Home » Posts tagged 'bankruptcy' (Page 2)

Tag Archives: bankruptcy

The Great American Shale Oil & Gas Massacre: Bankruptcies, Defaulted Debts, Worthless Shares, Collapsed Prices of Oil & Gas

The Great American Shale Oil & Gas Massacre: Bankruptcies, Defaulted Debts, Worthless Shares, Collapsed Prices of Oil & Gas

The bankruptcy epicenter is in Texas.

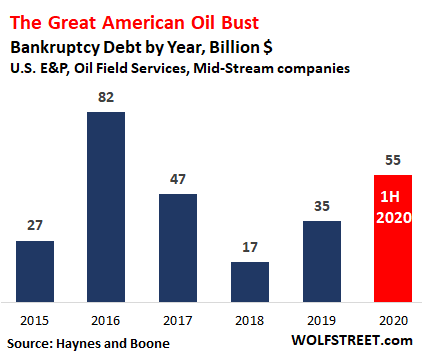

The Great American Oil Bust started in mid-2014, when the price of crude-oil benchmark WTI began its long decline from over $100 a barrel to, briefly, minus -$37 a barrel in April 2020. Bankruptcies of US companies in the oil and gas sector started piling up in 2015. In 2016, the total amount of debt listed in these filings hit $82 billion. Bankruptcy filings continued, with smaller dollar amounts of debt involved. In 2019, the shakeout got rougher.

And this year promises to be a banner year, as larger oil-and-gas companies with billions of dollars in debt collapsed, after having wobbled through the prior years of the oil bust.

The 44 bankruptcy filings in the first half of 2020 among US exploration and production companies (E&P), oilfield services companies (OFS), and “midstream” companies (gather, transport, process, and store oil and natural gas) involved $55 billion in debts, according to data compiled by law firm Haynes and Boone. This first-half total beat all prior full-year totals of the Great American Oil Bust except the full-year total of 2016:

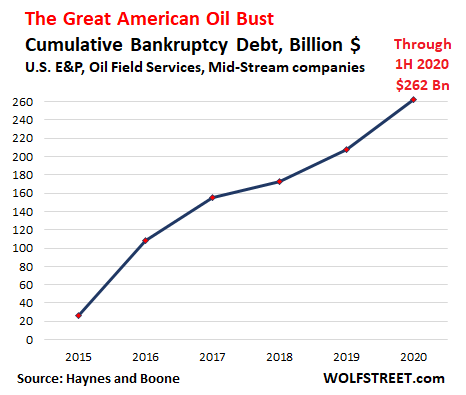

The cumulative amount of secured and unsecured debts that the 446 US oil and gas companies disclosed in their bankruptcy filings from January 2015 through June 2020 jumped to $262 billion:

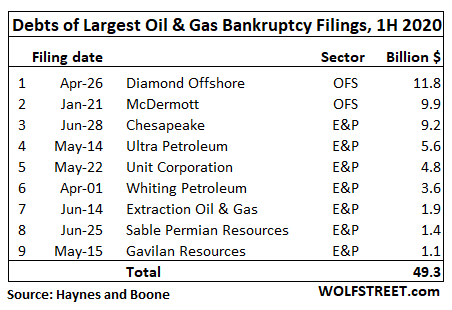

The three biggies: In the first half of 2020, nine of the 44 US oil and gas companies that filed for bankruptcy listed over $1 billion in debts, including the three biggies with debts ranging from $9 billion to nearly $12 billion, according to data by Haynes and Boone.

These three companies – oil-field services companies Diamond Offshore and McDermott and natural-gas fracking pioneer Chesapeake – are the biggest in terms of debts that have toppled in the Great American Oil Bust so far. Those three companies combined listed $31 billion in debts, accounting for 56% of the $55 billion in total debts listed by all 44 companies to file so far this year:

…click on the above link to read the rest of the article…

Chesapeake Files For Bankruptcy, Wiping Out $7 Billion In Debt And Any Existing Equity Value

Chesapeake Files For Bankruptcy, Wiping Out $7 Billion In Debt And Any Existing Equity Value

After years of melting, the Chesapeake icecube is finally history: at exactly 350pm on Sunday afternoon, the company that launched the US shale boom, finally gave up and filed for a pre-packaged bankruptcy in the Southern District of Texas. In so doing, the company with roughly $9.5 billion in debt has become one of the biggest victims of a spectacular collapse in energy demand from the virus-induced global recession, and follows the collapse of another high-flyer in the US oil patch, Whiting Petroleum, which filed for Chapter 11 at the start of April after championing what was once the premiere U.S. shale field, the Bakken of North Dakota.

As part of its prepack agreement, Chesapeake announced that it had entered into a Restructuring Support Agreement (“RSA”) with 100% of the lenders under its revolving credit facility, holders of approximately 87% of the obligations under its Term Loan Agreement, approximately 60% of its senior secured second lien notes due 2025, and approximately 27% of its senior unsecured notes, pursuant to which Chesapeake will implement a Chapter 11 plan of reorganization to eliminate approximately $7 billion of debt.

