Home » Posts tagged 'dollar' (Page 2)

Tag Archives: dollar

The Cardinal Sin Of Investing: Permanent Impairment Of Capital

Victor Moussa/Shutterstock

The Cardinal Sin Of Investing: Permanent Impairment Of Capital

The key message was: When smart analysts independently find the same patterns in the data, it’s time to take notice.

Well, many of you did, by participating in this week’s Dangerous Markets webinar, which featured Grant and Lance.

In it, both went much deeper into the structural fragility of today’s financial markets and the many reasons why economic growth will remain constrained for years to come.

The excessive build-up of debt in the system — and the absolute dependence on its continued expansion to keep the economy from imploding — is, of course, seen as the prime risk to future growth.

As Lance demonstrates here with several of his excellent charts, so much leverage has been taken on that its servicing is increasingly stealing capital that would otherwise go to savings, consumption and productive investment. Going forward, the demands of the debt service will simply result in less and less capital available left over to grow the economy:

As financial assets are (supposed to be) valued on future growth prospects, lower forecasted growth demands lower valuations. Grant calculates that, should the US see another decade of 2% average annual GDP growth (and it has averaged less than that over the past decade), stock prices should be roughly half of what they are today to be considered fairly valued:

And Lance builds further on this, explaining how this moribund growth, coupled with America’s aging demographic trend, will simply savage the nation’s (already troublesomely underfunded) pension and entitlement systems:

…click on the above link to read the rest of the article…

The Federal Reserve Is Destroying America

The Federal Reserve Is Destroying America

Perhaps I should start with a disclaimer of sorts. Yes, I realize that the people working at the Federal Reserve, as well as the other central banks around the world, are just people. Like the rest of us, they have egos, fears, worries, hopes, and dreams. I’m sure pretty much all of them go home each night believing they are basically good and caring individuals, doing important work.

But they’re destroying America. They might have good intentions, but they are working with bad models. Ones that lead to truly horrible outcomes.

One of the chief failings of central banks is that they are slaves to an impossible idea; the notion that humans are free to pursue perpetual exponential economic growth on a finite planet. To be more specific: central banks are actually in the business of promoting perpetual exponential growth of debt.

But since growth in credit drives growth in consumption, the two are concepts are so intimately linked as to be indistinguishable from each other. They both rest upon an impossibility. Central banks are in the business of sustaining the unsustainable which is, of course, an impossible job.

I can only guess at the amount of emotional energy required to maintain the integrity of the edifice of self-delusion necessary to go home from a central banking job feeling OK about oneself and one’s role in the world. It must be immense.

I rather imagine it’s not unlike the key positions of leadership at Easter Island around the time the last trees were being felled and the last stone heads were being erected. “This is what we do,” they probably said to each other and their followers. “This is what we’ve always done. Pay no attention to those few crackpot haters who warn that in pursuing our way of life we’re instead destroying it.”

…click on the above link to read the rest of the article…

Venezuela On The Verge Of Revolution As Hyperinflated Currency Crashes To New Record Low

Venezuela On The Verge Of Revolution As Hyperinflated Currency Crashes To New Record Low

James Holbrooks points out that the people are starving. The government has gone full-on authoritarian, and now desperate human beings are dying in the streets. From an Associated Press report on Friday:

“Authorities in Venezuela say 12 people were killed overnight following looting and violence in the South American nation’s capital amid a spiraling political crisis.”

“Most of the deaths took place in El Valle, where opposition leaders say 13 people were hit with an electrical current while trying to loot a bakery protected by an electric fence.”

These are people without options, forced to turn to thievery to stay alive. And they died because of it.

On April 6, The Economist reported that over the past year, 74 percent of Venezuelans lost an average of 20 pounds. Venezuela, incidentally, has topped Bloomberg’s Economic Misery Index for the past three years.

The country began its slide downward into chaos with the election of President Nicolas Maduro, who immediately began implementing socialist programs and has since taken extreme measures to secure his position.

At the end of March, for instance, Maduro effectively shut down Venezuela’s congress — his primary political opposition — and gave those legislative duties to his puppet Supreme Court.

