Our reader L from Mumbai has mailed us a number of questions about the negative interest rate regime and its possible consequences. Since these questions are probably of general interest, we have decided to reply to them in this post.

The NIRP club – negative central bank deposit rates – click to enlarge.

The NIRP club – negative central bank deposit rates – click to enlarge.

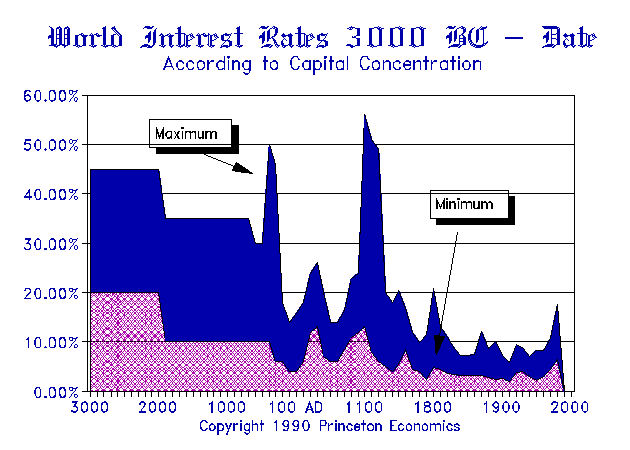

Before we get to the questions, a few general remarks: negative interest rates could not exist in an unhampered free market. They are an entirely artificial result of central bank intervention. The so-called natural interest rate is actually a non-monetary phenomenon – it simply reflects time preferences. Time preferences are an inviolable category of human action and are always positive.

Market interest rates consist of the natural interest rate plus two additional components: a price (or inflation) premium that reflects the expected decline in money’s purchasing power, and a risk premium or entrepreneurial profit premium that reflects the perceptions of lenders of a borrower’s creditworthiness and generates an entrepreneurial profit for those engaged in lending.

One often reads that interest is the “price” of money, but that is actually not quite correct. It is really a price ratio, the difference between the valuation of present against that of future goods. An apple one can obtain today will always be worth more than a similar apple one can obtain at some point in the future. If time preferences were to decline to zero, people would stop consuming altogether. All efforts would be directed toward providing for the future, but they would never see that future, because they would starve to death before it arrives.

…click on the above link to read the rest of the article…

{kind=link}