Of course, since 73% of unsecured bondholders refused to sign off on the deal, expect a very vicious bankruptcy fight over the recoveries, as hedge funds that accumulated positions in the bonds unleash hell in their fight with the secureds (even as the equity committee claims that all classes above it should be unimpaired).

Also, we have some bad news for Jefferies, which won’t be able to repeat its hilarious attempt to fund the company in bankruptcy by selling stock to Robnhood daytraders: as part of the RSA, the Company has secured $925 million in debtor-in-possession financing lenders under Chesapeake’s revolving credit facility. The DIP will provide Chesapeake the capital necessary to fund its operations during the Court-supervised Chapter 11 reorganization proceedings.

…click on the above link to read the rest of the article…

30% Of U.S. Shale Drillers Could Go Under

30% Of U.S. Shale Drillers Could Go Under

U.S. shale was one of the big losers of the Saudi-Russian price war that many saw as a war on U.S. shale. Producers scrambled to stay afloat as prices sank back to lows not seen since 2016, and they are still scrambling. Banks are giving them the cold shoulder, worried that many will not be able to pay their debts. Is there a way out? According to various forecasting agencies, there is, but it will take a while. A Bloomberg analysis of forecasts for the shale industry made by outlets such as the International Energy Agency, energy consultancy Rystad, IHS Markit, Genscape, and Enervus suggests shale will be back on its feet by 2023, with production back to over 12 million bpd.

This is not a long time for a full recovery, really, especially given the current circumstances, including shut-in wells, abandoned drilling plans, tight cash, and, for many, looming bankruptcies.

As much as 30 percent of shale drillers could go under if oil prices fail to move substantially higher, Deloitte said in a recent study, as quoted by CNN. These 30 percent, the firm said, are technically insolvent at oil prices of $35 a barrel. Right now, West Texas Intermediate is higher than $35 but not by much. Oil is now trading closer to $35 than to $50—the level at which most shale drillers will be making money.

And they need to make money: banks have started cutting credit lines for industry players as they reassess their assets and the production that they promised would be realized from these assets. According to calculations by Moody’s and JP Morgan, cited by the Wall Street Journal, banks could reduce asset-backed loan availability for the industry by as much as 30 percent, which translates into tens of billions of dollars.

…click on the above link to read the rest of the article…

The Unique Ways Oil Companies Are Looking To Avoid Bankruptcy

The Unique Ways Oil Companies Are Looking To Avoid Bankruptcy

Many U.S. shale firms have cruised through the past couple of years by borrowing money and drilling new wells, making the United States the world’s top crude oil producer. The strategy worked for a while, especially when oil prices were around $60 a barrel.

But this year’s oil price crash exposed the financial vulnerability of many U.S. shale companies who are now fighting for survival. All producers across the U.S. patch pulled back production volumes in April and May in response to the collapse in prices.

For some oil and gas firms, reduced capital budgets will not be enough to save them from defaulting on debt or seeking restructuring as cash flows are shrinking, while the window of access to capital markets and new debt remains, for the most part, closed.

Those firms who choose not to seek (or are not forced to seek) protection from creditors via Chapter 11 restructuring could look at other options to avoid bankruptcy, some of which may be a little unconventional.

Today, unconventional may be an understatement when it comes to describing the oil industry’s state of affairs. All options – regardless of how (un)common they are – are on the table for struggling oil producers.

Industry consolidation, private equity firms acquiring assets or distressed companies, banks ending up holding oil and gas assets, or power utilities buying their providers of energy could be some of the options that oil firms might consider, Suzy Taherian, who worked with Exxon and Chevron at the start of her career, writes in Forbes.

Mergers & Acquisitions Hit By Uncertainty

U.S. shale firms have fewer financing options now than they did in the 2015-2016 downturn. Thus could drive consolidation in the industry with some attractive M&A opportunities emerging, according to Robert Polk, principal analyst with Wood Mackenzie’s U.S. Corporate Research team, covering Lower 48 independents.

…click on the above link to read the rest of the article…

Coronavirus Bankruptcy Pandemic Continues

Coronavirus Bankruptcy Pandemic Continues

Hertz has now joined the ranks of filing for bankruptcy as this lockdown has caused car rentals to crash to virtually zero. Of course, Climate Change activists led by Bill Gates are celebrating. They cheer every bankruptcy they have managed to create with the absurd lockdowns were the first time in history you quarantine the entire population rather than just those who are sick.

The total economic destruction we have said is about $30 trillion in businesses. If we add real estate which cannot be sold, that is most likely $35-$45 trillion. Then add on top of that the coming wave of sovereign bond defaults which will include emerging markets that have witnessed their exports collapse. Global GDP is about $90 trillion. The global bond market is about $100 trillion.

