Question: How do you know when you are in a bubble?

Answer: Gauge asset prices against a standard, foundational premise to determine if the price appreciation is warranted.

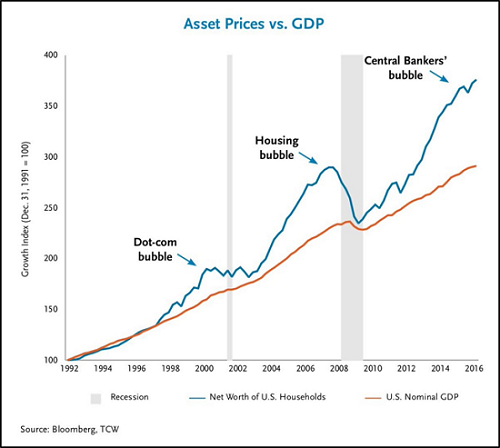

Lucky for us, the Federal Reserve provides exactly what is needed to show how unjustifiable current prices are against households disposable income. The chart below is all US household’s net worth (current value of all real estate, stocks, bonds, etc.) as a percentage of their disposable personal income (disposable income is what they have left to spend or save after paying their taxes). To round out the picture, I’ve added in the net growth in full time workers during each period, dramatically decelerating.

Since 1970, every time asset values have risen above 520% of households disposable income (the dashed line in the chart) then the US has been in a bubble and a subsequent crash has followed. This has simply meant asset values growing much faster than households income or households capability to sustain those price increases. The depth of each crash has been relative to the overshoot of asset values on the upside.

Why???

I hear much discussion that the millennials are the largest age group in US history and are expected to drive growth in demand. However, most people fail to understand what this truly means. The millennials are just marginally larger than the boomers but what this truly means is zero growth. The millennials are just meeting the previous high water mark the boomers set. When the boomers came through, they nearly doubled the previous high water mark.

…click on the above link to read the rest of the article…