An example of this can be seen as iron ore prices hit a six and a half year high on Thursday as the Chinese construction and manufacturing sector claims to be experienced levels of activity not seen for almost a decade. Fastmarkets MB reported that benchmark 62% Fe fines imported into Northern China were changing hands for $129.92 a tonne on Tuesday, up 2.1% on the day. That would be the highest level for the steel-making raw material since mid-January 2014 and put gains for 2020 to over 40%.

The biggest black swan facing the financial system is China.

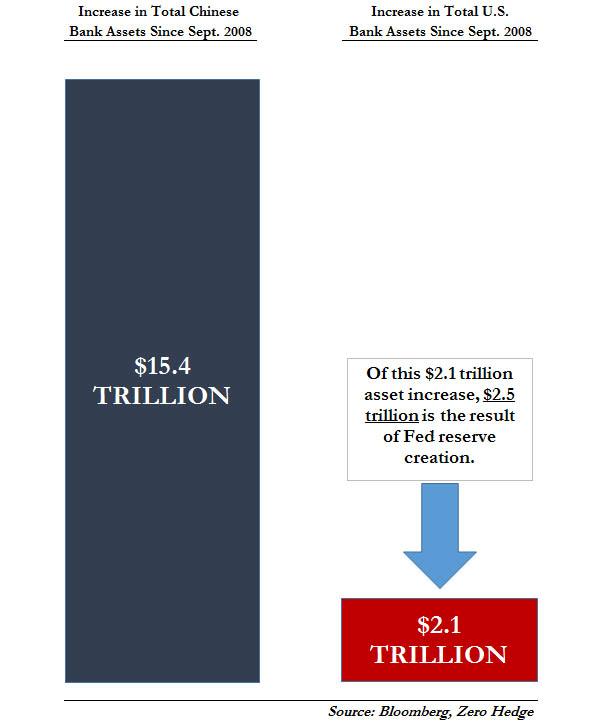

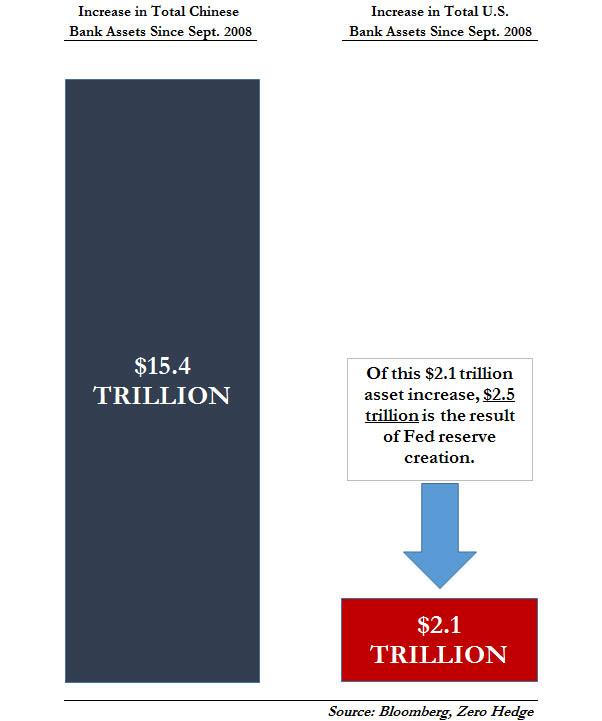

China has been the primary driver of growth for the global economy since the 2008 Crisis. Despite only accounting for 15% of global GDP, China accounts for 25%-30% of GDP growth.

Put simply, from an economic perspective, if China catches cold, the world gets sick… and if China goes into a coma…

Which is why anyone paying attention should be truly horrified by the latest round of data from China’s economy.

In December, China’s Manufacturing PMI came in below 50, signaling a contraction is underway.

This is a massive deal because this was an OFFICIAL data point, meaning one that China had heavily massaged to look better than reality.

Let me explain…

Over the last 30 years China’s economic data has ALWAYS overstated growth. The reason for this is very simple: if you are an economic minister/ government employee who lives in a regime in which leadership will have you jailed or executed for missing your numbers, the numbers are ALWAYS great.

Indeed, this is an open secret in China, to the degree that former First Vice Premiere of China, Li Keqiang, admitted to the US ambassador to China that ALL Chinese data, outside of electricity consumption, railroad cargo, and bank lending is for “reference only.”

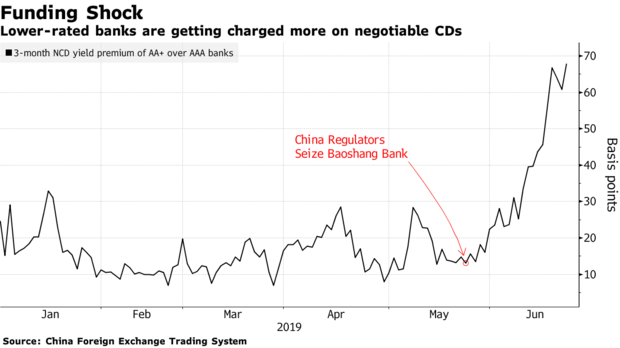

With that in mind, we have to ask… how horrific is the situation in China’s financial system that even the heavily massaged data is showing a contraction is underway?

Think “systemic risk” bad.

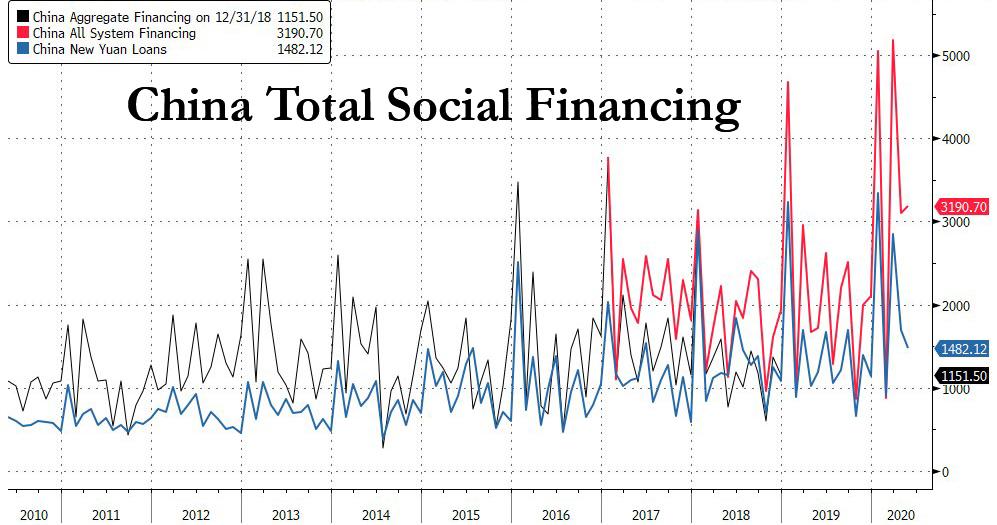

I’ve already outlined how China is sitting atop 15% of all junk debt in the global financial system, resulting in the country’s “bad debt” to GDP ratio exceeding 80% (a first in history).

However, it now appears that even that assessment was too rosy.

…click on the above link to read the rest of the article…

{kind=link}