Commercial Real Estate is worth about $32 trillion and Agricultural Real Estate about $27 trillion. Total residential Real Estate is about $170 trillion at the end of 2019. If we have to put a number of that we reach about $230 trillion.

The total world equity market at the end of 2019 was nearly $90 trillion.

Therefore, if we add up what I call Capital Formation, this is the combination of real estate, equities, and bonds. This number works out to be about $420 trillion.

Consequently, the economic contraction in just the current GDP of $90 trillion is about $30 trillion, and Capital Formation is probably about $120 trillion illiquid out of $420 trillion if they even tried to sell. Anyone who thinks that governments can possibly stimulate their way out of this or create hyperinflation by spending even $10 trillion are not taking into consideration the full scope of this economic collapse.

…click on the above link to read the rest of the article…

California Just Put Washington in this Economic “Catch-22”

California Just Put Washington in this Economic “Catch-22”

Government bailouts are being revived, and this time, unlike during the 2008 recession, it appears large financial companies won’t be the only ones asking for help.

The problem is, the government may not be able to help this time.

In response to a bloated state budget and a massive debt of over $550 billion, Newsmax reports that California Governor Gavin Newsom is looking for a bailout from the federal government:

Without an infusion of at least $14 billion from Congress, Newsom said the state would have to cut billions to public schools, not to mention hundreds of millions for preschool, child care and higher education programs. It’ll also need to eat into health benefits for the poor, among other things.

“The enormity of the task at hand cannot just be borne by a state,” Newsom said. “The federal government has a moral and ethical and economic obligation to help support the states.”

Obviously, Newsom’s decision to impose lockdowns in response to the coronavirus pandemic, resulting in more than 746,000 unemployed, partly explains the sudden need for cash.

Economist Robert Wenzel thinks the “lockdown is projected to lead to a state budget shortfall this year of $54 billion,” which is bound to make things more complicated.

Wenzel added another sharp critique of Newsom’s request for a bailout, and a comparison to Greece’s economic bust in 2007:

[Newsom] is now in begging mode just like Greece was, but, whereas a lot of Greece’s financial trouble was about paying off old debt, California’s problem is about running the current state government (and also local governments).

It sure seems like California has been playing a dangerous debt game, first ignoring economic realities prior to the pandemic, and then asking the federal government to send bags of cash so things can keep running smoothly.

…click on the above link to read the rest of the article…

What is Really the Game with the Bailouts?

What is Really the Game with the Bailouts?

There is a major crisis economically unfolding and the markets are not yet taking into account the seriousness of the economic damage. I have explained that this is a Coronavirus Bankruptcy Pandemic which has put about 30% of the retail service industry in the crosshairs of insolvency. But there are smaller municipal governments that are also bankrupt as we see with some of the first filings starting to unfold here in May.

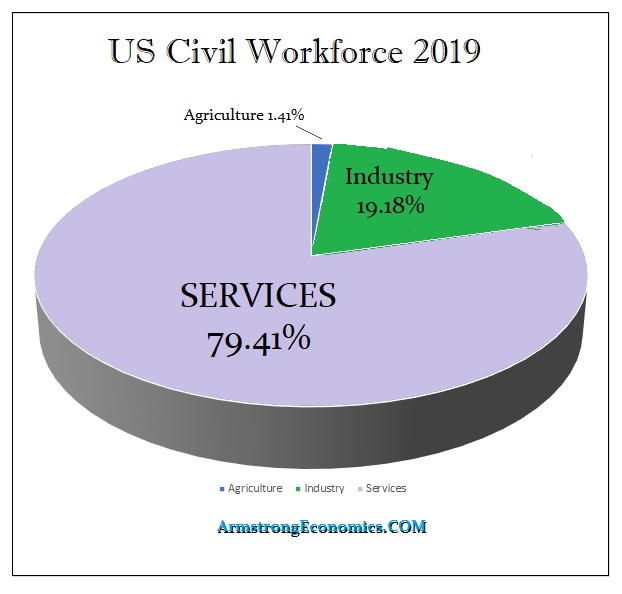

With nearly 80% of the civil workforce employed in the service sector, these schemes of keeping the economy locked down are profoundly dangerous. They fail to realize that this is undermining society in a major way that it is not going to return to normal even with Bill Gates’ certificates to prove you have been vaccinated by him personally.

The Democratic states are refusing to open up when there is no real justification to keep their economies closed. What is really going on behind the curtain is a clever trick. The $1 trillion that Pelosi was stuffing in the Democratic Bill is money to bail out state and municipal governments which have been going broke because of their unfunded pensions.

The scheme is to crash their economies and then blame everything on the virus and then blame Trump for not bailing them out for the 2020 election. This is a very clever scheme being relayed in whispers from behind the curtain. They are using this virus as cover to bail out 70 years of fiscal mismanagement.

