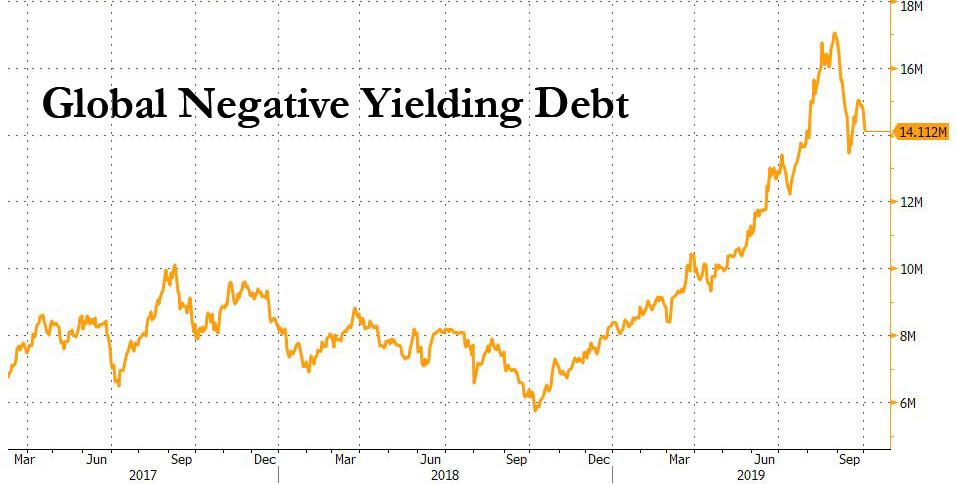

We are often warned that negative interest rates are an approaching menace — not an immediate menace.

Yet are negative rates already reality in the United States? Has the unholy day already arrived?

Today we don the sleuth’s cap, step into our gumshoes… and unearth evidence that negative interest rates are not the future menace… but the present menace.

What is the evidence? Answer anon.

Under negative interest rates…

Your bank does not compensate you for stabling your money with it. You instead compensate the bank for stabling your money.

A man sinks a dollar into his bank. Under standard rules he hauls out a dollar and change on some distant date — perhaps $1.05.

These days he is of course fortunate to bring out $1.01.

Yet under negative interest rates he endures a rooking of sorts. He pulls out not a dollar and change — but change alone. The bill itself has vanished.

His dollar may be worth 97 cents for example. Thus his dollar — rotting down in his bank — is a sawdust asset, a wasting asset, a minus asset.

Would you willingly hand a bank a dollar today to take back 97 cents next year? You are a strange specimen if you would.

Yet that is precisely as the Federal Reserve would have it…

The Federal Reserve wants your money eternally up and doing, searching, hunting, grasping… adventuring…

It must be forever acquiring, forever chasing rainbows, forever upon the jump.

That is, the Federal Reserve would not allow your money one contemplative moment to sit idle upon its hands… and doze.

For a dollar in motion is a dollar in service — in service to the economy.

The dollar in motion runs down goods and services. It invests in worthwhile and productive enterprises.

…click on the above link to read the rest of the article…

{kind=link}

{kind=link}

{kind=link}