwhelmed with hungry people.

The deployment of military assets to these facilities is a reflection of where the government believes the most vulnerable parts of instabilities reside at the moment. Just imagine if some of these places ran out of food, and people in mile-long lines were told to go home empty-handed. That would leave many in an untenable hangry state where social instabilities could be seen.

So, without further ado, here is the military deployed at the nation’s food banks:

A very cool #timelapse of the #Delaware #NationalGuard assisting a food bank

… https://dvidshub.net/r/fs5sks #COVID19

…click on the above link to read the rest of the article…

When Economic Depression Follows Pandemic, No Time to Waste

When Economic Depression Follows Pandemic, No Time to Waste

What the Bank of Canada and IMF see coming will demand bold stimulus.

It is still sinking in that the end of the pandemic will not be the end of our troubles. On the contrary — we will likely see the end of the pandemic overlap with a full-scale economic depression, with COVID-19 waiting to make recurrent comebacks. Amid a global economic collapse, Canada will have to postpone hopes of recovery; for the foreseeable future, we will be in damage-control mode.

The IMF’s best-case scenario assumes that the pandemic “fades” in the second half of 2020, and “containment efforts can be gradually unwound,” permitting some economic rebuilding. Even so, “the global economy is projected to contract sharply by -3 per cent in 2020, much worse than during the 2008-09 financial crisis.”

Strikingly, the IMF implicitly endorses a program that is socialist in all but name:

“The immediate priority is to contain the fallout from the COVID-19 outbreak, especially by increasing health-care expenditures to strengthen the capacity and resources of the health-care sector while adopting measures that reduce contagion. Economic policies will also need to cushion the impact of the decline in activity on people, firms and the financial systems reduce persistent scarring effects from the unavoidable severe slowdown; and ensure that the economic recovery can begin quickly once the pandemic fades.”

The IMF approves such policies in many of the advanced countries as well as in China, Indonesia and South Africa. It argues that “Broad-based fiscal stimulus can preempt a steeper decline in confidence, lift aggregate demand, and avert an even deeper downturn. But it would most likely be more effective once the outbreak fades and people are able to move about freely.”

The best-case scenario?

…click on the above link to read the rest of the article…

America’s New Breadlines Are Growing…

America’s New Breadlines Are Growing…

Over the past month, the American economy has collapsed into a depression, with the most significant unemployment spike in history. Millions of people have just lost their jobs, and as we’ve been documenting, food bank networks across the country are becoming overwhelmed.

We recently said that some food banks had seen an eightfold increase in the number of people asking for food. The National Guard has been deployed to food banks in Cleveland, Pittsburgh, and Phoenix, to make sure supply chains do not breakdown, which if food shortages did materialize, it could lead to a “social bomb,” triggering civil unrest.

“I’ve been in this business over 30 years, and nothing compares to what we’re seeing now. Not even when the steel mills closed down did we see increased demand like this,” said Sheila Christopher, director of Hunger-Free Pennsylvania, which represents 18 food banks across 67 counties.