Bankrupt Cities And States Get The National Disaster They’ve Been Hoping For

Bankrupt Cities And States Get The National Disaster They’ve Been Hoping For

The people running states like New Jersey and cities like Chicago know they’re broke. Ridiculously generous public employee pensions – concocted by elected officials and union leaders who had to have understood that they were writing checks their taxpayers couldn’t cover – are bleeding them dry, with no political solution in sight.

They also know that they have only two possible outs: bankruptcy, or some form of federal bailout. Since the former means a disgraceful end to local political careers while the latter requires some kind of massive crisis to push Washington into a place where a multi-trillion dollar state/city bailout is the least bad option, it’s safe to assume that mayors and governors – along with public sector union leaders – have been hoping for such a crisis to save their bacon.

And this year they got their wish. The country is on lockdown, unemployment is skyrocketing and mayors and governors now have a plausible way to rebrand their criminal mismanagement as a “natural disaster” deserving of outside help.

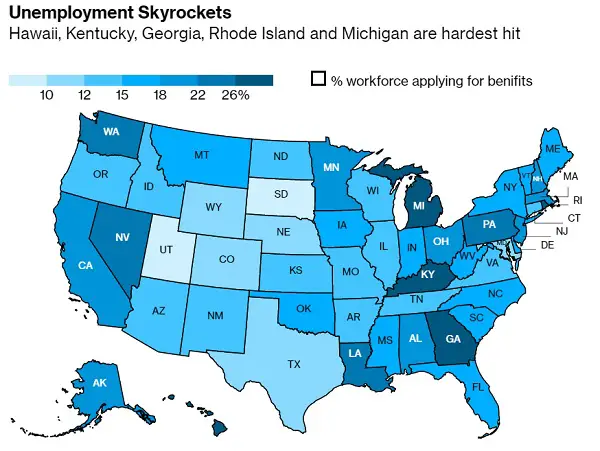

Here, for instance, is an estimate of how high unemployment will spike for various states. Note that overall it’s brutal, but the distribution isn’t what you might expect:

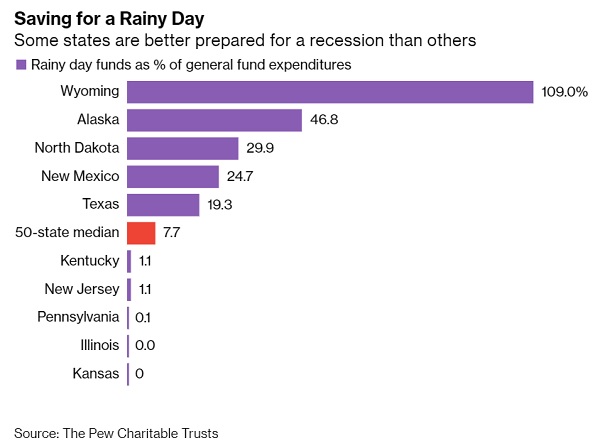

And here’s a table of state rainy day funds (i.e., cash on hand). To their credit, oil-producing states had the discipline to save against that commodity’s inevitable price fluctuations. Other states apparently didn’t see the need:

Illinois, which has the most underfunded pensions but, interestingly, a relatively healthy labor market, apparently had its natural disaster bailout plan prepped and printed before COVID-19 was invented and released. Because governor Gov. J.B. Pritzker almost instantly had his hand out for – get this – $41 billion, a sum equal to three times the state’s estimated pandemic-related revenue loss in the coming year. Overall, governors have asked for about $500 billion in aid.

…click on the above link to read the rest of the article…

FIRST SHALE OIL DOMINO TO FALL: More to Follow

FIRST SHALE OIL DOMINO TO FALL: More to Follow

In a stunning news release, Continental Resources, the largest shale producer in the Bakken, is shutting in most of its production in the region. That is one hell of a lot of output to shut-in as Continental Resources was producing over 200,000 barrels per day in the Bakken at the end of 2019.

From the data on Shaleprofile.com, Continental Resources had over 2,200 wells in the North Dakota and Montana Bakken producing oil and gas during February this year. How many wells will Continental’s Harold Hamm shut in the Bakken?? And how many will be brought back online, at to what cost, when the market recovers??

According to Reuters, Continental Resources halts shale output, seeks to cancel sales:

April 23 (Reuters) – The largest oil producer in North Dakota has halted most of its production in the state, notifying some customers it would not supply crude at current pricing, according to people familiar with the matter.

Continental Resources Inc, the company controlled by billionaire Harold Hamm, stopped all drilling and shut in most of its wells in the state’s Bakken shale field, said three people familiar with production in the state. North Dakota is the second-largest oil-producing state in the United States after Texas.

This is terrible news for the U.S. Shale Oil Industry because $200 billion in debt is due over the next four years. How are they going to repay this debt if shale companies stop drilling and shutting in production??