The latest news coming out of the South American nation — aside from the deaths of people trying to steal bread to live — is that General Motors, whose Venezuelan production facility was overtaken by local authorities, has now ceased all operations in the country.

To put that in perspective, consider that in 2016, only 3,000 vehicles were sold in Venezuela, a country of 30 million people.

…click on the above link to read the rest of the article…

Like Everything Else, History Repeats (Almost Exactly) Because Power Truly Corrupts

Like Everything Else, History Repeats (Almost Exactly) Because Power Truly Corrupts

If you read through the policy statement from July 2006 it sounds as if it were written by American central bank officials in July 2016. Swap out the year and the country and you really wouldn’t be able to tell the difference.

Japan’s economy continues to expand moderately, with domestic and external demand and also the corporate and household sectors well in balance. The economy is likely to expand for a sustained period…The year-on-year rate of change in consumer prices is projected to continue to follow a positive trend.

With incoming data judged as meeting predetermined criteria (they were somewhat “data dependent”, too), the Bank of Japan voted to raise their benchmark short-term rate but were careful, just like the Fed since December, to assure “markets” that it would be a gradual change only in the level of further “accommodation.”

The Bank has maintained zero interest rates for an extended period, and the stimulus from monetary policy has been gradually amplified against the backdrop of steady improvements in economic activity and prices…

…click on the above link to read the rest of the article…

We Know How This Ends, Part 2

We Know How This Ends, Part 2

In March 1969, while Buba was busy in the quicksand of its swaps and forward dollar interventions, Netherlands Bank (the Dutch central bank) had instructed commercial banks in Holland to pull back funds from the eurodollar market in order to bring up their liquidity positions which had dwindled dangerously during this increasing currency chaos. At the start of April that year, the Swiss National Bank (Swiss central bank) was suddenly refusing its own banks dollar swaps in order that they would have to unwind foreign funds positions in the eurodollar market. The Bank of Italy (the Italian central bank) had ordered some Italian banks to repatriate $800 million by the end of the second quarter of 1969. It also raised the premium on forward lire at which it offered dollar swaps to 4% from 2%, discouraging Italian banks from engaging in covered eurodollar placements.

The “rising dollar” of 1969 had somehow become anathema to global banking liquidity even in local terms.

The FOMC, which had perhaps the best vantage point with which to view the unfolding events, documented the whole affair though stubbornly and maddeningly refusing to understand it all in greater context of radical paradigm banking and money alterations. In other words, the FOMC meeting MOD’s for 1968 and 1969 give you an almost exact window into what was occurring as it occurred, but then, during the discussions that followed, degenerating into confusion and mystification as these economists struggled to only frame everything in their own traditional monetary understanding – a religious-like tendency that we can also appreciate very well at this moment.

At the April 1969 FOMC meeting, Charles A. Coombs, Special Manager of the System Open Market Account, reported that the bank liquidity issue then seemingly focused on Germany was indeed replicated in far more countries.

…click on the above link to read the rest of the article…

We Know How This Ends, Part 1

We Know How This Ends, Part 1

The finance ministers and representatives of central banks from the world’s ten largest “capitalist” economies gathered in Bonn, West Germany on November 20, 1968. The global financial system was then enthralled by a third major currency crisis of the past year or so and there was great angst and disagreement as to what to do about it. While sterling had become something of a recurring devaluation tendency and francs perpetually, it seemed, in disarray, this time it was the Deutsche mark that was the great object of conjecture and anger. What happened at that meeting, a discussion that lasted thirty-two hours, depends upon which source material you choose to dissect it. From the point of view of the Germans, it was a convivial exchange of ideas from among partners; the Americans and British, a sometimes testy and perhaps heated debate about clearly divergent merits; the French were just outraged.

The communique issued at the end of the “conference” only said, “The ministers and governors had a comprehensive and thorough exchange of views on the basic problems of balance-of-payments disequilibria and on the recent speculative capital movements.” In reality, none of them truly cared about the former except as may be controlled by the latter. These “speculative capital movements” became the target of focused energy which would not restore balance and stability but ultimately see the end of the global monetary system.