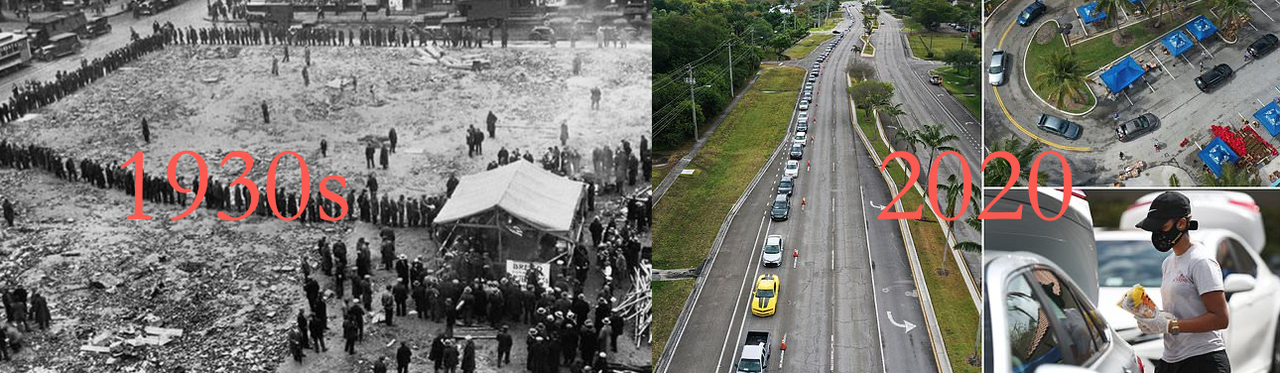

Today’s food bank lines resemble ‘breadlines’ from the 1930s. However, this time around, Americans are not standing around city blocks waiting for soup, they’re sitting in mile-long traffic jams outside donation centers waiting for a care package.

The run on food banks was first documented on March 30. Drone footage captured a traffic jam of hungry Americans waiting to pick up food aid at a facility in Duquesne, Pennsylvania.

Hundreds of cars wait to receive food from the Greater Community Food Bank in Duquesne. Collection begins at noon. @PghFoodBank @PittsburghPG

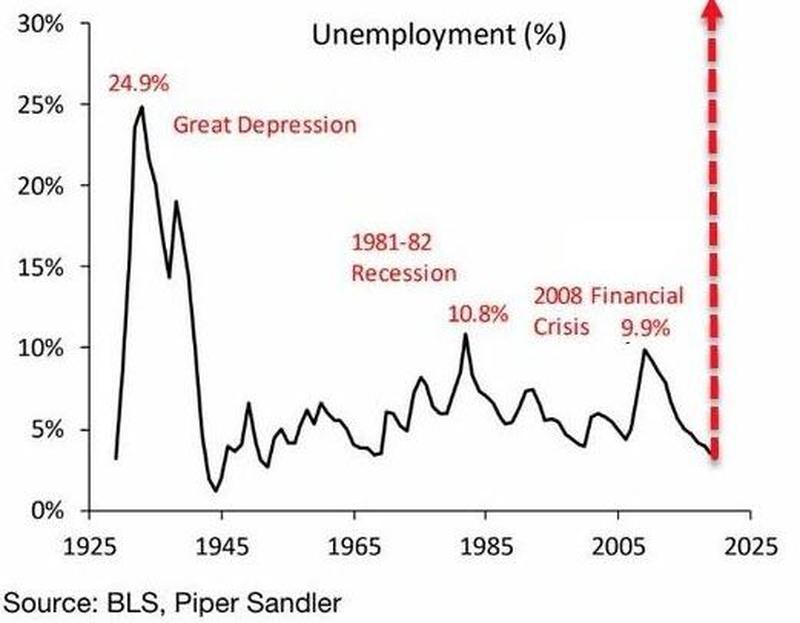

As a reminder, to visualize how America went from “the greatest economy ever” to “Greater Depression,” in just one month, take a look at the chart below:

The run on food banks will only increase as the depression worsens in April.

On Monday, a drone captured dramatic footage outside a South Florida food bank that measured “miles-long” row of cars, reported Daily Mail.

…click on the above link to read the rest of the article…

The worst economic collapse ever?

The worst economic collapse ever?

Country after country has reported extremely dark economic numbers. The gigantic jobless claims, 6.6 million from the U.S. last week, are just the tip of the iceberg. For example, the service sector PMIshave been simply ghastly across the globe. We are now in a crisis of epic proportions.

But, how massive can the crisis eventually get? Since our inception, in 2012, we have contemplated three scenarios as a part of our quarterly forecasts. While we have not referred to them in each report, we have repeated them periodically. They are: the optimistic, the most probable and the pessimistic.

But at this point our main worry is the approaching realization of the pessimistic, or the worst, scenario. It’s likelihood, while still low, is increasing fast in our estimate.

Underpinning its severity is not the virus, but the fragility of the global economy.

Breeding chaos: failed clean-ups and bad policies

The Global Financial Crisis (GFC) was considered a Black Swan event to many. However, it was no such thing. It was a massive failure of hedging and diversification within the global banking system, most notably in the U.S., and a number of prominent analysts saw it coming. See our blog, 10 years from Lehman. And nothing has been fixed, for an insight view on that crisis.