If we look at the top five shale oil producers in the Bakken, Continental Resources was clearly ahead of the pack:

This chart from Shaleprofile.com shows that Continental Resources produced more than 200,000 barrels per day in the Bakken at the end of 2019. Hess, which is the second-ranked company, followed by a wide margin at 145,000 barrels per day. Interestingly, the third-largest producer in the Bakken is Whiting Petroleum that just filed for Bankruptcy on April 1st.

…click on the above link to read the rest of the article…

Bankrupting America

Bankrupting America

Source: AP Photo/Alex Brandon

Two weeks ago, President Donald Trump signed the largest stimulus bill in U.S. history: more than $2 trillion.

For once, both Republicans and Democrats agreed. The Senate voted 96-0. The House didn’t even bother with a formal vote.

At the White House, a reporter asked the president, pointing out that the bill includes $25 million for the Kennedy Center, “Shouldn’t that money be going to masks?”

“The Kennedy Center has suffered greatly because nobody can go there,” Trump responded. “They do need some funding. And look — that was a Democrat request. That was not my request. But you got to give them something.”

“Something” they got. The bill includes $25 million for Congressional salaries, $50 million for an Institute of Museum and Library Services and lots of other wasteful things.

Only a few politicians were wary. Rep. Thomas Massie complained that he wasn’t even allowed to speak against the bill.

Rep. Alex Mooney asked: “How do you pay for it? Borrow it from China, borrow it from Russia? Are we going to print the money?”

Those are good questions.

Our national debt is already $24 trillion. Now it will jump, percentage-wise, to where Greece’s debt was shortly before unemployment there hit 27%.

Greece was bailed out by the European Union. But the United States can’t be bailed out by others.

How will we pay off our debt? That’s the topic of my new video.

There are really three options:

1. Raise taxes.

2. Print money.

3. Default.

Let’s consider each:

1. Raising taxes on rich people is popular. Even Michael Bloomberg wants “higher taxes on billionaires” like him.

But raising taxes on the rich often kills the wealth and jobs some rich people create. And it won’t solve our debt problem. Even if we took all the billionaires’ wealth — reducing their net worth to zero — it would cover only an eighth of our debt.

…click on the above link to read the rest of the article…

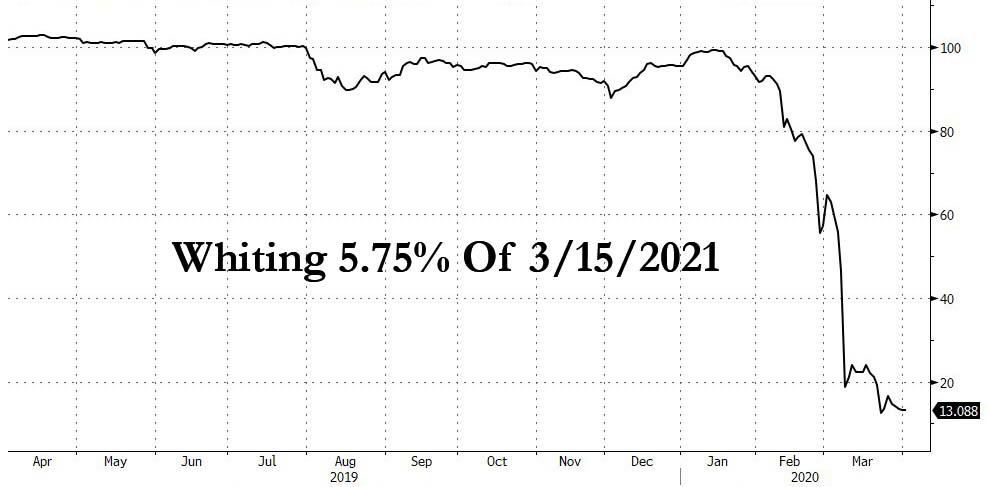

Whiting Petroleum Files For Prepackaged Bankruptcy

Whiting Petroleum Files For Prepackaged Bankruptcy

Talk about a coincidence: just as we were discussing why April would be “apocalyptic” for the oil industry, as Saudi Arabia just unleashed an unprecedented record amount of oil to buyers in a scramble to put its high-priced competitors out of business, warning that “countless oil producers would file for bankruptcy”, former shale darling Whiting Petroleum did just that, filing a pre-packaged Chapter 11 deal in the Southern District of Texas Bankruptcy Court after reaching an agreement with certain note holders to pursue a “comprehensive” and “consensual” financial restructuring.

Whiting, which in Q4 pumped 123,000 bpd of which 80,000 bpd was nat gas, said it concluded that given a “severe downturn” in oil and gas prices resulting from the Saudi Arabia-Russia oil price war and COVID-19-related impact on demand a financial restructuring was the “best path forward.” Creditors may disagree: the company’s bonds due March 2021 were trading at par as recently as mid-January, even though we warned as far back as 2015 that it would be the first company to go under: truly a testament to how idiotic the junk bond market has been for the past 4 years.

