Four times in as many months did ABC publish inaccurate statements about US shale oil. A glut of mis-information. This is unacceptable because it leads to wrong policy decisions and has ultimately damaging economic and financial consequences.

(1) “US shale producers pump like never before”

Just in time for last year’s X’mas we received these reassuring news:

Peak oil losing credibility as renewables shift accelerates

24/12/2015

“US shale producers are pumping like never before and adding to stockpiles”

http://www.abc.net.au/news/2015-12-24/peak-oil-losing-credibility-as-shift-to-renewables-accelerates/7052196

(2) “US virtually self-sufficient in oil”

This was broadcast on the 7 pm news (ABC channel 1)

16/1/2016

“The United States is now virtually self-sufficient in oil, while Saudi Arabia, the world’s biggest producer, has stepped up production to protect its market share.”

http://www.abc.net.au/news/2016-01-16/benefits-of-falling-oil-prices-not-fully-passed-on-to-motorists/7091862?section=business

(3) “US oil output rises”

Two months later the headline was:

Oil output rises even as US rig count falls to historic lows

18/3/2016

“The US Energy Information Agency said, despite the dramatic decline in rig numbers, production has steadily grown, indicating that drilling has becoming increasingly efficient”

http://www.abc.net.au/news/2016-03-18/oil-output-rises-even-as-us-rig-count-falls/7259566

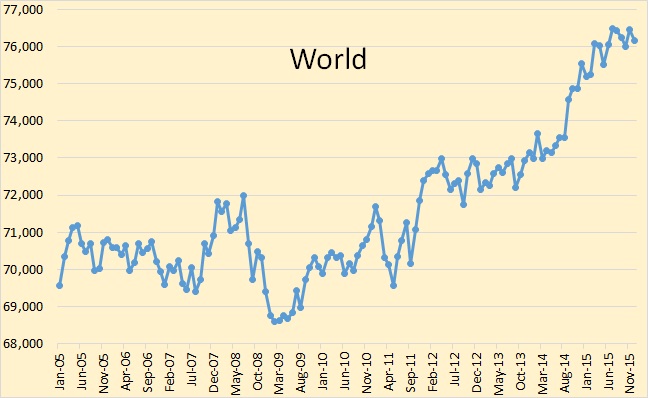

This ABC article included the following graph

Fig 1: EIA’s annual US oil production

Coming from this post by the EIA:

Hydraulic fracturing accounts for about half of current U.S. crude oil production

15/3/2016

http://www.eia.gov/todayinenergy/detail.cfm?id=25372

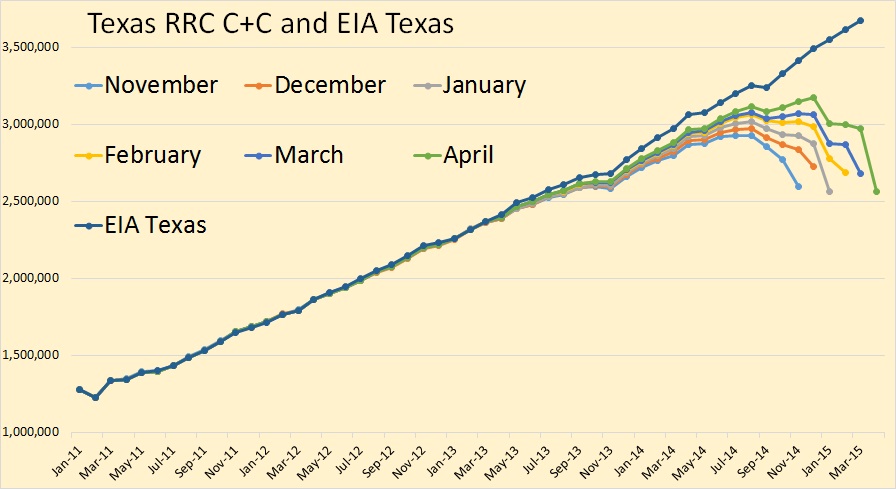

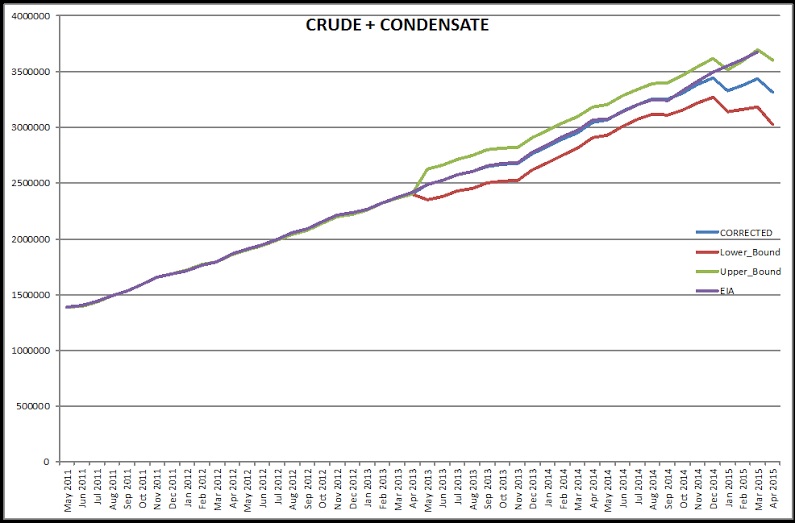

The graph shows that indeed 2015 production is higher than 2014 but the ABC author failed to look at monthly statistics where a turning point was already visible.

(4) “New shale oil technology the end of OPEC”

In the most recent article “Saudi Arabia to sell part of Aramco as part of shift from oil” we find this para:

New shale oil technology ‘the end of OPEC’

26/4/2016

“With US shale oil producers pumping more than ever before and Iran production coming back on line with US sanctions lifted, the planned Saudi reforms underscore the damage from falling revenues.”

http://www.abc.net.au/news/2016-04-26/saudi-arabia-to-sell-part-of-aramco-as-part-of-shift-from-oil/7360388?section=business

…click on the above link to read the rest of the article…

Since the possible double bottom at $26 formed on February 11th the oil price has staged a rally to $40 (WTI). Traders lucky enough to buy at $26 and sell at $40 have pocketed a tidy 54% profit. Very few will have been this lucky. The trade was stimulated by news that Saudi Arabia and Russia had agreed to not increase production this year which is hollow news since neither country could significantly increase production no matter how hard they tried. Profit taking has now driven WTI back towards $37 as of 1 April.

Since the possible double bottom at $26 formed on February 11th the oil price has staged a rally to $40 (WTI). Traders lucky enough to buy at $26 and sell at $40 have pocketed a tidy 54% profit. Very few will have been this lucky. The trade was stimulated by news that Saudi Arabia and Russia had agreed to not increase production this year which is hollow news since neither country could significantly increase production no matter how hard they tried. Profit taking has now driven WTI back towards $37 as of 1 April.