While banks were wound down and recapitalized in the U.S. after the GFC, an equivalent restructuring did not happen in Europe. Stricken European banks were left to linger in a state of permanent financial distress.

“Outright Monetary Transactions” or “OMT”, negative interest rates, and ECB’s QE program all aggravated the predicament of European banks. The failure to resolve the 2008 crisis ‘zombified’ the European banking sector, a situation which persists today. (See Q-Review 3/2019 for a detailed account).

…click on the above link to read the rest of the article…

Gold Gains 3% To $1,672 and Silver Surges 5% To $15.40; Goldman Warns Of $3 Trillion Explosion In U.S. Debt

Gold Gains 3% To $1,672 and Silver Surges 5% To $15.40; Goldman Warns Of $3 Trillion Explosion In U.S. Debt

◆ Gold surged 2.9% and silver by 5% yesterday, with futures leading the way higher with gold reaching it’s highest price in more than seven years

◆ Investors are diversifying into safe haven gold to hedge themselves from the coming destruction of balance sheets, trillions and trillions of fiscal and monetary stimulus and a likely economic depression

◆ JPMorgan Chase & Co.’s Jamie Dimon has blamed the pandemic on creating a “major major downturn” (see News below) and potentially an economic depression

◆Goldman Sachs have warned that the emergency “stimulus” may lead to an explosion of US national debt by about $4 trillion in just two years (see News below). This is not including the trillions in monetary stimulus by the Federal Reserve to bail out Wall Street including most large financial service providers including the mortgage sector and banks

◆ The “Everything bubble” is bursting before our eyes which is evident in the stock market crashes. Property and bond market bubbles will soon burst and confidence in the dollar and other fiat currencies will soon begin to evaporate

◆ Gold’s utility as a safe haven is again being experienced by those who own it. Gold is outperforming and has delivered a 12% dollar return in 2020 year to date, exactly when they need a safe haven and a source of returns as stocks and other assets under perform. Gold has seen even greater returns in other currencies and is 15% higher in euros and 19% higher in pounds year to date.

◆ The only major asset to outperform gold year to date is the U.S. 30 year bond. This out performance is unlikely to continue as the 30 year bond cannot go much higher. We are near 0% interest rates despite the appalling fiscal, financial and economic outlook for the U.S.

…click on the above link to read the rest of the article…

Could the Covid19 Response be More Deadly than the Virus?

Could the Covid19 Response be More Deadly than the Virus?

The economic, social and public health consequences of these measures could claim millions of victims

The initial, alarming estimates of deaths from the virus COVID-19 were that as many as 2.2 million people would die in the United States. This number is comparable to the annual US death rate of around 3 million. Fortunately, correction of some simple errors in overestimation has begun to dramatically reduce the virus mortality claims.

The most recent estimate from “the leading US authority on the COVID-19 pandemic” suggests that the US may see between 100,000 and 200,000 deaths from COVID-19, with the final tally likely to be somewhere in the middle.” This means that we are expecting around 150,000 US deaths caused by the virus, if the latest estimates hold up.

How does that compare to the effects of the measures taken in response? By all accounts, the impact of the response will be great, far-reaching, and long-lasting.

To better assess the difference we might ask, how many people will die as a result of the response to COVID-19? Although a comprehensive analysis is needed from those experienced with modeling mortality rates, we can begin to estimate by examining existing research and comparative statistics. Let’s start by looking at three critical areas of impact: suicide and drug abuse, lack of medical treatment or coverage, and poverty and food access.

SUICIDES AND DRUG ABUSE

According to the National Center for Health Statistics, over 48,000 suicides occurred in the US in 2018. This equates to an annual rate of about 14 suicides per 100,000 people. As expected, suicides increase substantially during times of economic depression. For example, as a result of the 2008 recession there was an approximate 25% increase. Similarly, during a peak year of the Great Depression, in 1932, the rate rose to 17 suicides per 100,000 people.

…click on the above link to read the rest of the article…