The company said that the plan provides for de-leveraging of capital structure by more than $2.2 billion, and listed $1-$10 billion in debt and more than $585 million of cash on its balance sheet, noting that it expects to have sufficient liquidity to meet its financial obligations during the restructuring without the need for additional financing.

More importantly, it will continue to operate its business and pump oil for the duration of the Chapter 11 proceedings, meaning that oil production won’t decline by even one drop.

The bankruptcy press release is below:

…click on the above link to read the rest of the article…

Major Freight Carrier Bankrupted, Leaving 3,000 Truckers Jobless, Many Stranded On Highways

Major Freight Carrier Bankrupted, Leaving 3,000 Truckers Jobless, Many Stranded On Highways

As the manufacturing recession gains momentum, the largest U.S. truckload carrier filed for bankruptcy Monday morning, leaving 3,000 truck drivers and 500 administrative positions without a job two weeks before Christmas.

Indianapolis-based Celadon filed for voluntary Chapter 11 bankruptcy in the early hours on Monday morning.

Around 1:43 am est., headlines via Reuters confirmed the bankruptcy and how all domestic and international operations have been halted.

- CELADON GROUP, INC. AND AFFILIATES COMMENCE VOLUNTARY CHAPTER 11 CASES

- CELADON GROUP INC – CELADON ALSO ANNOUNCED THAT IT WILL SHUT DOWN ALL OF ITS BUSINESS OPERATIONS EFFECTIVE AS OF TODAY, MONDAY, DECEMBER 9, 2019

- CELADON GROUP INC – THIS SHUT DOWN DOES NOT INCLUDE TAYLOR EXPRESS BUSINESS HEADQUARTERED IN HOPE MILLS, NORTH CAROLINA

- CELADON GROUP – CELADON INTENDS TO USE ITS CHAPTER 11 PROCEEDINGS TO WIND DOWN ITS GLOBAL OPERATIONS

- CELADON GROUP INC – HAVE FILED VOLUNTARY PETITIONS FOR RELIEF UNDER CHAPTER 11 OF BANKRUPTCY CODE IN U.S. BANKRUPTCY COURT FOR DISTRICT OF DELAWARE

- CELADON GROUP INC – TO SUPPORT WIND DOWN OF OPERATIONS, CELADON’S LENDERS HAVE AGREED TO PROVIDE INCREMENTAL DEBTOR-IN-POSSESSION FINANCING

Celadon CEO Paul Svindland told WTHR Indianapolis that the entire company would shut down business operations except for the “Taylor Express” subsidiary in Hope Mills, North Carolina, on Monday.

Svindland said the company will guarantee delivery of their last loads and will instruct drivers where to leave trucks.

“We have diligently explored all possible options to restructure Celadon and keep business operations ongoing, however, a number of legacy and market headwinds made this impossible to achieve,” Svindland said in a press release.

“Celadon has faced significant costs associated with a multi-year investigation into the actions of former management, including the restatement of financial statements…

…click on the above link to read the rest of the article…

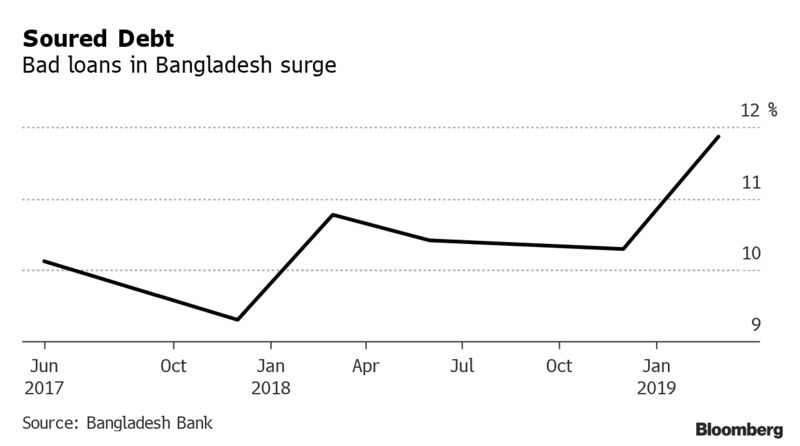

Bangladesh’s Central Bank Offers Amnesty To Delinquent Borrowers, Prompting Mass Default

Bangladesh’s Central Bank Offers Amnesty To Delinquent Borrowers, Prompting Mass Default

Bangladesh’s Central Bank in May introduced an amnesty program that allowed delinquent borrowers to make a small upfront payment and then pay off the rest of their debt over 10 years at favorable interest rates, according to Bloomberg.

However, the plan also triggered a rush by healthy companies to reschedule debt on the same terms which, in turn, now threatens to overwhelm the country’s banks.

The program is also seen as encouraging those with debt to default. Big surprise, right?

