“Americans today fear that linearism (alias the American Dream) has run its course. Many would welcome some enlightenment about history’s patterns and rhythms, but today’s intellectual elites offer little that’s useful. Caught between the entropy of the chaoticists and the hubris of the linearists, the American people have lost their moorings.” – Strauss & Howe – The Fourth Turning

“The most effective way to destroy people is to deny and obliterate their own understanding of their history.” ― George Orwell

The American Dream, where all Americans, no matter the circumstances of their birth, had a legitimate opportunity to live a better life than their parents, based upon their own intelligence, work ethic, and good fortune, is an illusion in today’s world. The ruling elite have stolen the wealth of the nation and its citizens. This was not an accident, but a plan implemented over many decades, accelerating after Nixon closed the gold window and opened the door to unlimited amounts of debt being created out of thin air and backed by nothing.

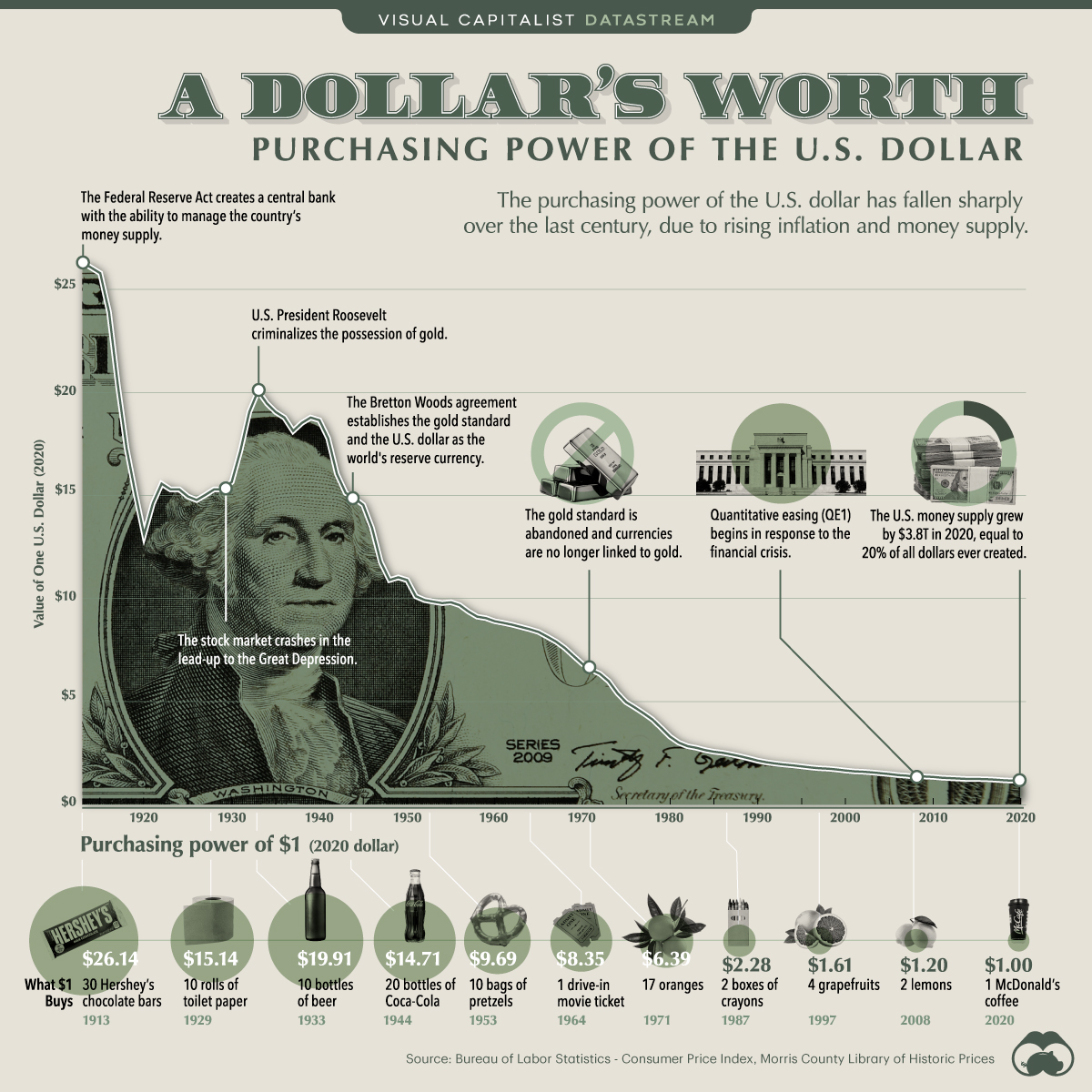

One of the Fed’s only mandates was to maintain a stable currency. Since its inception in 1913 to 2020, the USD had lost 96% of its purchasing power. The USD has lost 7.5% of its purchasing power since 2020, as Powell and his cronies have lost control of inflation.

…click on the above link to read the rest of the article…