Some background is needed before jumping into West Germany’s financial energy. The gold exchange standard under the Bretton Woods framework had appeared to have lasted as far as this monetary conference, but it had ended in practicality long before. In the late 1950’s, central banks, the Federal Reserve primary among them, had rendered gold especially and increasingly irrelevant in settling the world’s trade finance.

…click on the above link to read the rest of the article…

The Confidence Game Is Ending

The Confidence Game Is Ending

I’m not saying the Fed’s rate hike is what caused the negative market reaction Thursday and Friday. The die for the economy has likely already been cast and right now it doesn’t look like a particularly promising roll. Raising a rate that no one is using by 25 basis points is not the difference between expansion and contraction. And a bit over a 3% drop in stocks isn’t normally much to concern oneself with; a 700 point move in the Dow ain’t what it used to be.

The pre-existing conditions for the rate hike were not what anyone would have preferred. The yield curve is flattening, credit spreads are blowing out and the incoming economic data is not improving. Inflation is running at a fraction of the Fed’s preferred rate and falling oil prices have been neither transitory nor positive for the economy, at least so far. The Fed is not unaware of this backdrop – they may not like it or acknowledge it publicly but they aren’t blind – but seems to have decided the financial instability consequences of keeping rates at zero longer are greater than any potential benefit. A sobering thought that.

…click on the above link to read the rest of the article…

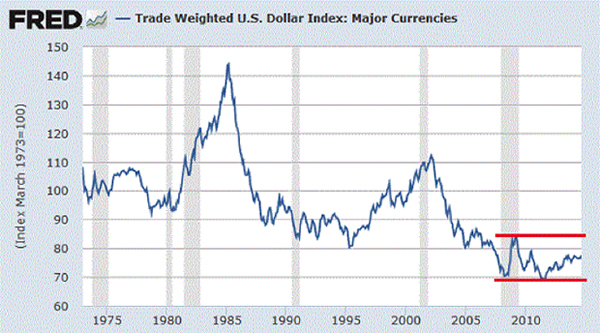

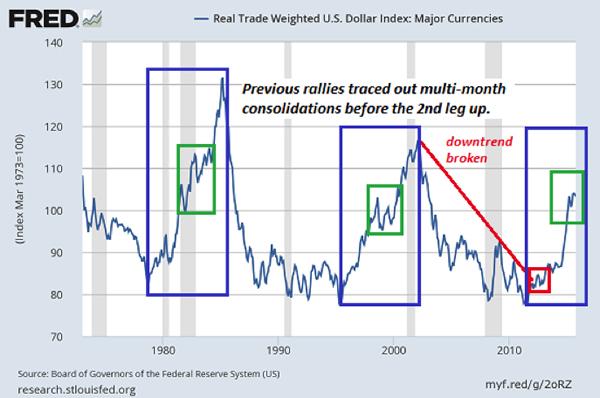

How Much Higher Can The U.S. Dollar Go?

How Much Higher Can The U.S. Dollar Go?

megainarmy/Shutterstock

Let’s start our examination of the U.S. dollar (USD) by recalling the chart from my August 2014 essay, Why the Dollar Could Strengthen—A Lot. At that point, the USD had moved modestly off its lows, and had yet to challenge long-term resistance around 80.

Here’s the same chart of the Real Trade-Weighted U.S. Dollar Index now:

The USD broke out of its multi-year downtrend and soared above 100. Needless to say, the USD did in fact strengthen a lot. After that initial leg up, the dollar has remained in a consolidation range for much of 2015. Though it recently broke out of a wedge/triangle formation to the upside, it’s not yet clear if this is a definitive move higher or more consolidation.

Is the Dollar Rally Done?

So is the dollar rally done, or could it move higher?

The long-term chart above (Real Trade-Weighted U.S. Dollar Index) offers some clues.

Our first observation is that trends in the USD tend to last for some time, so if this rally follows the pattern of previous rallies, it’s unlikely to have run its course in one year.

Secondly, previous rallies paused for a multi-month consolidation period before launching upward for the second leg of the long-term rally.