Anis A. Khan, managing director of Dhaka-based Mutual Trust Bank Ltd. said:

“I’m traumatized by non-performing loans. Borrowers have been using every excuse they can find — from a death in the family to political uncertainty — to try to get onto the central bank program.”

The initiative is available to borrowers until September 7 and created a “perverse incentive” to default. Now, the country is expecting that nonperforming loans may rise significantly from 11.9% in March as a result of the program.

The upfront payment was lowered to 2% from 10% for those who are defaulting for the first time. The maximum interest rate over the next 10 years was set at 9%, even if borrowers were paying as high as 15% previously.

And like all other great “Band-Aid” fixes to debt problems, the initiative has backfired: it has created a sense among Bangladeshi companies that people can get away without paying back their loans. That, in turn, poses a threat to the wider economy and a banking system that is already overwhelmed with defaults.

The central bank, meanwhile, says that the policy will help revive lending growth in an economy that is dependent on attracting investment to sustain growth. Asian Development Bank predicts that the country’s economy will expand 8% over the next two years.

Shitangshu Kumar Sur Chowdhury, banking reforms adviser at Bangladesh Bank said:

…click on the above link to read the rest of the article…

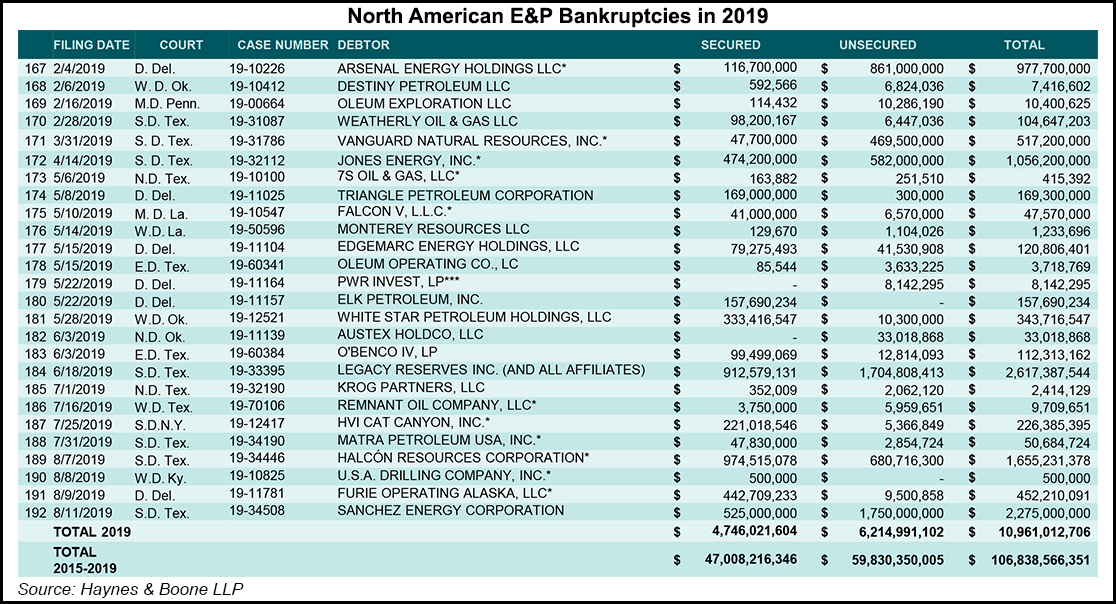

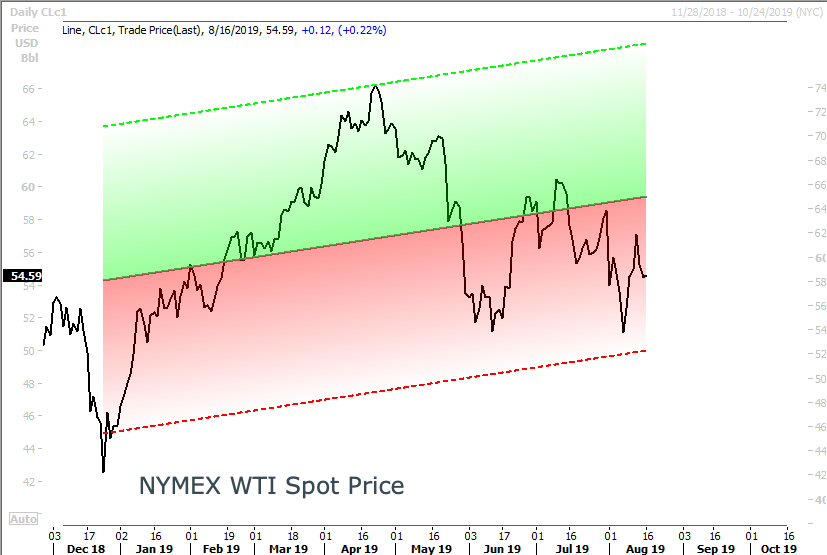

Bankruptcy Filings Rise Among US Energy Producers, Report

Bankruptcy Filings Rise Among US Energy Producers, Report

According to a new report from law firm Haynes and Boone LLP, bankruptcies in the upstream sector are increasing this year as energy spot prices remain subdued amid a cyclical downshift in the economy.

