Drain, drain, drain…

Money from thin air going back whence it came from – circling the drain of a ‘no reinvestment’ black hole strategically placed in its way by the dollar-sucking vampire bat Ptenochirus Iagori Powelli.

Money from thin air going back whence it came from – circling the drain of a ‘no reinvestment’ black hole strategically placed in its way by the dollar-sucking vampire bat Ptenochirus Iagori Powelli.

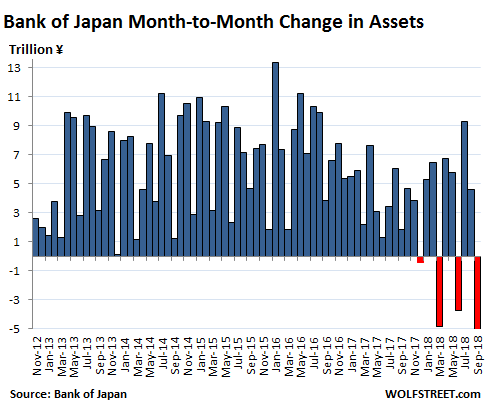

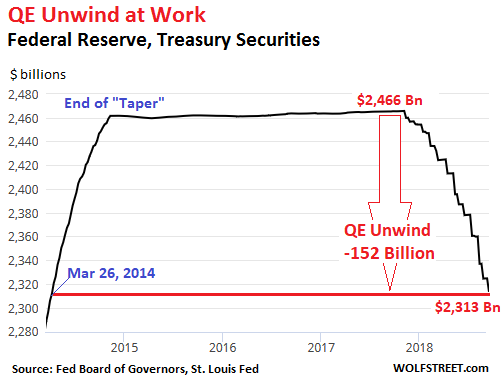

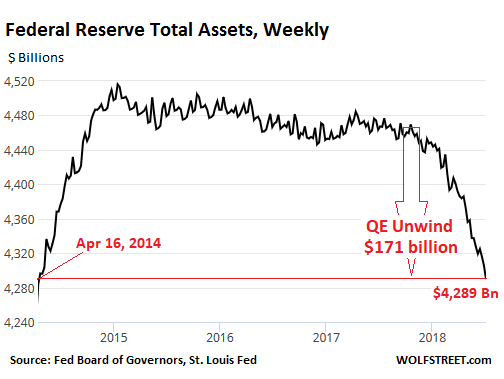

Our friend Michael Pollaro recently provided us with an update of outstanding Fed credit as of 26 December 2018. Overall, the numbers appear not yet all that dramatic, but the devil is in the details, or rather in the time frames one considers.

The pace of the year-on-year decrease in net Fed credit has eased a bit from the previous month, as the December 2017 figures made for an easier comparison – but that is bound to change again with the January data. If one looks at the q/q rate of change, it has accelerated rather significantly since turning negative for good in April of last year.

The pace of the year-on-year decrease in net Fed credit has eased a bit from the previous month, as the December 2017 figures made for an easier comparison – but that is bound to change again with the January data. If one looks at the q/q rate of change, it has accelerated rather significantly since turning negative for good in April of last year.

Below are the most recent money supply and bank lending data as a reminder that “QT” indeed weighs on money supply growth rates. It was unavoidable that the slowdown in money supply growth would have an impact on asset prices and eventually on economic activity.

Note that in the short to medium term, the effects exerted by money supply growth rates are far more important than any of the president’s policy initiatives, whether they are positive (lower taxes, fewer regulations) or negative (erection of protectionist trade barriers). The effects of changes in money supply growth are also subject to a lag, but in this case the lag appears to be over.

Any effects seemingly triggered by “news flow” are usually only of the very short term knee-jerk variety, and they are often anyway the opposite of what one would normally expect – particularly in phases when news flow actually lags market action (see the recent case of disappointingly weak PMI and ISM data). The primary trend cannot be altered by these short term gyrations.

…click on the above link to read the rest of the article…