Central banks still brush it off as just “temporary.”

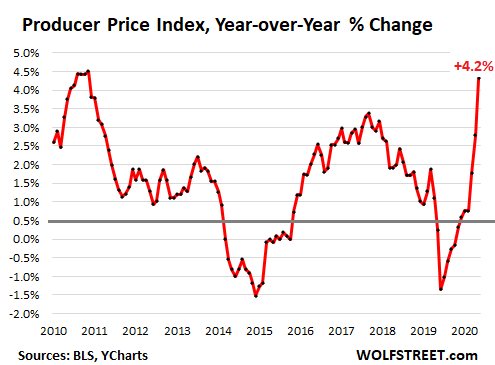

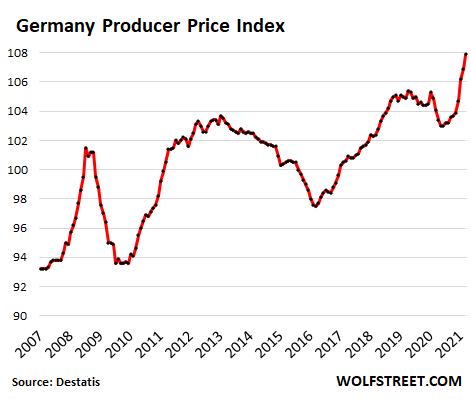

Producer prices of German industrial products in March rose by 0.9% from February, after having risen by 0.7% in February from January, and after having spiked by 1.4% in January from December, the biggest month-to-month jump since 2008.

Compared to March last year, producer prices jumped by 3.7%, according to the German Federal Statistics Office (Destatis), the biggest year-over-year jump since November 2011. The surge began last fall, after sharp declines earlier in the year:

Part of what caused the 3.7% increase from March last year — but not the surge over the past few months — is the “base effect“, since in February and March last year the producer price index was declining, and the latest year-over-year results are measured from those low points.

But factory prices have been rising on a month by month basis for the seventh straight months — with large increases over the past three months. And that has nothing to do with the base effect.

Prices of intermediate goods jumped by 5.7% year over year in March, the fastest since July 2011, due mainly to sharp rises in the price of secondary raw material (47%) and prepared feed for farm animals (16%). There were also increases in durable consumer goods (1.4%) and energy (8%), which in large part were driven by a sharp increase in electricity prices (9.6%).

Producer prices are now rising fast in the major manufacturing economies.

In China input costs rose 4.4% in March from a year earlier up from a 1.7% increase in February. It was the sharpest rise since July 2018. As the world’s biggest exporter, China’s rising prices stoke inflation around the world.

…click on the above link to read the rest of the article…