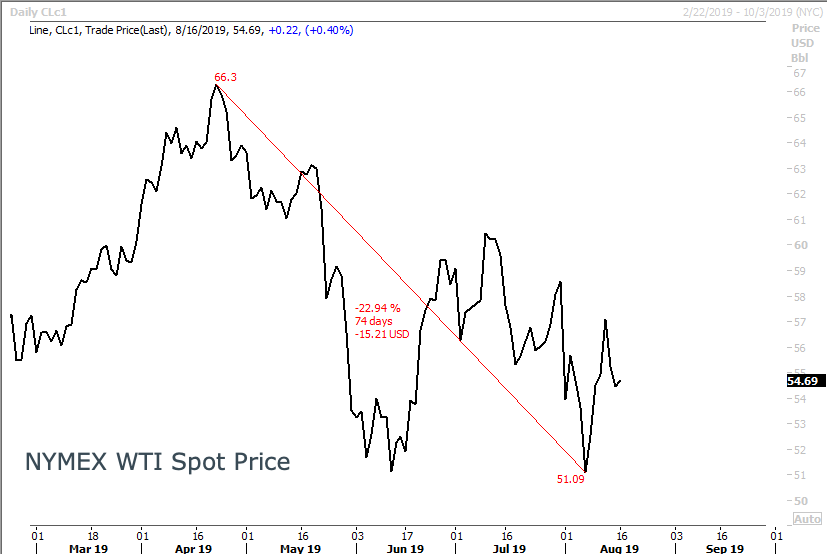

So far, 26 exploration and production (E&P) firms have filed for bankruptcy through mid-August, with debts totaling $10.96 billion. The firm noticed a surge in bankruptcies began in May, following a -23% correction in WTI prices from mid-April to mid-June.

In 2018, 28 E&P firms filed for bankruptcy, posting $13.2 billion in debt, while 24 firms asked for protection in 2017 with $8.5 billion in debt. The firm points out that insolvencies in the energy patch are gaining momentum.

“So far this year there has been an uptick in the number of filings,” Haynes & Boone said.

Oil and gas prices have remained depressed for 2019.

The law firm said it’s hard to tell if a new bankruptcy wave is imminent, but said, “some stakeholders may have given up hope that resurgent commodity prices will bail everyone out,” especially operators who have been on the verge of bankruptcy.

“For these producers, the game clock has run out of time to keep playing ‘kick the can’ with their creditors and other stakeholders,” the firm warned.

Buddy Clark, a Haynes & Boone partner, told Reuters that many of 2019’s bankruptcies are pre-planned, Chapter 11 restructurings, where creditors agree in advance on restructuring plans.

“I don’t think you will see a lot of Chapter 7 (liquidations),” he said. “When you see Chapter 7s is when there are no assets left. Typically, there are always assets left.”

Natural Gas Intelligence believes a bankruptcy wave for the upstream sector could be nearing. This is because operators across the country have been scaling back since oil crashed -44% in 4Q18. Producers have been faced with margin compression, high debt loads, and oversupplied markets so far this year.

…click on the above link to read the rest of the article…

A World With no Debt and no Bankruptcies: How About Social Credit as Money?

A World With no Debt and no Bankruptcies: How About Social Credit as Money?

Mark Twain had a genial idea with his story “The One Million Pound Bank Note” published in 1853. It was such a huge amount of money that it couldn’t be exchanged, yet it gave its owner all sorts of perks and goods. It was, in a certain way, an anticipation of what we call today the “social credit score” obtained on the various social media services on the Web. It is a form of money that can be owned, but cannot be exchanged — in most cases, you can’t even go negative with your social credit. So, no debt, no bankruptcy. Would it be possible to build a financial system based on this concept? Not easy, but also an idea being examined nowadays, especially in China with their state-owned social credit system (shèhuì xìnyòng tǐxì). The text below is derived from the chapter on financial collapses of my new book “The Seneca Strategy,” to be published in later 2019.

The whole problem of financial collapses is the result of the existence of money. But what is money exactly? Without going into the various theories of money that economists are still discussing, we can say that once, money was something that everybody agreed on: a weight of precious metals. After all, the British currency is still defined in units of weight, even though one pound (in monetary terms) does not weigh a pound (in physical terms). Still, up to not too long ago, money was simply a token representing a physical entity, typically a certain weight of gold and silver. But things changed a lot with time and, with the 20th century, the convertibility of the dollar into precious metals was more theoretical than real. In 1971 president Nixon formally canceled it.

…click on the above link to read the rest of the article…