Thirdly, the USD rose sharply to previous peaks and then round-tripped back to the 80 level.

This raises the question: How high could the dollar rise in this rally?

…click on the above link to read the rest of the article…

World Holds Breath, Waits for “Death of the Dollar”

World Holds Breath, Waits for “Death of the Dollar”

Dismantling the dollar hegemony one yuan at a time.

I’ve been asked many times about the impending “death of the dollar.” I know some folks who expect the dang thing to die. They’re already envisioning the spectacle. An entire industry has sprung up to prepare and equip people for the moment when the dollar dies. It’s like insurance, the theme goes: hopefully you’ll never need it.

But the dollar is a human creation, a fiat currency. It doesn’t have a life of its own. It’s managed, rigged, and manipulated. It’s an accounting entity, a (lousy) store of value, and a means of handling transactions so you don’t have to barter your first-born for a Lexus.

As longs as it’s useful, the powers that be are going to keep it around. But over the long term, the dollar will do what it has done since the Fed was put in charge of it 100 years ago: it will lose value.

And the “strong dollar” these days? Ah, the irony!

It’s causing mayhem in the emerging markets where governments, corporations, and even consumers borrowed in dollars to save on interest. Now that their currencies are collapsing against the dollar, it’s getting very expensive to service these dollar debts, and they’re going to explode, and the holders of these debts are going to eat some big losses, unless they get bailed out again.

This “strong dollar” dents US exports and boosts imports. US corporations use it liberally as an excuse for their sorry revenues and earnings.

This is the value of the dollar in relationship to other currencies. These relationships are rigged to the nth degree. They go up and down and react to a million things, including central bank jawboning and monetary policies.

…click on the above link to read the rest of the article…

Monetary Metals Supply and Demand Report 9 August, 2015

Monetary Metals Supply and Demand Report 9 August, 2015

Withdrawing the Gold Bid

Last week, we left off with this:

“Something is happening with gold…”

It began in Dec 2008. To understand it, it is necessary to understand two principles. The first is that gold is money and the dollar is credit, which currently has nontrivial value. A dollar is worth 28.4mg gold. To understand the second, let’s look at how markets work at the mechanical level.

An assortment of well-known bullion coins and bars from all over the world

An assortment of well-known bullion coins and bars from all over the world

Photo via reisebank.de

Regular readers of this Report know that we emphasize the bid and ask prices as separate values. The people and forces involved in the bid price are different from those involved in the ask price. This is critical in our definition and calculation of the basis and cobasis. You cannot just assume that there is a real price, somewhere between the bid and ask. That may be a working approximation during normal market conditions. But it could be badly misleading.

Suppose there is stress in the market, a crisis impending or active. The bid recedes, and can even withdraw entirely. For example, what if the US Geological Survey were to say that there will be an earthquake in Los Angeles, 15 on the Richter scale, and nothing taller than a dollhouse will be left standing? You would not find any lack of offers to sell real estate. But what is the price of a house in LA? There wouldn’t be a bid in LA, and maybe not as far south as Chile, as far north as British Columbia, and as far east as the Mississippi River. The bid would come back into the market when the threat was over (perhaps at a much lower level).

…click on the above link to read the rest of the article…

Deflation Is Winning – Beware!

Deflation Is Winning – Beware!

Expect the ride to get even rougher

Deflation is back on the front burner and it’s going to destroy all of the careful central planning and related market manipulation of the past 6 years.

Clear signs from the periphery indicate that a destructive deflationary pulse has been unleashed. Tanking commodity prices are confirming that idea.

Whole groups of enterprises involved in mining and energy are about to be destroyed. And the commodity-heavy nations of Canada, Australia and Brazil are in for a very rough ride.

Whether the central banks can keep all of their carefully-propped equity and bond markets elevated throughout the next part of the cycle remains to be seen. We know they will try very hard. They certainly are increasingly willing to use any all tools at their disposal to keep the status quo going for as long as possible.

Whether it’s the People’s Bank of China stepping in to the market to buy 10% stakes in major Chinese corporations in a matter of weeks, the Bank Of Japan becoming the majority owner of key ETFs in the Japanese markets, or the Swiss National Bank purchasing $100 billion of various global equities, we see the same desperation. Equity prices are being propped, jammed and extended higher and higher without regard to risk or repurcussions.

It makes us wonder: Why haven’t humans ever thought to print their way to prosperity before?

Well, that’s the problem. They have.

And it has always ended up disastrously. History shows that the closest thing that economics has to an inviolable law is: There’s no such thing as a free lunch.

Sadly, all of our decision-makers are trying their hardest to ignore that truth.

First, The Fall….

So how will all of this progress from here?

We’ve always liked the Ka-Poom! theory by Erik Janzen which we explained previously like this:

…click on the above link to read the rest of the article…

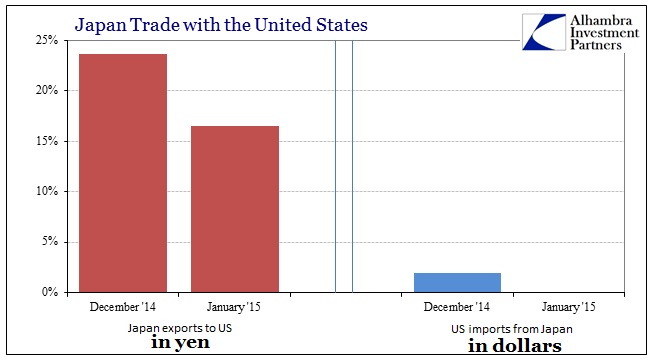

The Monetary Illusion Again in Trade

The Monetary Illusion Again in Trade

Just as a follow-up to further highlight and emphasize the “monetary illusion” of currency devaluation in this closed environment, the yen’s returned devaluation against the “dollar” more recently has renewed confusion (or intentional misdirection) about what Abenomics is supposedly accomplishing. Taken solely from the perspective of the Japanese internally, exports to the US are once more growing, and doing so rather sharply. December’s year-over-year gain, in yen, was almost 24% while January came in at an equally robust 16.5%.

Taken by themselves without context, it would seem great fortune and monetary capability to gain in exports at such huge growth rates. But, as I have shown time and again, what goes out of Japan is matched by what comes in to the US. For all that buzz over huge export growth, nothing much shows up on this end.

Both months were positive in “dollars” but barely and thus no actual growth took place. Economists and central bankers even concede the disparity, but don’t much care about it. They simply assume that Japanese exporters now flush with more yen will hire more workers and pay the ones they have even more, igniting that virtuous circle of “aggregate demand.” In reality, why would they do that?

…click on the above link to read the rest of the article…

Replacing the Dollar | Armstrong Economics

Replacing the Dollar | Armstrong Economics.

The conspiracy crowd keep swearing the dollar has to collapse and remain clueless that the world is in serious trouble. The impact of debt is far worse outside the USA than inside yet their myopic vision blinds them to the truth. Taxes are so high in Europe and this renders it is impossible to grow the economy out of recession. Debt use to be debt and the theory was it would be less inflationary to borrow than to print. However, after 1971, debt became merely currency that paid interest as it began in the 1860s. The dollar is now the reserve currency and not even the USA can prevent that – there is no alternative !!!!!!!!

It is now MORE inflationary to borrow than to print for now the currency just pays interest. You trade markets and post TBills as collateral. So TBills are now cash paying interest. Moving toward electronic money to collect even more taxes will divide the economy with a greater division between above and below ground. If you could not borrow on government paper, then government could not sell it. So they are trapped in a doomed system that cannot be sustained and the press is controlled to ensure the public remain blinds, death, and dumb about the crisis.

Many insurance companies and pension funds buy government debt for it is considered “riskless”. We are facing a monumental crisis of tremendous proportion. However, this isNOT about the dollar, it is about global debt and taxes. We have reached the peak of the bell curve that Art Laffer articulated correctly. The higher the taxes the lower the growth and the greater the debt. Rising interest rates expand government debt. Government debt defaulting takes down all pension funds. This is a huge problem. We are not in a position to handle the massive uprising when people wake up and realize they have been really is been living a dream.

…click on the link above for the rest of the article…